Updated on: May 29, 2021 ; Investments

Background:

This article is the third in the series of articles on stock portfolio investment strategies. Today, we will be looking at the equidistant-weighted portfolio of stocks and measure their performance against the Sensex.

We have already looked at the equal-weighted portfolio and marketcap-weighted portfolio, in the previous articles and will be covering more stock portfolio creation strategies in the following articles.

Portfolio selection:

We follow the same logic that was followed in the previous article here. So we won’t be going into great details explaining the whole logic of stock selection. Please refer to the previous article and go to the ‘portfolio selection’ section to understand the details. We will only revisit the key points in this article. Readers familiar with the logic can skip this section.

We choose BSE Sensex as the index to represent the market. Since we will be creating an equidistant-weighted portfolio of stocks and compare it with the index, we will be choosing our list of stocks from Sensex itself.

We apply a simple rule to pick the list of stocks. We choose the stocks that were part of the original Sensex in 1986 and were also in the list of top 30 stocks by market capitalization in March 2003. This makes the stock selection process free from any bias.

Once we get the list of stocks, we create our equidistant-weighted portfolio in march 2003. Next, we track the performance of this portfolio till march 2021. Now, let’s understand which are these stocks and how do we create our equidistant-weighted portfolio out of these stocks.

Methodology for equidistant-weighted portfolio:

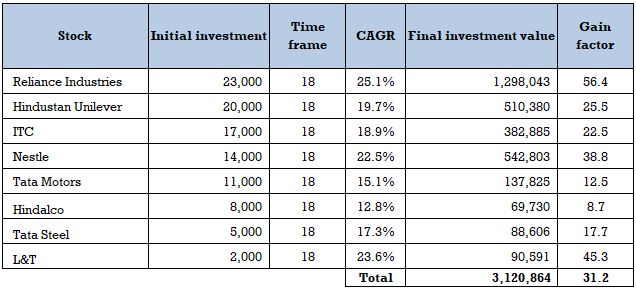

You will find many similarities in this section with the corresponding section in the previous article. Readers familiar with this section can skip the first 6 paragraphs. In the last section, we discussed the rationale behind the stock selection. Putting that in action, we found the stocks that were part of Sensex in 1986 and were also in the list of top 30 stocks by market capitalization in 2003. These are:

- Reliance Industries

- Hindustan Unilever

- ITC

- Nestle India

- Tata Motors

- Hindalco

- Tata Steel

- Larsen & Toubro

This list is in the order of their market capitalization in March 2003, with Reliance Industries having the largest market capitalization.

We will be analysing two scenarios in this second part of the multi-part series on stock portfolio investment strategy. As you already know, this part is dedicated to an equidistant-weighted portfolio, so both scenarios will have equidistant-weighted portfolios.

In the first scenario, we construct our portfolio with the top 5 stocks only. That means the first portfolio (Scenario 3a) consists of Reliance Industries, Hindustan Unilever, ITC, Nestle India, and Tata Motors.

The second portfolio (Scenario 3b) consists of all the 8 stocks listed above.

Now, we have an understanding of the stock selection criteria and the different scenarios that we will be exploring here. But one question still remains unanswered. What does an equidistant-weighted portfolio mean?

This would need a little bit of explaining. Each stock gets a different allocation of funds, and the gap in the amount invested between subsequent stocks is equal. There is an equal stepwise increment of funds as we go from the lowest market cap stock to the highest. Here, the stock with the highest market cap gets the biggest share.

In Scenario 3a, the stepwise increment is kept at 5% of the whole investment corpus. In Scenario 3b, this is kept at 3%.

Other things to note is that we are looking at a one-time investment with no withdrawals and no balancing. We allocate the amount to each stock in march 2003 and let it remain as such till march 2021.

There are no adjustments or fund re-allocations between these stocks anytime in between. This is what I meant by no balancing.

We do not add any more funds either. That is what we call a one-time investment or lumpsum investment.

Now, going into specifics. We assume that we had a corpus of 100,000 rupees to start in March 2003. So in ‘Scenario 3a’, this amount was distributed among the top 5 stocks. And in ‘Scenario 3b’, it was distributed among 8 stocks. The exact distributions are provided in the tables below.

Readers familiar with this section can directly go to the next section.

We compare both these scenarios with the third case. This third case serves as the base case, where the entire 100,000 rupees is invested in the broad index, i.e. Sensex.

One callout – we have assumed that the allocated amount for each stock is fully utilized. Let me explain it with an example to make it clear.

In March 2003, one share of Reliance Industries was priced at 35 rupees (adjusted price). So, if one were to invest 30,000 rupees in Reliance Industries, he/she would be able to buy 857.41 shares. But this is not possible in the real world, as you cannot buy a fraction of a share. It has to be a whole number.

But this hardly makes any difference to our analysis as the fractions are very small. So we have ignored such constraints. We have assumed that fractional purchases are possible. And this assumption will remain true for the other parts of this series as well.

Now, it is time to go to the analysis.

Comparative study:

Take a look at the tables below. They summarize the final investment values of the Sensex and the two scenarios as of March 2021. You can also see the stock-wise break-up for both scenarios.

What we see here is that both the scenarios have exceedingly performed well than the Sensex. The final investment value is more than double in the case of scenario 3a. It seems a carefully curated equidistant-weighted portfolio of stocks has the potential to significantly outperform the benchmark index. You can skip the next 7 paragraphs if you have gone through the previous articles in this series.

You should also notice that not all stocks performed equally in the portfolio. The proportion of each stock ended up very differently after 18 years, compared to their start.

Stocks like Reliance Industries, L&T, and Nestle India have grown at a very high pace. So, if we were to create a portfolio with just these three stocks, the final investment value would be much higher. It is easy to make such statements now because we know what has happened. But standing in 2003, there was no way anyone could have predicted these outcomes. I repeat, NO ONE could have predicted these outcomes.

Another point to be noted is that only one stock in Scenario 3a (Tata Motors) underperformed the Sensex. In the case of Scenario 3b, only two stocks (Tata Motors and Hindalco) underperformed the Sensex.

The point I am trying to make is that it is impossible to accurately predict the performance of individual stocks. This is true for both short-term and long-term investment time horizons. But a portfolio of ‘good stocks’ has a much higher chance of outperforming the Index.

You need to diversify your portfolio across quality financial assets. In this case, you diversify across quality stocks. Some will perform much better than others, and some might not even give you market-level returns. But overall, a ‘solid portfolio’ will, in all probability give you higher returns than the market in the long run.

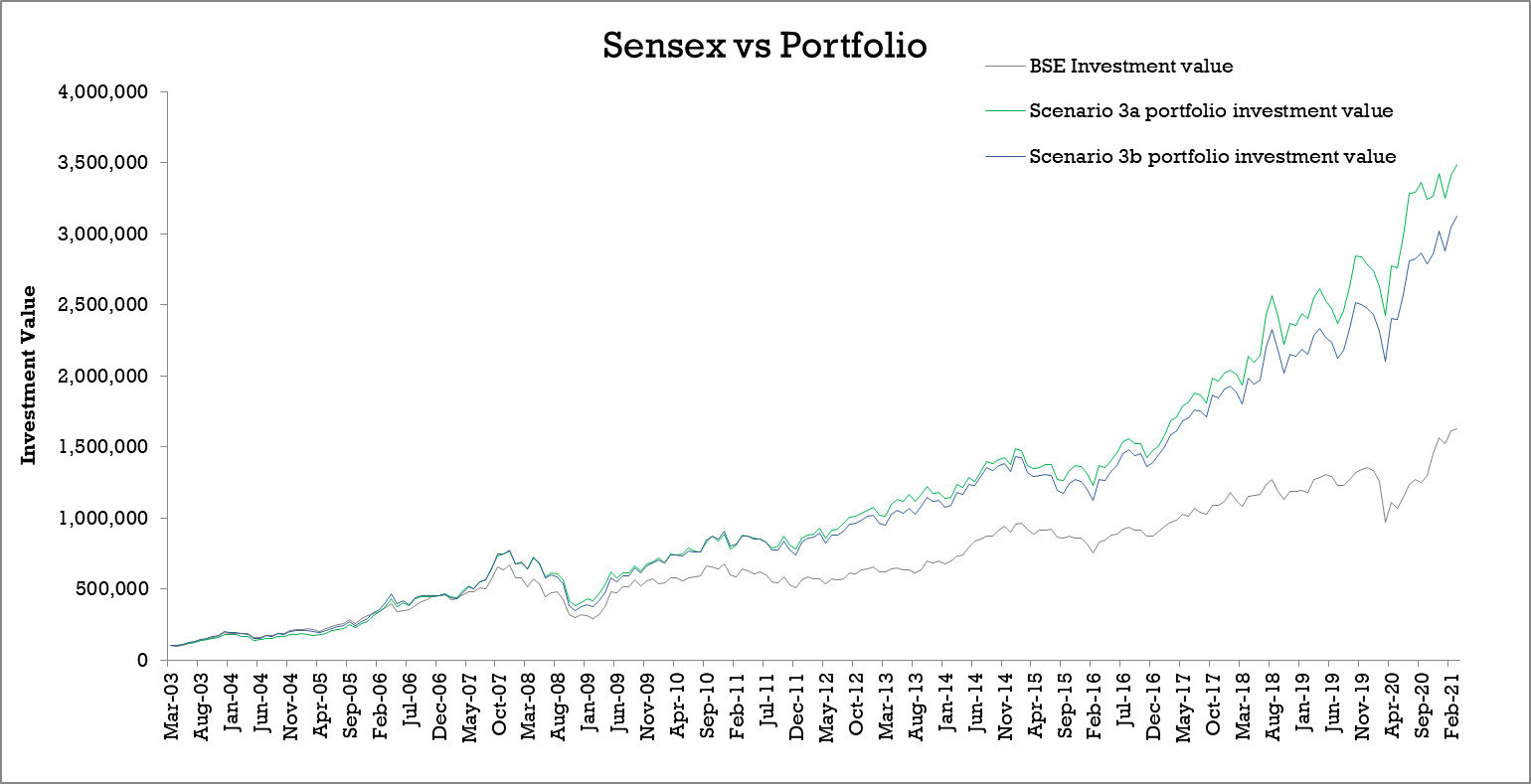

Let’s get back to the tables once more. We see that the performance of the 5-stocks portfolio is better than the 8-stocks portfolio with a marginal difference. But can we infer that a 5-stocks portfolio or a smaller portfolio will always perform better than an 8-stock portfolio or large portfolio?

The data in the table is not enough to draw any such inference. To answer this question, let’s look at another set of numbers. This time we will be looking at a chart.

The chart captures the monthly value of your investments for the 18-year investment period. You can see from the charts that scenario 3a seems to be a little ahead of scenario 3b for most of the investment period.

Now, this analysis is based on just one starting point, i.e. March 2003. We need to do similar analyses for multiple starting points to make a concrete inference. But we can safely say that in a long term investment time frame, a marketcap-weighted portfolio will outperform the index most of the time.

Final remarks:

We have seen that an equidistant-weighted portfolio of stocks has performed better than the index over a long period of time. The index itself went through many changes during this period. But sticking with a focused set of limited stocks proved to be far more beneficial. This study is Not conclusive and only indicative.

This strategy has performed better than the equal-weighted portfolio during this time period, but worse than the marketcap-weighted portfolio. But no one knows what will work better in future.

The performance of a portfolio depends a lot on its constituents and how you diversify your corpus across it. I urge all of you to make your own portfolios based on your judgement.

Here we conclude the third part of stock portfolio investment strategies. We created our portfolio out of stocks based on the Sensex constituents in 1986 and 2003. In the next three articles we will be looking at the the same portfolio creation methodologies, but with a different portfolio selection strategy.

Stay tuned !!!