Updated on: May 15, 2021 ; Investments

Background:

We have already covered a few interesting PE based investment strategies. Moving ahead in the same direction we will cover another strategy called the PE based swapping strategy in this article. This strategy is built upon the previous two strategies with a few modifications.

I urge you to please go through the previous strategies if not done already. This will bring in some logical flow to the analysis. Following are the links to the previous strategies.

Anyone new to the concept of PE ratios need not worry. Please find here the simple explanations for the “meaning of PE ratios” and its usage as an “indicator”.

PE based swapping:

In the previous strategies, we saw how you would channel your monthly investments into equity or debt assets. We also looked at the strategy where you would move the entire debt component into the equity bucket based on pre-determined Nifty 50 PE levels.

In the first case, there were no withdrawals from either of the two investment buckets (equity and debt). In the second case, the entire debt corpus was switched over to the equity bucket at the threshold PE levels.

But, there were no withdrawals from the equity bucket in both cases. This is going to change in this strategy.

But, before we dwell deeper into it, let me provide a bit of a background on the base assumptions. Readers already familiar with it can skip the next five paragraphs.

We provide the investor with a choice of two fundamental financial assets only. One is an equity asset, and the other is a debt instrument.

For equity, we have considered the Nifty 50 index. And for debt, we have assumed a risk-free debt instrument that gives an 8% return annually.

In the real world, there are many more choices available to an investor. But, we are going ahead with these two basic assets to avoid any unnecessary complexities.

As far as data is considered, we have used monthly data for Nifty 50 starting from January 2001 till January 2021. The Nifty 50 level and its corresponding PE ratios are recorded at the start of each month.

The assumption is that the investor has 1000 rupees at the beginning of each month to invest. He/She can either choose to channel the investment in the equity bucket or the debt bucket. The default choice is to invest it in the equity bucket. This default choice will be our base case.

In the PE based swapping strategy, once the Nifty 50 PE level crosses above the set threshold, the investor invests the monthly investment into the debt instrument. In addition to that, the investor will also move the entire equity component into the debt bucket.

Similarly, when the Nifty 50 PE goes below the threshold value, the investor invests the monthly component into the equity bucket. Also, the entire debt corpus is moved to the equity bucket.

We have named this strategy the “PE based swapping strategy”. This is because the entire investment corpus is swapped between equity and debt. This swapping is driven

A complete swap takes place so that at any given point in time the entire investment corpus either lies in the equity bucket or the debt bucket.

This strategy is a bit aggressive and needs a lot of conviction to deploy.

We have considered an exit load of 0.5% for withdrawals from debt funds and an exit load of 1% for withdrawal from equity funds. This is in line, if not more than the prevailing market rates.

Based on the previous article “Can PE act as an indicator“, we have chosen two PE levels as the threshold levels. They are 22 and 18. The investor will channel and swap the investments based on these threshold values. We will compare the investment values throughout the analysis period with the base case. In the base case, the investor continues with the simple monthly SIP of 1000 rupees in the Nifty 50 index.

We will also take a look at a small variation of the above strategy. In this, the swapping decision is based on the 12-month moving average PE of Nifty 50. This is to ensure that swapping happens only when the PE threshold has been breached for a long time.

Now, let’s have a look at the graphs and see if this strategy is any better or worse.

Strategy in action:

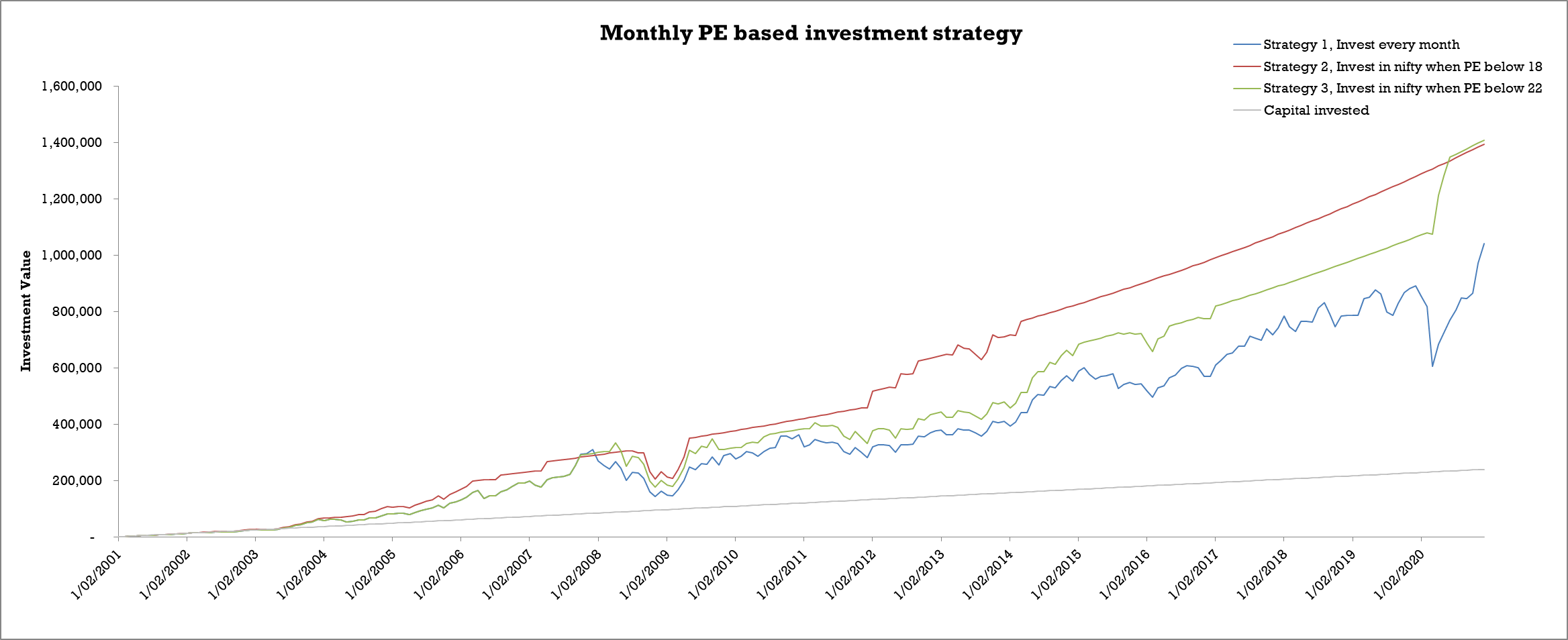

The graph below represents the performance of the monthly PE based swapping strategy.

The first striking point you can’t miss is the gap between the performance of the three strategies.

Strategy 2 is the best performer here. There is a wide positive gap between strategy 2 and the other strategies for almost the entire investment duration. You can also notice that for a significant time duration the investment value grows at a steady pace. This is the period when the Nifty 50 PE is above the respective PE threshold, and the entire corpus is parked in the debt bucket.

Strategy 2 dwarfs the performance of strategy 3, which is also an outperformer. You can see that in the last leg it suddenly jumps to overtake strategy 2 by a small margin after lying low for a long time. This is the point when the Nifty 50 level changes its gear back and forth. It crosses below 22 and remains there for 3 months, moving all the corpus to the equity bucket.

Then there is a sudden spike in Nifty 50 and the PE crosses above 22 again. This makes us move the whole corpus back to the debt bucket. This sudden spike in Nifty is enough to toss up the performance of strategy 3.

The other very interesting point to note is the minimal impact of market fluctuations (especially during the downside) on your investments. Compare the drop in the performance strategy 3 in April 2020 with that of strategy 1 and strategy 2.

The swapping of entire equity corpus to debt safeguards the portfolio from the sudden falls experienced in the market.

Out of all the strategies studied so far, strategy 2 at PE = 18, has given the best results retrospectively.

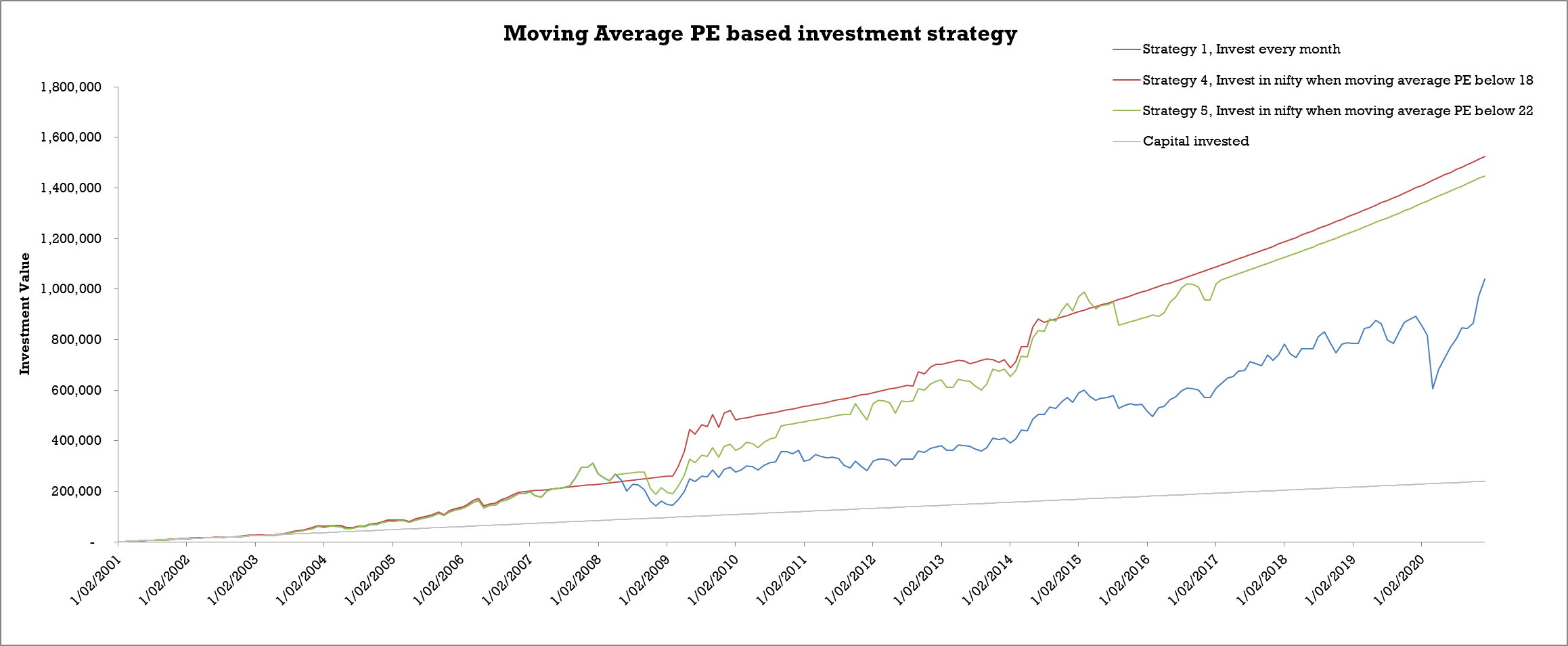

Following the tradition, we will also look at the performance when we use moving average PE (12 months) instead of monthly PE.

The performance here is even better than before. Strategy 5 also closely follows Strategy 4 with a constant negative gap. To get the real taste, let’s look at the actual investment values at the end of 20 years investment time horizon.

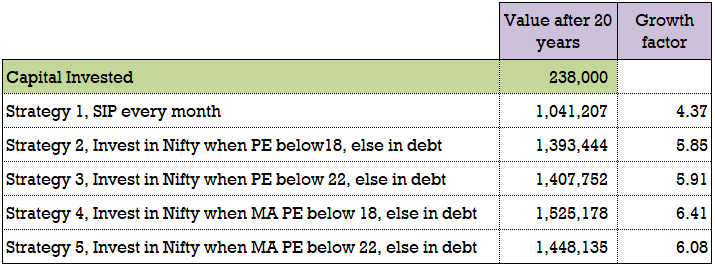

This swapping strategy has given the best performance so far. The base case has given ~4.4x returns. In comparison, all the different variations of PE based swapping strategy have given almost 6x returns.

But, don’t get too excited yet. There is always more to look at and explore.

You need to look at another set of numbers. If you have gone through the previous posts, you would know that the value of your investments depends on the investment time frame.

To complete our analysis, we will look at the scenario when the investment’s start time coincides with a market peak. For this, we have chosen a time before the financial crisis of 2008. This would have been one of the worst possible starts for any investor to get into the markets. So choosing this time frame would help us understand the performance of the investments under unfavourable conditions.

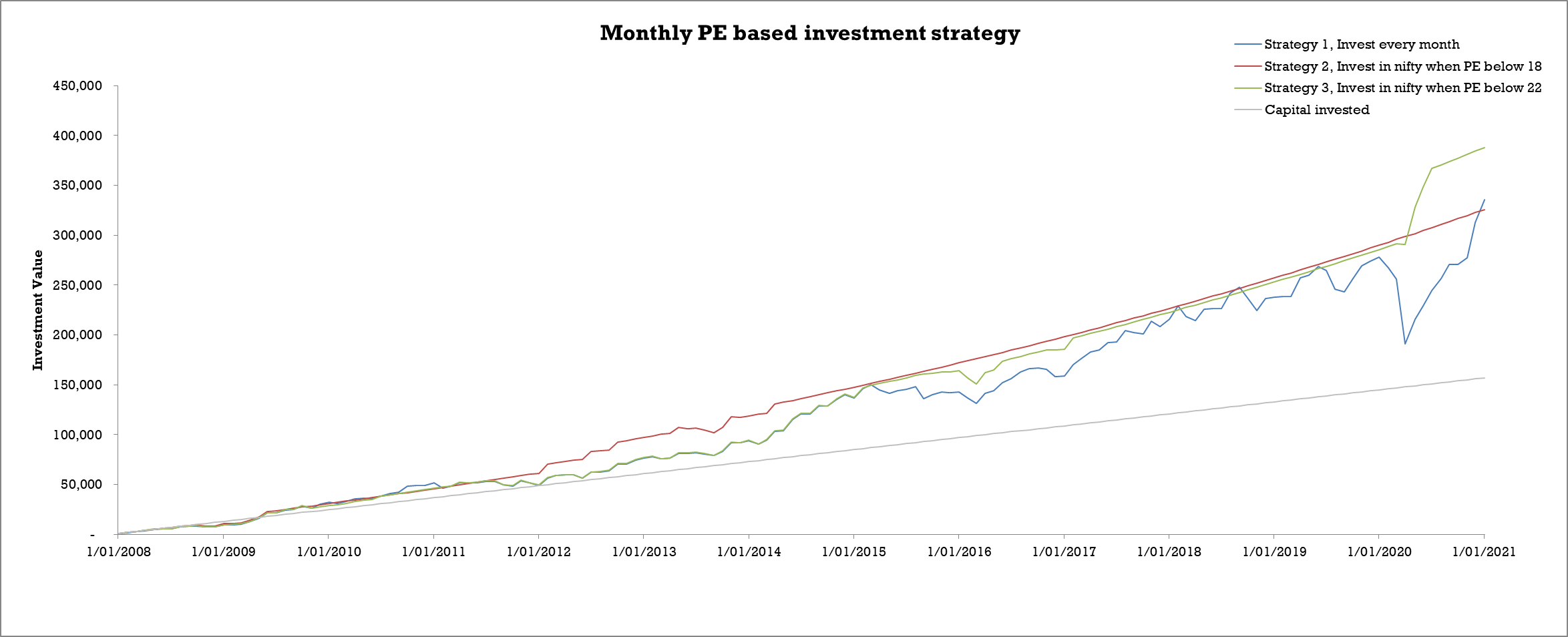

So, we repeat the same analysis with a different start time. With this, the investment time period reduces to 13 years from 20 years. Time to look at the graphs now:

This graph represents a slightly different story. Strategy 2 and 3 are still better performers than the base case. Although the difference is not as prominent as in the previous graphs, it is free from the market fluctuations to a large extent.

I would rank strategy 3 slightly above strategy 2 in this case because of the wider performance gap in the last leg.

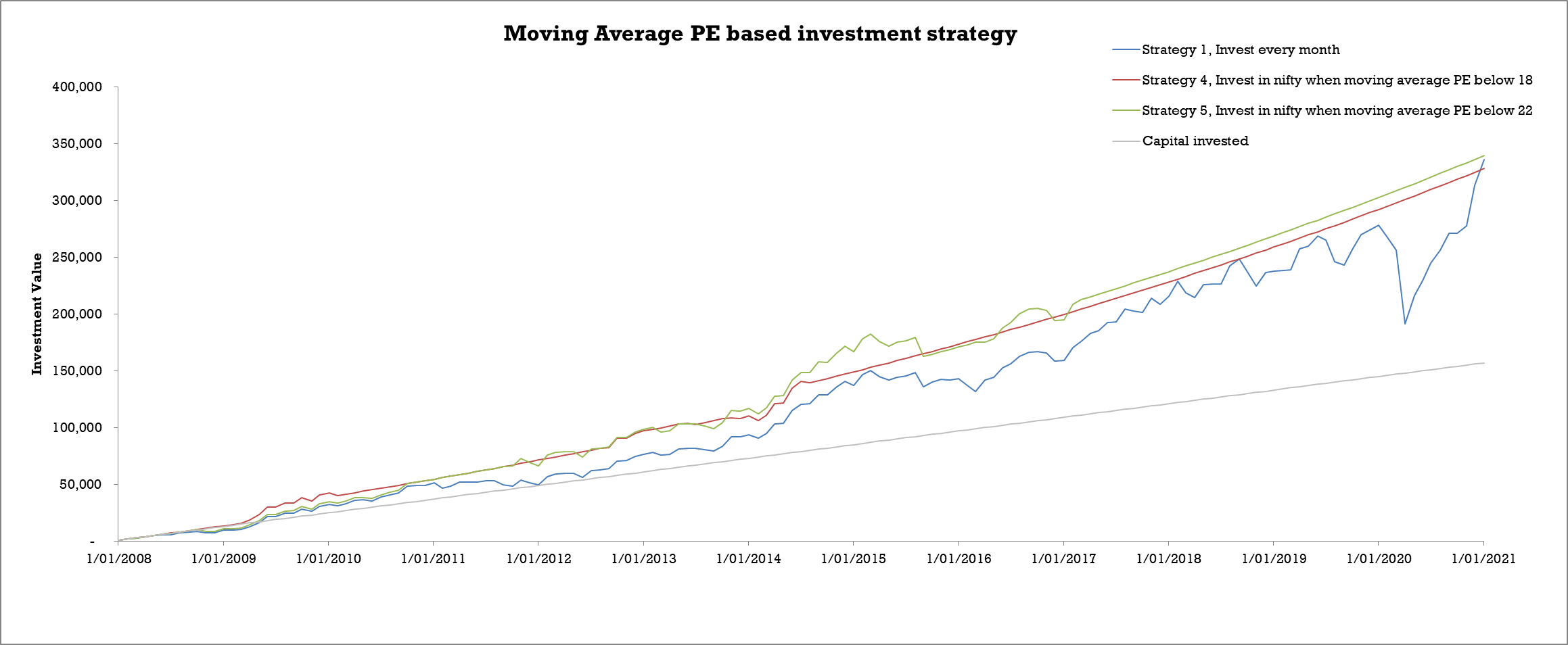

Time to look at this strategy in play with 12 month moving average PE values.

There is not much to choose between strategy 4 and 5 here. Both of them provide protection from market gyrations with slightly superior returns.

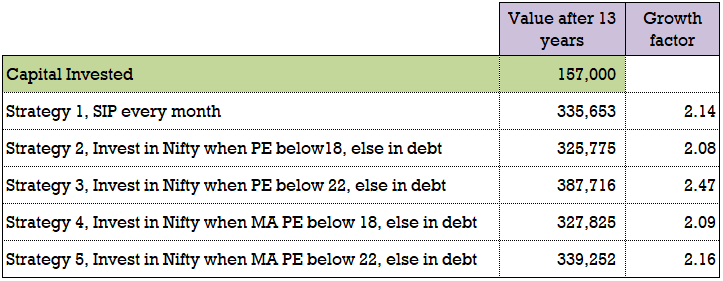

Let’s take a look at the summary table before we conclude.

These numbers don’t do justice to the actual performance. It is in the last few months that the base case catches up with the other strategies. Otherwise, this PE based swapping strategy has provided a good combination of superior returns and more importantly, downside protection throughout the 13 years investment period.

Key takeaway:

Following are the key points based on the numbers and the charts analysed above:

- PE based swapping strategy has given the best returns compared to all the other PE based strategies studied so far.

- This strategy provides greater stability to your portfolio with good downside protection.

- Over long periods of time, PE=18 seems to be better than PE=22.

- Even when an investor starts at a time when the markets are high, this strategy has turned out to be good.

- To conclude, if you have the conviction and the discipline to monitor and restructure your portfolio, then you can seriously consider deploying this kind of strategy.

Get strategised !!!