Updated on: June 8, 2021 ; Investments

Background:

So far, we have already covered five stock portfolio investment strategies. Today we are going to cover the sixth strategy. The first three articles followed a common principle of portfolio selection. The next three, including this one, follow a different portfolio selection strategy. This one would be part 2 of the equidistant weighted portfolio of stocks. Consider this to be a continuation of the previous article on equidistant weighted portfolio with a change in the stock selection process.

I request you to please read through the previous articles on portfolio creation. Here are the links for the same: link1, link2, link3, link4, and link5. This will help you understand the general progression of the slight differences in the strategies and comprehend the nuances better. If you already read through part 2 of the equidistant-weighted portfolio, then you can skip the next section.

These articles will feel repetitive for most of the part as there are a lot of common themes across them. But it is also equally necessary to touch upon the key elements in each article. So if you have been following the previous articles, then you would know which parts to skip and jump to the main section directly.

Potrfolio selection:

This is the section where this strategy differs from the first three strategies. There we had picked up the stocks that were part of the original Sensex (in 1986) and were still in the Sensex 18 years later (in 2003). This took care of choosing the companies that had stood the test of time and had shown some resilience. This implied that most of them have strong fundamentals and a better chance of surviving the next few decades.

But what we might have missed out on is the chance of tapping into new-age companies that did not exist during the initial days of Sensex and maybe have a better chance of compounded growth in the future. For instance, there were no technology companies or banks in the original Sensex.

So, in this article, we will shortlist our portfolio of stocks from the Sensex of 2003 only. We would be looking back at no other year for this. The 30 stocks in the Sensex of 2003 would be our sole bucket of stocks to choose from.

So, to keep the stock selection unbiased, we will use some very basic rule for the creation of our equidistant weighted portfolio. We simply choose the top stocks of Sensex by market capitalization, as of March 2003.

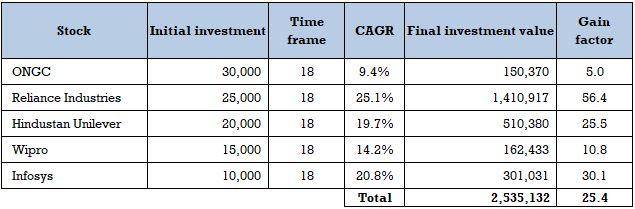

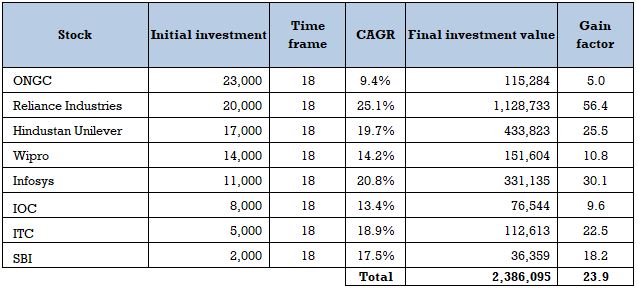

Following the same trend as earlier, we will be analysing two scenarios. In the first scenario (Scenario 6a), we choose the top 5 stocks, and in the second scenario (Scenario 6b), we choose the top 8 stocks. These are chosen based on the market capitalization of the stocks.

Methodology for equidistant weighted portfolio:

If you have read my previous articles, then after looking at the list of the shortlisted stocks you can directly go to the next section. Below is the list of the top eights stocks of Sensex as of March 2003.

- ONGC

- Reliance Industries

- Hindustan Unilever

- Wipro Limited

- Infosys Technologies

- Indian Oil Corporation

- ITC

- State Bank of India

The first 5 stocks will be part of the equidistant weighted portfolio in scenario 6a. And all 8 stocks will form the portfolio in scenario 6b.

In an equidistant weighted portfolio, each stock gets a different allocation of funds. And the gap in the amount invested between subsequent stocks is equal. There is an equal stepwise increment of funds as we go from the lowest market cap stock to the highest. Here, the stock with the highest market cap gets the biggest share.

In Scenario 6a, the stepwise increment is 5% of the whole investment corpus. In Scenario 6b, this increment is 3%.

Other things to note is that we are looking at a one-time investment with no withdrawals and no balancing. We allocate the amount to each stock in march 2003 and let it remain as such till march 2021.

There are no adjustments or fund re-allocations between these stocks anytime in between. This is what I meant by no balancing.

We do not add any more funds either. That is what we call a one-time investment or lumpsum investment.

Now, going into specifics. We assume that we had a corpus of 100,000 rupees to start in March 2003. So in ‘Scenario 6a’, this amount was distributed among the top 5 stocks. And in ‘Scenario 6b’, it was distributed among 8 stocks. The exact distributions are provided in the tables below.

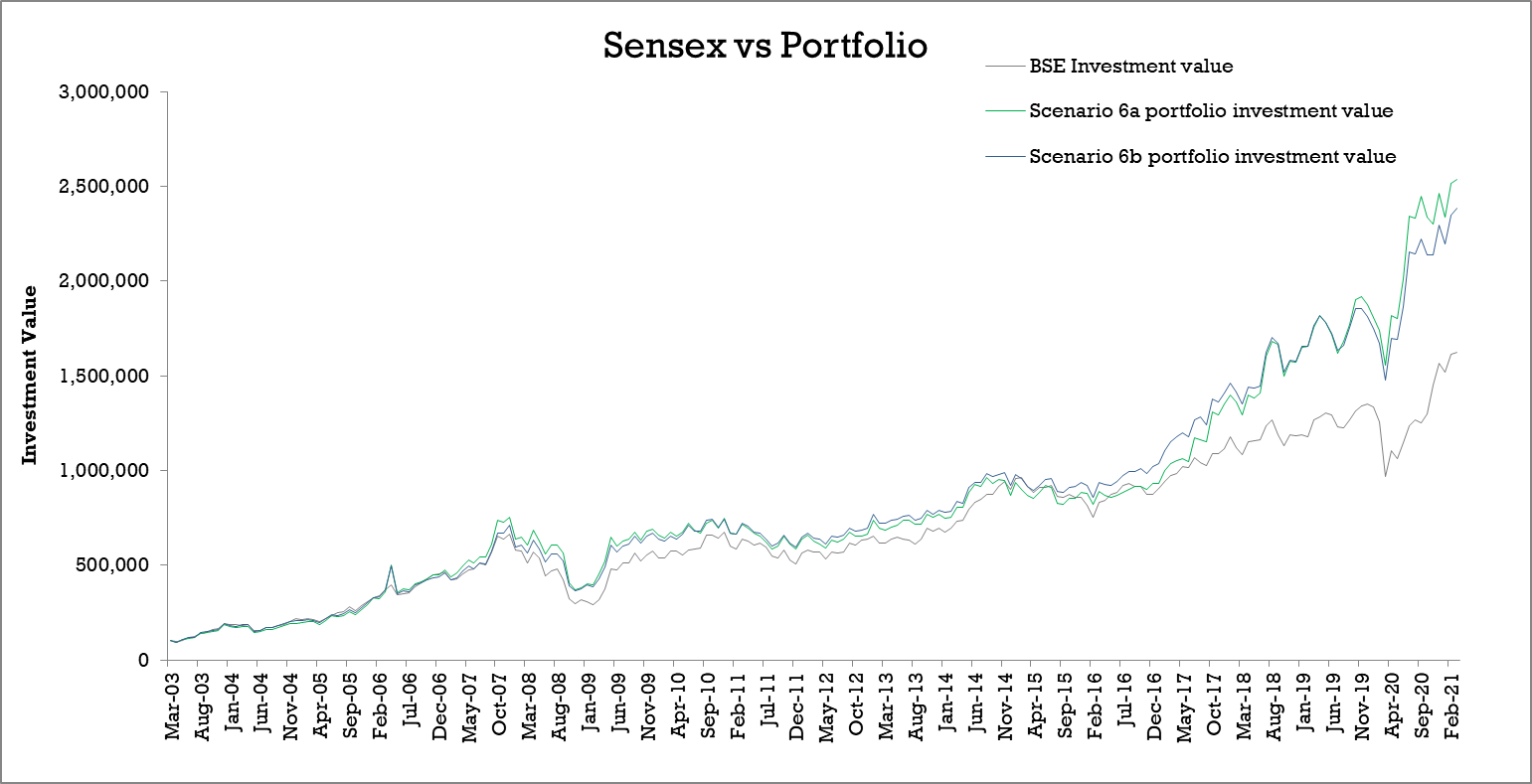

We compare both these scenarios with the third case. This third case serves as the base case, where the entire 100,000 rupees is invested in the broad index, i.e. Sensex.

Now, it is time to go to the analysis.

Comparative study:

Take a look at the tables below. They summarize the final investment values of the Sensex and the two scenarios as of March 2021. You can also see the stock-wise break-up for both scenarios.

As observed in previous cases, both the equidistant weighted portfolios have performed better than the Sensex. Although, not all stocks performed equally in the portfolio.

Also, note that the biggest stock of 2003 performed the worst in these 18 years. This shows that merely being big is no guarantee to success. In fact, ONGC was majorly responsible for dragging down the performance of both portfolios. The star performers were Reliance Industries, Infosys and Hidustan Unilever.

Now, compare this analysis with its predecessor. Please compare the tables from both the strategies side by side. Scenarios 3a and 3b have shown much better performance in this case. That is because the new stocks that replaced the old ones had lower CAGRs.

But, that may not be the case always. Maybe some other start year would have shown more promising results. Maybe a mix of both strategies would have yielded better results. Who knows?

Moving on, we will look at the chart that shows the monthly performance of the scenarios.

For most of the investment period scenario 6a and 6b run very close to each other. It is only in the last one and a half year that scenario 6a overtakes scenario 6b. If you look closely, you will notice that for a long period, both scenario 6a and 6b were very close to or below Sensex. There was not much difference between the three.

Things turned out to be better finally in the last few years but it would have left many investors anxious for a good 13-14 years. But, I do feel that this is NOT the best equidistant weighted portfolio strategy. The one we explored in the third article (Scenarios 3a and 3b) seems to be a better bet than this one.

Final remarks:

We saw the performance of the portfolios outperform the Sensex. They definitely have an edge over the Index. But at times, these scenarios underperformed the Index. We cannot say anything conclusively about this strategy until we explore more iteration with different start periods.

But if you plan to create an equidistant weighted portfolio of stocks, be very cautious with the stock selection. Do Not just rely on the current market leaders. Try to pick stocks that have been in the top position for some time and have a better prospect.

Overall, this strategy of portfolio selection is NOT the best. All the three portfolio allocation strategies with this portfolio gave inferior returns compared to the previous portfolio selection (Scenarios 1, 2 and 3).

This article tells you how NOT to create an equidistant weighted portfolio of stocks. We will look at the other strategies with a twist and see how worse or better they perform compared to other strategies discussed so far.

Stay tuned for more !!!