Updated on: June 10, 2021 ; Investments

Background:

So far, we have explored 6 stock portfolio investment strategies. Please go through them so that you get a better perspective of the options we have discussed and also understand the flow that we follow in each article. You can just click the previous post link at the end of the post or search for ‘weighted portfolio’ in the search bar above. Today, we will be exploring an equal-weighted portfolio with rebalancing.

This is similar to the equal-weighted portfolio that we discussed in the first article in this series, with a fundamental change in the way we manage the investments. Will talk about this in detail in the following sections.

Portfolio selection:

You can skip this section if you are already familiar with scenario 1a and scenario 1b.

To start with, we will have to choose an index. What else could be a better choice than India’s first equity index – S&P BSE Sensex. It was first launched in 1986, with the base year being 1978-79. It had the 30 largest companies of that time. Most of them were industrial companies with no presence of any bank or technology companies.

But this composition kept changing with time. If you were to look at the Sensex in 2000, or 2008, or 2020, you would see very big differences.

As market conditions and business outlook change over time, the stock prices of different companies react differently. This results in the need for reconstituting Sensex as the market capitalization of companies rise and fall. Only the companies that meet some stringent criteria, can be part of Sensex. We won’t be dwelling into that here. All we need to know is that market capitalization is the most important deciding factor.

Since we plan to study the performance of an equal-weighted portfolio of stocks vs Sensex, to be fair, we need to choose our stocks from Sensex. But, given the volatility of the Sensex itself, it might be a bit challenging to do the stock selection. The ideal way would be to pick your stocks based on strong fundamentals and thorough research. But for the sake of simplicity and unbiasedness, we will be using some very elementary rules to construct our portfolio.

Before we get into the details of portfolio selection, let’s talk about the timelines a bit.

We plan to do a long term study of our equal-weighted portfolio with rebalancing. Well, if you have been following me, then all my studies have been long term. So nothing surprising here. For this, we have taken the investment period to be from March 2003 till March 2021, 18 years.

But choosing a portfolio of stocks for investment in 2003 while standing today in 2021 won’t be fair. Today we have the luxury of knowing the past performance of all the stocks. So any stock selection won’t be completely bias-free. We can rephrase this as – we can never be too sure of ruling out any bias if we construct an equal-weighted portfolio of stocks for 2003 in 2021.

To keep this study unbiased, we will take the help of simple heuristics or rules. There can be many rules one may apply. We will be applying one such simple rule in this study. More on this rule in the next paragraph.

I have already mentioned that Sensex has undergone many changes since its inception. So we decided to construct an equal-weighted portfolio with stocks that survived to remain in the Sensex for a long time. This would mean that these stocks have some sort of robustness and strong fundamentals built in them.

For this, we started with the 30 stocks that were part of the original Sensex (1986). Then we looked at the stocks that had the biggest market capitalization in March 2003. Next, we picked up the common stocks from both these lists to construct our equal-weighted portfolio. These were the stocks that remained in the top 30 slots even after 17 years.

You may ask that why did we choose 2003 and not any other year. Actually, we could have chosen any other year as well. One reason for choosing this year is that I found the data for this year easily.

Methodology for equal-weighted portfolio with rebalancing:

Since we are using the same stock/portfolio selection criteria as scenario 1a and 1b, we will be using the same set of stocks in our portfolio. They are:

- Reliance Industries

- Hindustan Unilever

- ITC

- Nestle India

- Tata Motors

- Hindalco

- Tata Steel

- Larsen & Toubro

We will be analysing two scenarios in this 7th part of the multi-part series on stock portfolio investment strategy. As you already know, this part is dedicated to an equal-weighted portfolio, so both scenarios will have equal-weighted portfolios.

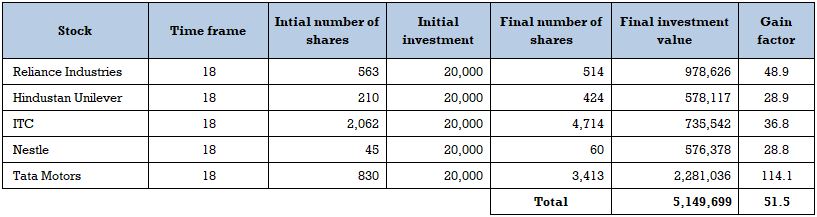

In the first scenario, we construct our portfolio with the top 5 stocks only. That means the first portfolio (Scenario 7a) consists of Reliance Industries, Hindustan Unilever, ITC, Nestle India, and Tata Motors.

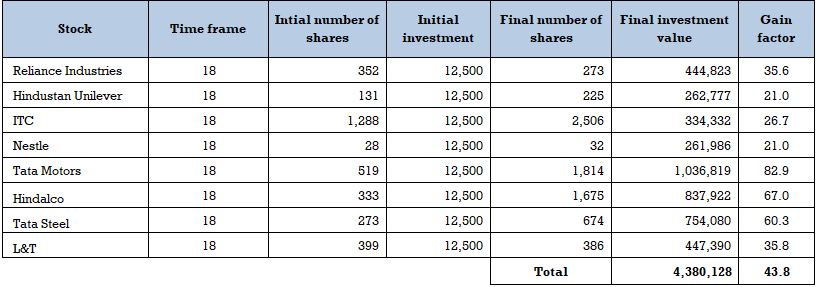

The second portfolio (Scenario 7b) consists of all the 8 stocks listed above.

Now Equal-weighted means that we invest an equal amount of money in each stock in our portfolio.

We assume that we had a corpus of 100,000 rupees to start in March 2003. So in ‘Scenario 7a’ where we picked 5 top stocks, we allocate 20,000 rupees to each stock. And in ‘Scenario 7b’ where there are 8 stocks, each stock gets 12,500 rupees as the initial investment.

We compare both these scenarios with the third case. This third case serves as the base case, where the entire 100,000 rupees is invested in the broad index, i.e. Sensex.

Now, I will be talking about the point that makes this strategy different from the previous ones. The point is rebalancing.

At the end of March each year, we equally redistribute the entire corpus/investment across the stocks in the portfolio. What it means is that, at the end of March of any year, we pull out the money by selling the stocks and use that money to redeploy an equal amount of money into each stock.

Suppose the corpus grew to 200,000 at the end of March in a particular year, then under ‘scenario 7a’, each stock gets get 200,000 / 5 = 40,000 and in ‘scenario 7b’ each stock gets 200,000 / 8 = 25,000 after redistribution. This is called rebalancing.

This is repeated each year at March-end without fail.

Now, since we are pulling out money every year, there will be some costs involved. The two major cost components are the transaction costs and the capital gains tax. Now because the money is pulled out after 1 year, you will be charged long term capital gains tax instead of short term capital gains tax. If you are not familiar with these cost components, then don’t worry too much. I will provide all the necessary information you will need to understand the rebalancing strategy.

Transaction charges and other regulatory taxes apply whenever you buy or sell stocks. This applies to the total value of the transaction. We have assumed this to be 0.25%.

Next, you have to pay capital gains tax if you make a profit by selling stocks. we have considered the tax rate to be 10%, which is the prevailing rate today. Please note, these charges are subject to change based on revised government policies and regulations.

In the real world, each year some stocks will grow faster than others. So for rebalancing, you will only pull out the additional money that needs to be redistributed from the better-performing stocks and invest it back in the stocks that have performed poorly compared to the rest. But in our case, we have assumed that we pull out the entire corpus and then rebalance the portfolio.

This serves two purposes. First, it makes our calculation easy. Yes, I am being a little lazy here. And second, it assumes the maximum cost that one can incur. This means that the returns we calculate will be on the conservative side, and the actual returns will be higher for these scenarios.

Just to re-iterate, in rebalancing, we take out the relative gains made in the stocks that have performed better than the rest. Then, we distribute these gains among the stocks that have performed worse relatively. So that each stock has an equal capital allotment after rebalancing.

This is done with the view that each stock in the portfolio will eventually do well in the long run. The interim highs and lows will provide opportunities to buy and sell. Investors can sell the stocks when they are relatively highly-priced, and buy them back when they are relatively cheap.

But in our strategy, we don’t do this activity too frequently. We have pre-decided the timing and frequency of rebalancing. We do it every year at March-end without any changes or exceptions.

Also, we do not add any additional corpus or withdraw money out of it. So it is like a lump sum or one-time investment, but with annual rebalancing.

Now, that we have understood the concept of rebalancing, let’s see how did these scenarios performed in the past.

Comparative study:

Take a look at the tables below. The first table summarizes the performance of the corpus invested in Sensex as of March 2021. You must be familiar with this table already if you have read any of the previous articles in this series.

The next two tables summarise the performance of the two scenarios (7a and 7b).

One point to note is that the portfolio values at the last point of observation (Final investment value), i.e. on March 2021 are just before rebalancing. This is to show the value of the portfolio before the transaction charges and the taxes apply. The charges for rebalancing were deducted at the start of the year, so there is no need to deduct it again at the end of the year.

Also, note that the number of shares has changed for each stock over the investment period.

What we see is that both the scenarios have done extremely well when compared to the Sensex.

Scenario 7b grew close to 45 times (CAGR of 23.4%), whereas scenario 7a grew more than fifty folds (CAGR of 24.5%).

Now, look at the gain factor for each stock in both scenarios and compare it with the Sensex. Each stock has individually performed better than the Sensex. So, an equal-weighted portfolio with rebalancing definitely has some merits as an investment strategy.

It also seems from these numbers that the portfolio with a lesser number of stocks has performed better. We will revisit this point after we have looked at the chart below.

But before that, let’s compare these numbers with the previous well-performing strategies that did not have rebalancing. Have a look at the tables in the equal-weighted portfolio and marketcap-weighted portfolio.

The equal-weighted portfolio with rebalancing performed much better than the other two strategies. In fact, this has been the best performing strategy of all the 7 strategies we have covered so far. At least, that is what the numbers say with this set of stocks in this investment time horizon.

But things might be different under different circumstances when you have different stocks and different start time.

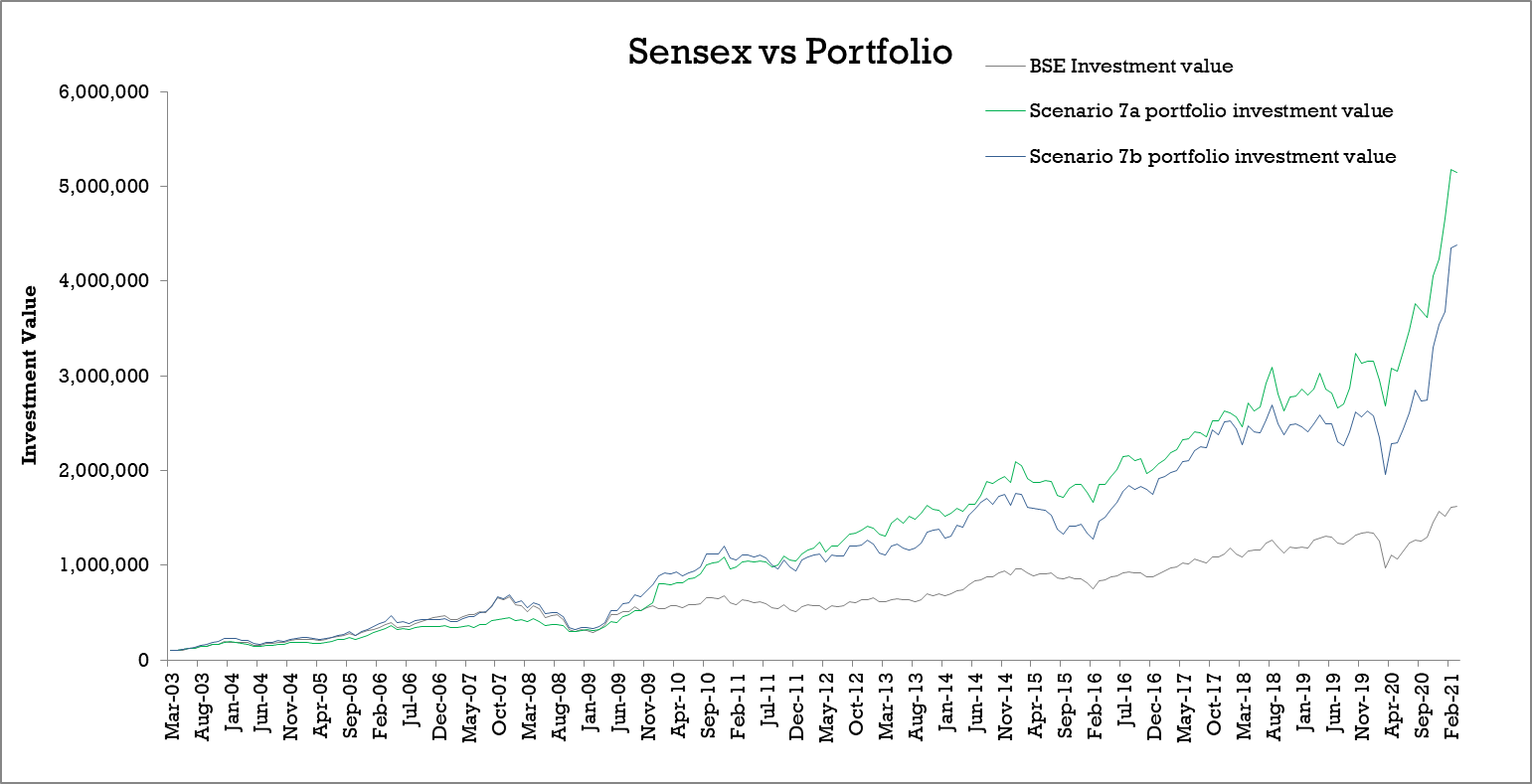

As you know, this is just a snapshot of the portfolio performance. So to understand it a little better, we will look at the monthly performance of the equal-weighted portfolio with rebalancing over the entire investment period.

These numbers have a very interesting story to convey. According to the tables above, ‘Scenario 7a’ was our star performer. But based on the chart, it was not doing as well in the first 6-7 years.

In fact, till October-November 2009, Sensex performed better than Scenario 7a. And it was only after September 2011, 7.5 years into the investment, that Scenario 7a overtook Scenario 7b.

You must be wondering why.

It was mainly driven by the poor performance of Tata motors during that period. But things turned around later, and all stocks in the portfolio performed well eventually, leading to the success of the portfolio.

So, an equal-weighted portfolio with rebalancing has the potential to give superior returns. But there are chances of failing if some of the stocks in your portfolio start failing and don’t recover.

Now coming back to the question we had asked a while back – if lesser stocks mean better performance. There is no straight answer to it. This is the classical case of diversification. Diversification has both its merits and demerits. In this case, if you picked a bad stock, then its negative impact will be lower in a portfolio with a higher number of stocks. On the other hand, having more stocks will dilute the positive impact of the top-performing stocks in your portfolio.

Therefore, it is even more critical to choose the right set of stocks in a rebalancing portfolio strategy.

Final remarks:

Rebalancing does give you a good mechanism to increase the value of your equal-weighted portfolio. But the success of it relies heavily on the success of each individual stock in your portfolio. It also benefits from the interim swings in the prices of the stocks, we call it volatility.

But it can backfire if any stock(s) in your portfolio starts to go down with no sign of recovery. You can see that in the first 7 years in the chart. So, you have to be very careful while making your stock selection.

You will have to regularly monitor the health of your stocks and be ready to change the composition of your portfolio. If you feel that some stocks in your portfolio are beyond redemption, then it would be best to get rid of them, even if it is at a loss.

There is no magic mantra for successful portfolio creation. You have to decide what is right for you.

Strike the right balance !!!