Updated on: November 12, 2020 ; Investments

Recap:

This is the final and the fourth part of the 4 part series on SIPs. In the previous articles, we looked at the performance of SIPs of largecaps, midcaps, and smallcaps. The links for the same are given below. I request you to please read them before going through this article. In this article, we will go ahead with SIP comparison, so it is important that you have read the previous three articles.

SIP comparison:

In the previous articles, we analyzed each kind of SIP individually. But here we will make a direct comparison. The time period of analysis was different in the case of SIP (Sensex). So we have taken a common time period for all the three SIPs in this article.

Since overlapping data is available only from April 2003 for all three scenarios, the period under consideration will be from April 2003 till October 2020. That makes it 211 monthly data points for each scenario. Following the same process as before, we will look at the rolling-window CAGRs for different durations, starting from 1 year to 15 years.

Analyzing all the three ‘cap’ SIPs for the same time duration will enable us to make a true comparison between them.

Before we proceed with the comparison charts, I would like to call out a few things. The normal convention is to think that higher risks result in higher returns. We all know that smallcaps are riskier than midcaps, which in turn are riskier than largecaps (represented by Sensex here). So the expectation would be to get the highest returns from smallcaps. Next would be from midcaps, and then finally largecaps (Sensex).

Also, please keep in mind that this analysis is based on very limited data, so make your judgment with a pinch of salt. I personally would have liked to have at least 15-20 years of additional data in the analysis.

Now, let’s start looking at the data and see what it has to reveal. First, we will be looking at the average returns for different rolling windows, followed by the range charts. The representation here is slightly different from the previous articles. This was required to show a comparison between the three caps in a better presentable way. But, don’t worry it is the same information, just shown in a different way. So you should not have any difficulty in understanding the information if you have read the previous articles.

SIP comparison of average returns:

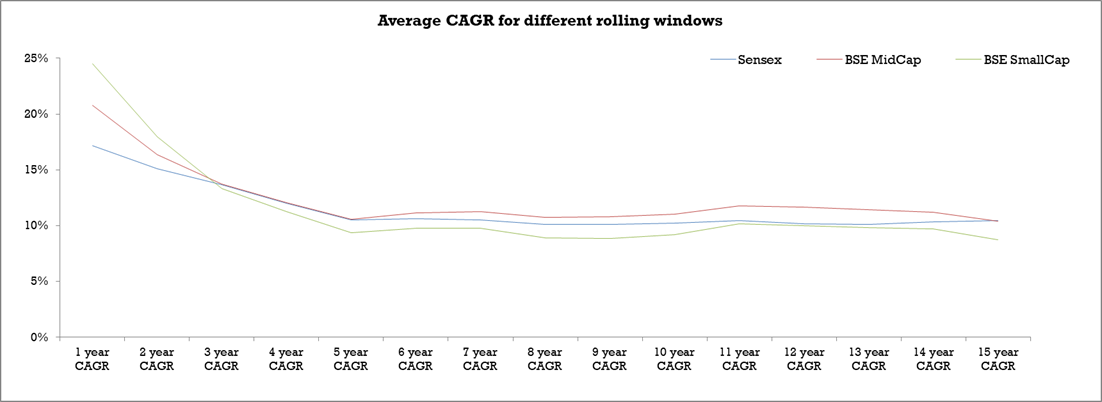

Here, we will take a closer look at the average returns of the SIPs of the three caps. Large(Sensex), midcap(BSE MidCap), and smallcap(BSE SmallCap). The average returns for the 15 different rolling windows are listed in the table below. The same information is also shown right below the table in the form of a chart. This is to provide a better visual for your understanding.

If we look at the 1-year and 2-year CAGRs, we find that the smallcaps have outperformed the other two. After smallcaps the next best performing SIP is the midcaps. This is in line with the expectation of higher returns for riskier investments. But as the duration of the rolling window increases the gap narrows. In fact, very soon we see a reversal of trend, 3-year window onwards. The smallcap SIP is the worst performing for durations greater than 2-year. This is contrary to the popular belief.

Next, we compare the midcap CAGRs with Sensex CAGRs. We find that midcaps have outperformed Sensex across all the durations, with the only exception of the 15-year window.

Let’s analyze these numbers qualitatively. The Sensex has given above 10% returns consistently. Midcaps have given above 11% in most of the cases. Both these returns are very good. On the other hand, smallcaps have underperformed midcap or Sensex by around 1.5% across most of the longer durations.

Just by looking at these numbers, it looks as if midcaps is the clear winner. Smallcaps don’t seem to be a very attractive option in comparison to the other two caps. But hold on a second, the picture isn’t complete until we analyze the risk associated. Normally risk is measured in terms of standard deviation.

But I will not complicate matters here. We will look at the range of CAGRs to understand the maximum and minimum potential returns. This is the same approach that we followed in the previous articles. More on this in the next section.

SIP comparison of CAGR range:

Now, it is time to look at the range of the CAGRs for different rolling windows. This will help you understand the volatility in the CAGRs realized in the past. More importantly, it will also highlight the maximum potential loss faced by SIP investors in the past.

We will first look at the maximum and then at the minimum CAGR values.

Maximum range:

We have represented the maximum CAGRs for each rolling window for the three caps in the table below. Right after that, we have represented the same information in the form of a chart for better visual representation.

What we clearly see here is that for the lower durations the highest CAGRs are seen for smallcaps, followed by midcaps. Sensex has given the least returns. As the duration increases, the gap between the three reduced significantly. What it signifies is that smallcaps and midcaps have much higher volatility than largecap(Sensex), especially for the lower durations.

They’re a few periods when these SIPs have given unbelievable returns, but don’t get blinded by these numbers. These are special cases, and no one knows if and when will they repeat. Maximum returns should never be your guide for making investment decisions. We are showing you these numbers so that you get familiar with these past returns.

Another interesting point to note here is that, after the 9-year window, midcaps have given better results than smallcaps. This is something to keep in mind as it is again against normal expectations. Some of us would have expected the smallcaps to have outperformed midcaps throughout. It means that over longer periods the wide swings seen in smallcaps, limit their upside when compared to midcaps.

Now it is time to look at the more important aspect – the maximum possible downside or the minimum range.

Minimum range:

Let’s analyze the minimum values in the table and the chart below.

We can see that smallcap SIPs have the biggest downside, followed by midcaps. Sensex is the best among the three when it comes to minimum CAGR. This makes Sensex SIPs the safest best within these three caps.

Also, note the magnitude of these returns. It is worth pointing out that smallcap SIPs had a minimum CAGR of -2.9% for the 9-year rolling window. That is a big setback for any investor for such a long time duration. This doesn’t mean that all 9-year smallcap SIPs had negative returns. This highlights the fact that there were times when investors could have experienced such negative returns in the past.

The scene improves for all three scenarios as we move to the right. The Sensex CAGRs exceeds the other two consistently.

So, now you can compare all three tables and charts and make your own long term SIP decisions. This 4 part series is by no means the only guide to your SIP investments. But this is an attempt to bring to light the SIP performance of the three caps and the potential downsides associated with them.

Conclusion:

We finally conclude our first series on SIP comparison. We have observed that smallcap SIPs have given lower average returns over longer durations. There have been a few sparks of brilliance in very short durations of 1 year or 2 years for smallcaps, but they are not consistent. Smallcaps also have the maximum potential downside that can stretch over long durations if the investment time is not correct.

Surprisingly midcap SIPs have performed better than Sensex SIPs in terms of average returns as well as maximum returns. But they are worse performers than Sensex when it comes to minimum returns, so there is this risk associated with midcaps as well. You can opt for Sensex or midcap SIPs or funds closely linked to them depending on your risk appetite.

Based on what we have seen, you would be better off avoiding smallcap SIPs, until you are sure of the market timing and attractive market level of smallcaps.

Choose your SIPs wisely !!!