Updated on: May 27, 2021 ; Investments

Background:

One of the simplest ways to invest in stocks is through an Index fund. These are passive funds with lower costs and give you ‘near’ market-level returns. But is there a way to perform better than the Index? We will try to answer this question in a series of articles by adopting few different investment strategies with a portfolio of stocks. We start with an equal-weighted portfolio of stocks in this article.

Here, we will construct an equal-weighted portfolio of stocks and compare its performance with the Index. Now there are many different ways to construct a portfolio, and equal-weights is just one of the many. While we concentrate on the equal-weighted portfolio in this article, we will be looking at many more ways of portfolio construction in the articles to follow.

Portfolio selection:

To start with, we will have to choose an index. What else could be a better choice than India’s first equity index – S&P BSE Sensex. It was first launched in 1986, with the base year being 1978-79. It was constituted of the 30 largest companies of that time. Most of them were industrial companies with no presence of any bank or technology companies.

But this composition kept changing with time. If you were to look at the Sensex in 2000, or 2008, or 2020, you would see very big differences.

As market conditions and business outlook change over time, the stock prices of different companies react differently. This results in the need for reconstituting Sensex as the market capitalization of companies rise and fall. There are some stringent criteria that the companies need to fulfil to be considered Spart of Sensex. We won’t be dwelling into that here. All we need to know is that market capitalization is the most important deciding factor.

Since we plan to study the performance of an equal-weighted portfolio of stocks vs Sensex, to be fair, we need to choose our stocks from Sensex. But, given the volatility of the Sensex itself, it might be a bit challenging to do the stock selection. The ideal way would be to pick your stocks based on strong fundamentals and thorough research. But for the sake of simplicity and unbiasedness, we will be using some very elementary rules to construct our portfolio.

Before we get into the details of portfolio selection, let’s talk about the timelines a bit.

We plan to do a long term study of our equal-weighted portfolio. Well, if you have been following me, then all my studies have been long term. So nothing surprising here. For this, we have taken the investment period to be from March 2003 till March 2021, 18 years.

But choosing a portfolio of stocks for investment in 2003 while standing today in 2021 won’t be fair. Today we have the luxury of knowing the past performance of all the stocks. So any stock selection won’t be completely bias-free. We can rephrase this as – we can never be too sure of ruling out any bias if we construct an equal-weighted portfolio of stocks for 2003 in 2021.

To keep this study unbiased, we will take the help of simple heuristics or rules. There can be many rules one may apply. We will be applying one such simple rule in this study. More on this rule in the next paragraph.

I have already mentioned that Sensex has undergone many changes since its inception. So we decided to construct an equal-weighted portfolio with stocks that survived to remain in the Sensex for a long time. This would mean that these stocks have some sort of robustness and strong fundamentals built in them.

For this, we started with the 30 stocks that were part of the original Sensex (1986). Then we looked at the stocks that had the biggest market capitalization in March 2003. Next, we picked up the common stocks from both these lists to construct our equal-weighted portfolio. These were the stocks that remained in the top 30 slots even after 17 years.

You may ask that why did we choose 2003 and not any other year. Actually, we could have chosen any other year as well. One reason for choosing this year is that I found the data for this year easily.

Methodology for equal-weighted portfolio:

In the last section, we discussed the rationale behind the stock selection. Putting that in action, we found the stocks that were part of Sensex in 1986 and were also in the list of top 30 stocks by market capitalization in 2003. These are:

- Reliance Industries

- Hindustan Unilever

- ITC

- Nestle India

- Tata Motors

- Hindalco

- Tata Steel

- Larsen & Toubro

This list is in the order of their market capitalization in March 2003, with Reliance Industries having the largest market capitalization.

We will be analysing two scenarios in this first part of the multi-part series on stock portfolio investment strategy. As you already know, this part is dedicated to an equal-weighted portfolio, so both scenarios will have equal-weighted portfolios.

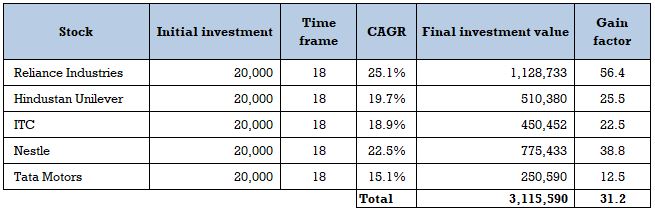

In the first scenario, we construct our portfolio with the top 5 stocks only. That means the first portfolio (Scenario 1a) consists of Reliance Industries, Hindustan Unilever, ITC, Nestle India, and Tata Motors.

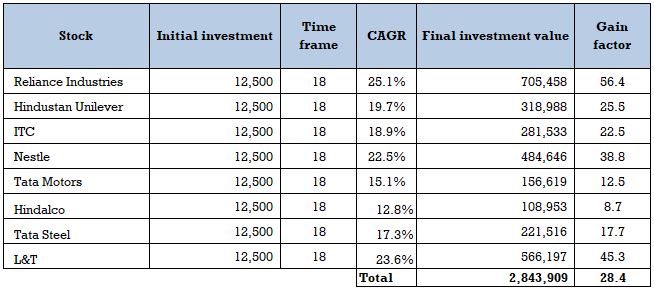

The second portfolio (Scenario 1b) consists of all the 8 stocks listed above.

Now, we have an understanding of the stock selection criteria and the different scenarios that we will be exploring here. But one question still remains unanswered. What does an equal-weighted portfolio mean?

It won’t be difficult to guess. I am sure most of you would have guessed it correctly already. Equal-weighted means that we invest an equal amount of money in each stock in our portfolio.

Other things to note is that we are looking at a one-time investment with no withdrawals and no balancing. It is -> fill-it, shut-it and forget-it type of investment. We allocate an equal sum of our corpus to each stock in march 2003 and let it remain as such till march 2021.

There are no adjustments or fund re-allocations between these stocks anytime in between. This is what I meant by no balancing.

We do not add any more funds either. That is what we call a one-time investment or lumpsum investment.

Now, going into specifics. We assume that we had a corpus of 100,000 rupees to start in March 2003. So in ‘Scenario 1a’ where we picked 5 top stocks, we allocate 20,000 rupees to each stock. And in ‘Scenario 1b’ where there are 8 stocks, each stock gets 12,500 rupees as the initial investment.

We compare both these scenarios with the third case. This third case serves as the base case, where the entire 100,000 rupees is invested in the broad index, i.e. Sensex.

One callout – we have assumed that the allocated amount for each stock is fully utilized. Let me explain it with an example to make it clear.

In March 2003, one share of Reliance Industries was priced at 35 rupees (adjusted price). So, if one were to invest 20,000 rupees in Reliance Industries, he/she would be able to buy 563.49 shares. But this is not possible in the real world, as you cannot buy a fraction of a share. It has to be a whole number.

But this hardly makes any difference to our analysis as the fractions are very small. So we have ignored such constraints. We have assumed that fractional purchases are possible. And this assumption will remain true for the other parts of this series as well.

Now, it is time to go to the analysis.

Comparative study:

Take a look at the tables below. They summarize the final investment values of the Sensex and the two scenarios as of March 2021. I have also provided the stock-wise break-up for both scenarios.

What we see here is that both the scenarios have exceedingly performed well than the Sensex. The final investment value is almost double in the case of the stock portfolios. It seems a carefully curated equal-weighted portfolio of stocks has the potential to significantly outperform the benchmark index.

You should also notice that not all stocks performed equally in the portfolio. Even though all started with an equal share within in portfolio, they all ended up very differently after 18 years.

Stocks like Reliance Industries, L&T, and Nestle India have grown at a very high pace. So, if we were to create a portfolio with just these three stocks, the final investment value would be much higher. It is easy to make such statements now because we know what has happened. But standing in 2003, there was no way anyone could have predicted these outcomes. I repeat, NO ONE could have predicted these outcomes.

Another point to be noted is that only one stock in Scenario 1a (Tata Motors) underperformed the Sensex. In the case of Scenario 1b, only two stocks (Tata Motors and Hindalco) underperformed the Sensex.

The point I am trying to make is that it is impossible to accurately predict the performance of individual stocks. This is true for both short-term and long-term investment time horizons. But a portfolio of ‘good stocks’ has a much higher chance of outperforming the Index.

You need to diversify your portfolio across quality financial assets. In this case, you diversify across quality stocks. Some will perform much better than others, and some might not even give you market-level returns. But overall, a ‘solid portfolio’ will, in all probability give you higher returns than the market in the long run.

Let’s get back to the tables once more. We see that the performance of the 5-stocks portfolio is better than the 8-stocks portfolio. But can we infer that a 5-stocks portfolio or a smaller portfolio will always perform better than an 8-stock portfolio or large portfolio?

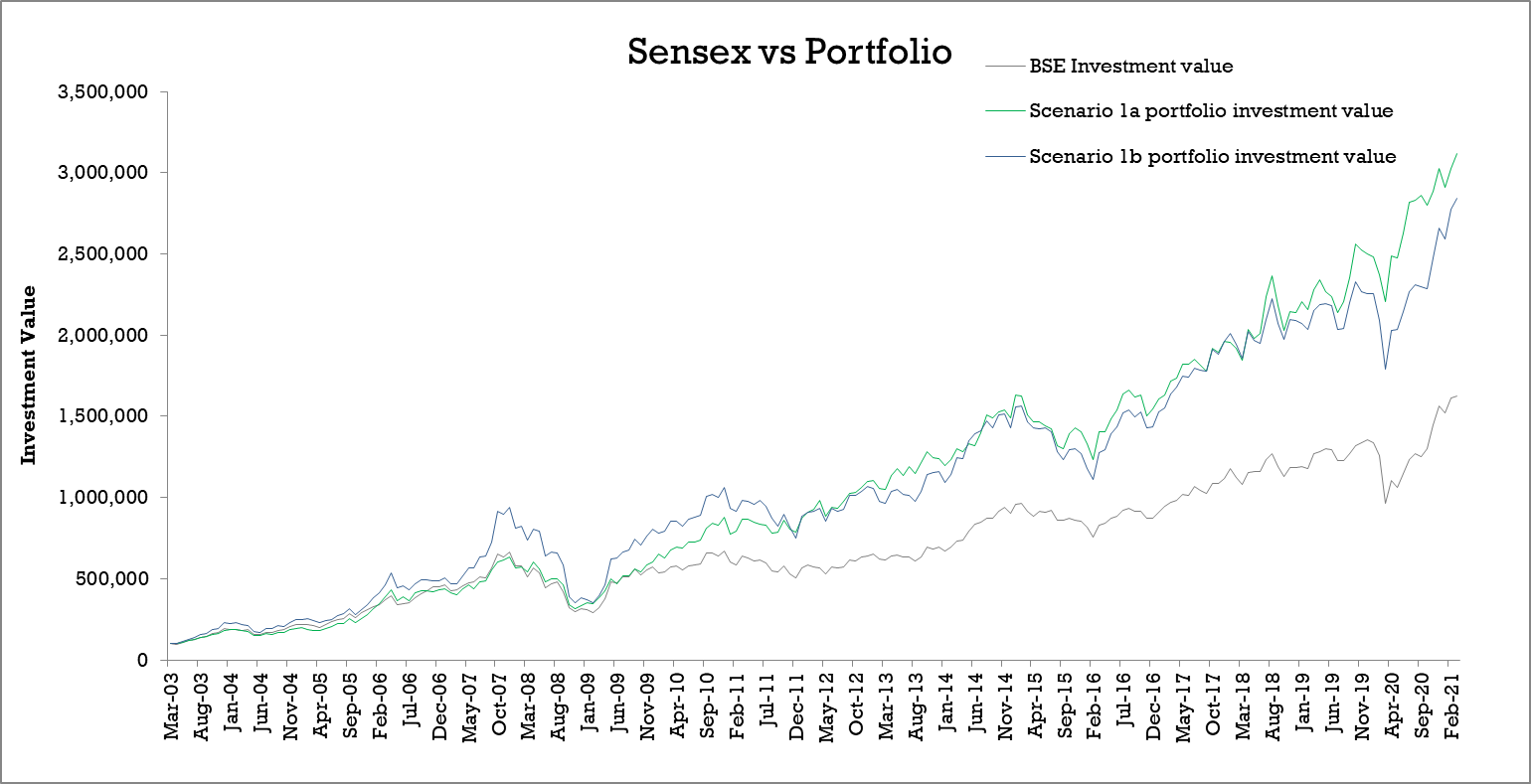

The data in the table is not enough to draw any such inference. To answer this question, let’s look at another set of numbers. This time we will be looking at a chart.

The chart captures the monthly value of your investments for the 18-year investment period. It is very clear from the chart that the order of performance is not consistent throughout the time period. There were many instances like the time period between 2003 and 2011 where Scenario 1b performed better than Scenario 1a. Then there were other times when Scenario 1a performed better.

Even if the two portfolios keep changing their positions, they have consistently performed better than the Sensex most of the time. And this gap widens significantly after 2009.

Now, this analysis is based on just one starting point, i.e. March 2003. We need to do similar analyses for multiple starting points to make a concrete inference. But we can safely say that in a long term investment time frame, an equal-weighted portfolio will outperform the index most of the time.

Final remarks:

We have seen that an equal-weighted portfolio of stocks has performed better than the index over a long period of time. The index itself went through many changes during this period. But sticking with a focused set of limited stocks proved to be far more beneficial. This study is Not conclusive and only indicative.

The performance of a portfolio depends a lot on its constituents. We tried to create a portfolio based on a very basic set of rules to eliminate any biases. We also stuck with the biggest stocks in the market. But you can make your own portfolio using your own set of rules and criteria.

I would urge all of you to make your own portfolios based on your judgement. The rule I used was to illustrate the benefits of an equal-weighted portfolio. It is by no means the best or the recommended method for portfolio construction.

Here we conclude the first part of stock portfolio investment strategies. We will be looking at many different ways of portfolio construction and investment strategies in the upcoming parts.

Pick your stocks well !!!