Updated on: September 19, 2021 ; Wealth & Value

The big question:

This is a question which most of us will have to face one day. The sooner we start thinking and planning for it, the better it will be. But, do we know how much we need to save for our retirement so that we can have a comfortable and stress-free time at least financially, post-retirement?

This might seem to be a very daunting question. And to add to it, it is very hard to predict our actual needs. But that doesn’t mean we should not be doing anything about it. It would be the most naive thing to do.

There are many simple rules of thumb that give an approximate estimate of your retirement corpus. That would be a good place to start.

Or, we could look at the problem from scratch. And work our way towards understanding the various factors that would impact the retirement corpus required.

Then start putting things together to compute the retirement corpus under different scenarios. And finally, find out – how much do we need to save for retirement.

The idea behind writing this article is to understand the many different factors that need to be kept in mind while planning, and saving for your retirement. To appreciate the impact of these factors and then enable you to finally plan better for your retirement.

I will try my best to cover most of the important aspects but feel free to incorporate any factor that might be relevant to you, which I missed out here.

Save for retirement:

The first thing to do is start saving. If you don’t have the habit of saving then you better start doing so right away. You can read here on the importance of savings. The sooner you start saving and investing your money at the right places, the smoother and painless the journey would be.

Disclaimer: I am not going to talk about where you need to invest your corpus. For that, you can read through my other articles where I have discussed different investment options and strategies at length.

The next obvious question would be: How much do I need to save? And…

What else?

There are loads of other factors upon which the answer to the previous question heavily depends. I have listed down them in the form of questions that you need to answer for yourself. You need to be brutally honest, and a little conservative with your approach while answering them.

Because if you get this wrong, there might not be many or any chances to redeem from. So be very careful while considering your answers.

- How much time is left to retire?

- What are my current monthly expenses?

- What inflation rate should I consider during my earning days?

- For how long should I plan my retirement corpus to last?

- How much of a contingency fund should I plan for?

- What is the right expected rate of return?

- What would be a fair annuity rate?

- Which are the other recurring expenses?

- At what rate do I expect my expenses to grow post retirement?

- What is the expected growth rate of my retirement corpus?

Now, the answer to some of these questions might be similar for many individuals. On the other hand, a few of them would be very contextual to you.

If you feel these questions are overbearing, don’t worry. I will help you work through them with a few examples and scenarios. Then you can plug in your inputs and make adjustments to derive at your own number. The final objective is not to come up with an exact number, because there is no exact number.

All you need to know is the approximate number that you need to save for your retirement.

Before we jump into the scenarios, let’s have a closer look at some of the factors or questions posed above.

How do they matter?

In this section, we will touch upon the critical factors, their directional impact, and the key assumptions taken into account while computing the scenarios. This is required so that you understand the importance of these factors while computing the savings for your retirement corpus.

To start with, you need to figure out, when do you want to retire? That will depend upon your current age and professional career. For our calculations, we have assumed that you will be working and earning till you reach the age of 60. The more time you have in hand, the less you need to save per month for your retirement.

If you plan to retire early, then your savings requirement would increase accordingly.

The next factor you need to consider is the time till which the retirement fund should be able to finance your needs. We have assumed life expectancy to be 100 and this might go up given the improvement in the health industry. So our calculations are such that the retirement corpus should last for at least 40 years and a few more years. That is from the time when to hit 60, till the age of 100.

Now, with the time-related factor covered, it is time to look at the other factors. You need to estimate your monthly expenses post-retirement. This could be very tricky, but a very critical factor in estimating your savings requirement. But using your current expenses as a starting point we can arrive at that number.

But, while computing your current monthly expenses you need to consider only the recurring expenses. You need to eliminate any mortgage payments or EMIs, assuming you would have cleared out all your debts by the time of your retirement.

If you think that you need to increase your monthly expenses to accommodate certain aspirations, then add such components to your monthly expense for calculation’s sake. Normally, aspirations and needs go down after you reach the retirement age, but I would urge you to consider such expenses for your calculations.

It is ok if you don’t spend that money later in life, at least you will have the option with you. So, estimate expenses on a higher side.

With the current expenses locked in, you need to come up with the corresponding figure at the time of retirement. For that, you will need to estimate the rate of inflation. This is because the prices will go up with time and so you will have to accommodate for it. We have assumed inflation to be at 5%.

The factor discussed so far would help you decide the monthly expense at the time of retirement. But you need to fund that requirement on an ongoing basis till the age of 100 years and maybe more. For that, you need to figure out the total money you need to accumulate when you retire. We call this the retirement corpus.

We assume that the retirement corpus would be invested in an investment vehicle that would be able to generate enough returns to cover your monthly expenses for the entire period of your retirement leg. For that, we assume a decent return rate of 4% annually on your retirement corpus. This is what we call the annuity rate.

What we mean by annuity in our case, is the money that you will withdraw from your corpus annually to fund your retirement.

Even though we are calling it as annuity rate, you need not necessarily invest in an annuity scheme.

This implies that 4% of your retirement corpus should be equivalent to your annual retirement requirement in the first of year retirement. In other words, the retirement corpus should be at least 25 times your annual retirement expenses.

Now, coming to the moot point. How much do you need to save every month to reach the retirement corpus? For that, we will look at a few scenarios with different investment return rates (8%, 10%, and 12%). Working backwards, we will arrive at the monthly savings required to be invested every month, to get us to the retirement corpus.

Other assumptions and considerations:

No one can plan everything to perfection. So we have to consider enough margin in our calculations. For that, we will add an additional 20% to our retirement corpus. This is what we call our contingency fund.

Your expenses post-retirement will also increase. We have assumed that to be at 3%.

Also, the retirement corpus is assumed to be invested in some safer investment vehicle(s) giving a return of 6%. This is important as your annual expenses (what we are calling as annuity) will deplete your corpus. So you need the retirement corpus to be invested at some place where you get a decent return. This will ensure that your corpus lasts longer.

In case you missed it, your recurring expenses like health and life insurance should also be considered in your monthly expenses.

I believe, now you have a fair idea of the various factors that you need to consider to derive your number for the monthly savings. You should also be able to appreciate that your number will change a lot based on person to person.

To help you, we will list out a few different cases, so that you can understand the interplay of various factors and their impact on the monthly savings number.

Scenario of savings for retirement:

In this section, we will explore a few different scenarios by varying two key factors:

- Investment period, this is directly correlated to the time when you start saving for retirement. Assuming that you will retire at the age of 60, we have explored 5 different investment periods (in years) – 35, 30, 25, 20, and 15.

- The investment return rate. We have considered three rates here – 8%, 10%, and 12%. 8% is a very conservative estimate.12% is a more realistic scenario, if you allocate most of your savings in equities.

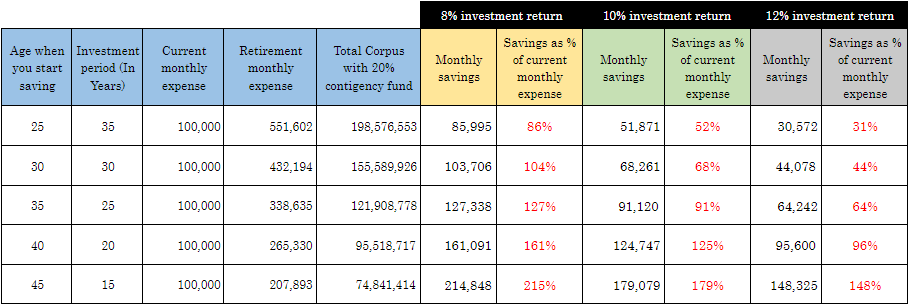

Well, most of the assumptions have been mentioned above. We have assumed that you have a monthly expense of 100,000 and computed your monthly retirement expense accordingly. We computed the retirement corpus required to fund your retirement expense, and then also baked in an additional 20% contingency fund into it. All these values are listed in the table below.

Finally, in the last 6 columns, you will find the monthly savings number. If you feel dizzy looking at so many numbers, just concentrate on the numbers highlighted in red. This is the amount you need to save as a percentage of your monthly expenses each and every month till you retire. This savings amount is in addition to your monthly expenses.

Time to have a closer look at these numbers.

Let’s start with the best-case scenario, where you start early and get to invest your savings for retirement at a higher rate of 12%. In this case, you will be required to save only 31% of your current monthly expenses. Keep in mind that these numbers are indicative. If you start before this, or your investment instrument delivers a higher return then you will end up with a higher corpus than required. This would give you an even bigger cushion in your old age.

Next, notice the different scenarios when you start a little late or invest at a lower rate of return. See how the savings requirement increases significantly with every 5 year block period. This increase is not linear.

Similarly, the required savings rate increases non-linearly as your rate of return decreases.

Both these factors are in your control. You can start as early as you want. But most of us won’t be thinking of retirement at such an early stage and by the time you start thinking about it seriously, you might have crossed the 30’s age barrier.

So, the next factor you could control is the investment return rate. Although you are free to choose your investment vehicle, there are no guaranteed returns. The risk of losses also looms larger for instruments that have historically given higher returns.

Another critical aspect to keep in mind is that you won’t have enough wiggle room if you start late and may be forced to go for safer instruments. If you start early, you will have time on your side and have more opportunities to invest in instruments (Mostly equity heavy) with higher returns. Because, even if the markets behave adversely in between, you will have enough time to recover.

Starting early also presents you the opportunity to rebalance your portfolio when required.

Now you know how much to save for retirement:

I hope that, by now you have a fair idea of how much you need to account for your retirement savings. Please note that these computations don’t include any big-ticket purchases like home or car. I touched upon the key factors and also showcased a few scenarios to show how a small change can significantly impact your savings requirement.

There are other factors as well, but you won’t have much control over them, so I have gone ahead with some assumptions that should mostly hold good. But if you feel that you need to adjust some of those levers then you can take a directional bet and adjust your savings.

The idea behind this article was not to give you an accurate figure for savings but to give you a fair estimate of the requirement. All I want is to get you to start thinking with the right perspective.

Happy planning !!!

Well I definitely enjoyed reading through it.

This subject offered by you is quite constructive for correct

organizing.