Updated on: November 12, 2020 ; Investments

SIP as a strategy:

For starters, SIP or Systematic Investment Plan refers to the monthly (systematic part) investment of a dedicated amount of money into an asset (mostly mutual funds) for a long period of time (the spirit is for long periods but technically you can have SIPs for shorter durations).

In this multi-part series, we will be looking into how have SIPs performed in the Indian markets. We will analyze different scenarios as we add more articles to this series. In this first edition, we start by exploring the performance of large-cap stocks or large-cap mutual funds. For this, we have taken Sensex as a proxy for large-cap stocks. We will understand the performance of your investments along with the risks associated with it if any.

We will analyze different time durations and rolling windows of SIPs to understand the returns given by SIPs.

SIPs for different durations and rolling windows:

We will look at the CAGRs for different SIP scenarios. To learn more about CAGR, read here. We will analyze the BSE-Sensex, which is the benchmark index of BSE, and consists of the top 30 stocks by market capitalization. We have assumed that we invested 1000 rupees, at the beginning of every month, starting from January 1990 till October 2020.

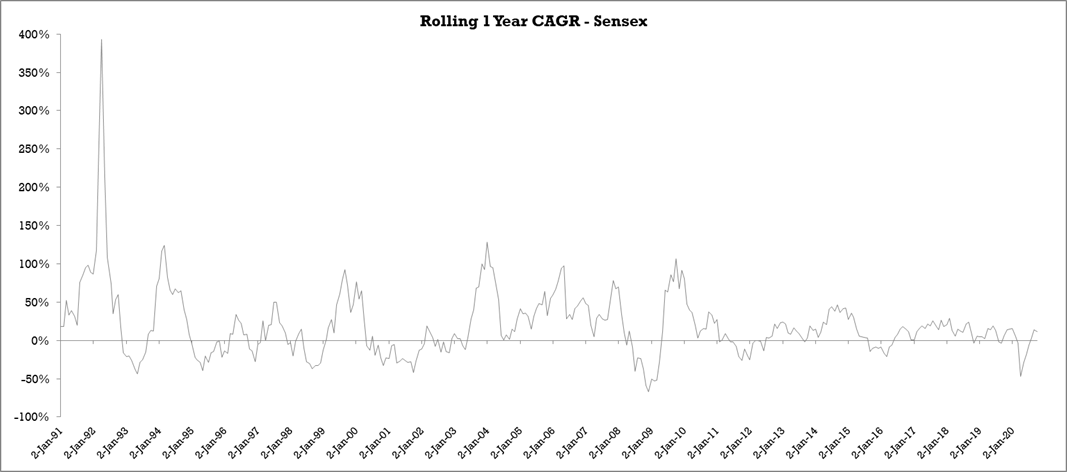

First, we will look at rolling window CAGRs for 5 different investment durations: 1 year, 3 years, 5 years, 10 years, and 15 years. This provides a good range of short-term to long-term investment scenarios. These CAGRs are computed for each month. The following two graphs show the CAGR trends of these five durations. We would have liked to fit all of them in a single graph. But the variation in the range was too large, especially for the first duration that we had to split them into two for better visual clarity.

Look carefully at the 1-year returns. Do you notice the wide swings? At one point in 1992, it almost touched a CAGR of 400%. You can also see several periods of ~100% CAGRs, which is great. But along with it, there are many instances of huge negative returns as well. These negative spikes are the real risks.

These negative spikes, many over -20% may seem small when compared to the 100%+ returns, but in reality, when someone has to live through them, they suffer much more pain than the exuberance of those high gains.

Overall, we can see a lot of volatility and no pattern whatsoever in this graph. You never know which part of the graph you might find yourself on a given day. But how does the story look for longer durations? To know more, let’s look at the other durations depicted in the graph below.

In the graph above, you can see the trends for four different durations. You can easily notice the difference in the volatility for these different durations. 3-year CAGR has the highest volatility and has some very big swings. Also notice that, as the duration increases the trends tend to become somewhat stable.

For example, if you had 4 investors who had completed their 3 years, 5 years, 10 years and 15 years SIPs on Jan 2008. They would be looking at astonishing CAGRs of 50.23%, 46.18%, 25.53%, and 19.14% respectively. These are staggering figures on their own and are very hard to achieve in the market.

But if we do a relative comparison, it might give the 3-years and 5-years investors a feeling of great accomplishment, and maybe some sense of ‘false’ superiority over the other two.

Now let’s fast forward to next year. Take another set of 4 investors who completed their SIPs of 3, 5, 10, and 15 years of Mar 2009. Their CAGRs would be -25.99%, -3.21%, 9.06%, and 7.95% respectively. This is the exact opposite of what we witnessed above.

In this case, the 3-years and 5-years investors would be very disappointed. In fact, many of them would leave the market forever. On the other hand, the 10-years and 15-years investors would be relieved to see their portfolios give decent returns, even during the time of such market crashes.

At times like these, your fixed income products like bonds, PPF, FD, and even your savings bank account would look very lucrative when compared to 3-years or 5-years SIPs. If you had not diversified your portfolio well enough, you would be at the complete mercy of the markets. Read more on diversification here.

Please note, these were just two extreme examples to highlight the fluctuations in the market and show how different investment durations can tell a very different story at different points in time. Each point on the graph has its own story. No would have been able to predict these SIP returns beforehand. But understanding the past is very important for any investor so that they can set their expectations right.

In the next section, we take a look at the summary view of a few more scenarios.

Summary view of CAGRs for different SIP durations:

In this section, we analyze the maximum, minimum, and average CAGR returns from SIP durations ranging from 1 year to 15 years. The time period under observation is from January 1990 till October 2020. The 1-year SIP has the maximum number of data points: 358 points, starting from January 1991 till October 2020. The 15-years SIP has the least number of data points: 190 points, starting from January 2005 till October 2020.

Each bar represents the maximum and minimum CAGRs for the respective SIP duration. Notice how the spread or the range of CAGR narrows down as the SIP duration increases. This means lesser volatility for long-duration SIPs. Having said that, the range is still substantial for all the durations shown above.

The lowest range is seen here is 16.3% for the 15-year SIP. This spread itself is very big. What this means is that, even after continuing your SIP for 15 long years, your returns could range from below-average returns of 5.8% to excellent returns of 19.1%. And all of this depends on when did you start your SIP.

Another crucial point to notice is that even 12-year durations SIPs have given negative returns at some point in time. Imagine, someone who invested for 12 long years in SIPs and still not able to match his invested amount, forget about inflation-beating returns.

So just continuing SIPs blindly is no guarantee of decent returns at all points of time. I am not against SIPs, I just want you to be aware of the realities of the SIP returns. The same SIPs that might be giving you negative returns today will turn profitable tomorrow, but there is no guarantee that it will remain profitable thereafter throughout.

So, the entry point of your investments also plays a crucial role. All of this analysis is based on past data of 30 years, which might seem too long. But in the financial world, even 30 years might not be long enough to fully understand the market performance. Before closing this article let’s have a look at the average returns for these durations.

The average numbers look very impressive. But they just tell you the good part of the story. The story is complete only when you combine this view with the range of CAGRs that we just discussed above. Again all of this is based on the limited data we have on Sensex. Having analyzed this over more data points might have given slightly different numbers.

But that is not the point. The moot point here is not about the exact return figures, but the risks and the volatilities associated with SIPs. SIPs are one of the popular ways of investing, but they too can’t guarantee positive returns all the time, leave alone superior returns.

Conclusion:

- We have seen that SIP CAGRs become less volatile as your investment duration increases. Even in the case of longer duration SIPs the range can be quite broad.

- SIPs are no guarantee for superior returns at all points in time. There could be times when your SIP returns might be negative or much lower than savings bank account returns.

- Even a long duration can give you negative returns at certain times.

- Don’t expect extraordinary returns from SIPs, but reasonably good returns over long durations.

- Average returns don’t tell you what your actual returns could be at any given point in time. Average numbers hide much more than they reveal. Your actual SIP returns at any given point in time depend on the market level at that time.

We will continue this discussion on SIPs with other case studies on midcap and smallcaps. In the last part, we compare all three cases. Click here to read the article on comparison.

Understand your SIPs first !!!

Data sourced from: https://www.bseindia.com/Indices/IndexArchiveData.html