Updated on: November 12, 2020 ; Investments

SIP Overview:

This is the second part of the multi-series articles on SIPs where we analyze the midcap SIPs. Please read the first part of the SIP analysis on large caps(Sensex) here. In the first part, we analyzed the SIP CAGRs on BSE Sensex for different durations and different rolling windows. We understood how historic returns and their fluctuations vary under different scenarios. We will follow the same structure for midcaps in this article as well. So you can skip some text if you are comfortable jumping to the charts directly.

In this article, we will look at a similar analysis of SIPs on the BSE MidCap index. This index consists of companies with medium-size market capitalization.

SIPs for different durations and rolling windows:

We will look at the CAGRs for different SIP scenarios. To learn more about CAGR, read here. We have assumed that we invested 1000 rupees, at the beginning of every month, starting from April 2003 till October 2020. Please note that the time period is less compared to Sensex as this index was created much later than BSE Sensex.

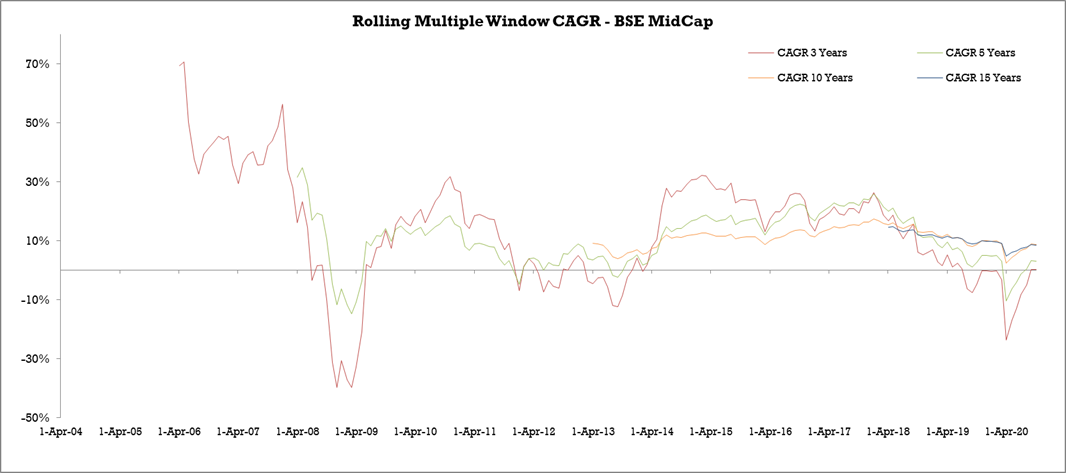

First, we will look at rolling window CAGRs for 5 different investment durations: 1 year, 3 years, 5 years, 10 years, and 15 years. This provides a good range of short-term to long-term investment scenarios. These CAGRs are computed for each month. The following two graphs show the CAGR trends of these five durations. We would have liked to fit all of them in a single graph. But the variation in the range was too large, especially for the first duration that we had to split them into two for better visual clarity.

You can notice the wide swings in the CAGRs over the years. Within this time period, the 1-year CAGR for midcap SIP touched the maximum of 147% and the minimum of -79.5%. Now, this is a very big range but expected based on what we have seen in the 1 year SIP CAGRs on Sensex. Now, let’s have a look at other durations.

Looking at the graph above we can clearly see that the volatility in the CAGRs reduces as the duration increases. You will notice that at different points, the shorter duration CAGRs have outperformed the longer duration ones by a big margin. But on the downside, they have also had bigger falls on many occasions.

The year-on-year performance of the longer duration SIPs may not look spectacular but they provide some sort of stability. But, is there any guarantee of stability? Do midcap SIPs behave differently than Largecap SIPs (Sensex SIPs)? To know this let’s look at the summary view of these midcap SIPs for different durations in the next section.

Summary view of CAGRs for different midcap SIP durations:

In this section, we analyze the maximum, minimum, and average CAGR returns from SIP durations ranging from 1 year to 15 years. The time period under observation is from April 2003 till October 2020. The 1-year SIP has the maximum number of data points: 199 points, starting from April 2004 1991 till October 2020. The 15-years SIP has the least number of data points: 31 points, starting from April 2005 till October 2018. The data points for 15-years SIP is on the lower side.

We wish we had more information. But, at this point, we will have to rely on this much information only, as there isn’t any more historical data on the midcap index.

Each bar represents the maximum and minimum CAGRs for the respective SIP duration. Notice how the spread or the range of CAGR narrows down as the SIP duration increases. This means lesser volatility for long-duration SIPs. Having said that, the range is still substantial for all the durations shown above.

Even the 15-year SIP has a big range of 10%. This means that even long durations SIPs are no guarantee for any kind of fixed returns. What your returns would be, will depend on when did you start your SIPs and at which point are you analyzing them.

The graphs above also tell you that SIPs of 9 years and above on the midcaps have at least given you positive returns in the last 17 years.

Let’s also look at average returns before wraping up this article.

The average numbers look very impressive. But they just tell you the good part of the story. The story is complete only when you combine this view with the range of CAGRs that we just discussed above. Again all of this is based on the limited data we have on the midcap index, this is even lesser than the Sensex data. Having analyzed this over more data points might have given slightly different numbers.

Reiterating the main point here – there are risks and volatilities associated with SIPs. SIPs are one of the popular ways of investing, but they too can’t guarantee positive returns all the time, leave alone superior returns (this needs another discussion).

Now, when you compare the charts with the ones on Sensex SIPs, you might come to the conclusion that Sensex SIPs have provided superior returns compared to the midcap SIPs, although Sensex SIPs may have shown higher volatility for some of the durations.

Well, the fact is that you cannot make that conclusion yet, as the time horizons are different. The Sensex SIP analysis had 30 years of data, whereas here we have just a little over 17 years of data. This article is to independently analyze the performance of the midcap index SIPs.

We will be talking about the smallcap SIPs as well, and then have a dedicated article where we will compare all the three analysis together.

Conclusion:

- SIP CAGRs become less volatile as your investment duration increases. Even in the case of longer duration SIPs the range can be quite broad.

- SIPs are no guarantee for superior returns at all points in time. There could be times when your SIP returns might be negative or much lower than savings bank account returns.

- Even a long duration can give you negative returns at certain times.

- Don’t expect extraordinary returns from SIPs, but reasonably good returns over long durations.

- Average returns don’t tell you what your actual returns could be at any given point in time. Average numbers hide much more than they reveal. Your actual SIP returns at any given point in time depend on the market level at that time.

We will continue this discussion on SIPs with other case studies on smallcaps. In the last part, we compare all the three cases. Click here to read the article on comparison.

Keep understanding your SIPs !!!

Data sourced from: https://www.bseindia.com/Indices/IndexArchiveData.html