Updated on: November 25, 2020 ; Investments

Introduction:

In this second series of studies on SIPs, we look at the SIPs for three caps (large, mid and small) once again. But this time with a different perspective, as it is critical to analyze all possible aspects before investing. In this article, the focus would be on largecap SIPs. We will cover midcaps and smallcaps in the upcoming articles. Before we proceed further, a quick mention of the other SIP studies done before.

We have already studied the performance of SIPs in largecaps, midcaps, smallcaps in detail. Please read them as well. We also compared all of them in a single dedicated article. Click here to read the comparison. There we looked a CAGRs of SIPs for different rolling windows with all possible starting points in the last 15-30 years. The focus was on the average as well as the range of returns. It provided a very broad sense of SIPs performance.

But in this second series, we will analyze specific scenarios and cases. We will simulate situations where an investor might find him/her after staying invested in largecap SIPs for different time periods. This will help you appreciate the effects of investment duration and investment start time much better.

We will achieve this by fixing the evaluation point of your SIPs and have different investment start time in the various scenarios. Let’s have a look at the background of the data and the approach before we start our largecap SIPs analysis.

Background on largecap SIPs:

As done earlier for the largecap SIPs, we have considered BSE Sensex as our proxy. We will compare the SIP performance of different investment durations in our study.

The idea is to simulate some probable situations that largecap SIP investors might find themselves in. For this, we have assumed that the investor is evaluating his/her SIP investment on November 2nd, 2020. But we will evaluate many different scenarios and each scenario will have a different SIP start date. We will be covering a big range of short-term and long-term investment durations here.

Since the Sensex data is available from Jan 1990, so our first scenario is the one where the investor starts his SIP investments from Jan 1990 and continues it till Oct 2020. The investor makes a monthly investment of 1000 rupees at the start of every month without missing any payment in between.

The next scenario would be, where the investor starts his SIP investments from next year, i.e. Jan 1991. So each scenario represents a new SIP, starting in January of each year. This will continue till the year 2020. This leaves us with a total of 31 scenarios, ranging from 1990 till 2020. So the longest investment duration is for 30 years and 10 months, and the shortest one is for 10 months only.

In this article, we will look at these 31 SIP scenarios based on the actual Sensex levels. In addition to that, we will also look at a few hypothetical cases to simulate returns at different Sensex levels on the evaluation date.

Largecap SIPs cases explained:

We will be analyzing a total of six cases here. Each one of them will have the 31 SIP scenarios in them. Let’s briefly define these different cases first.

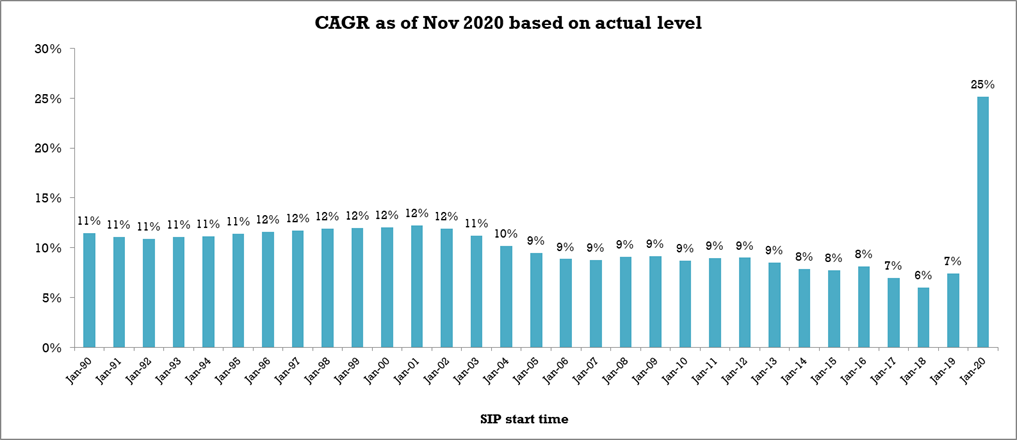

- Sensex at the actual level: CAGRs computed based on the actual level of Sensex (39,758) on November 2, 2020.

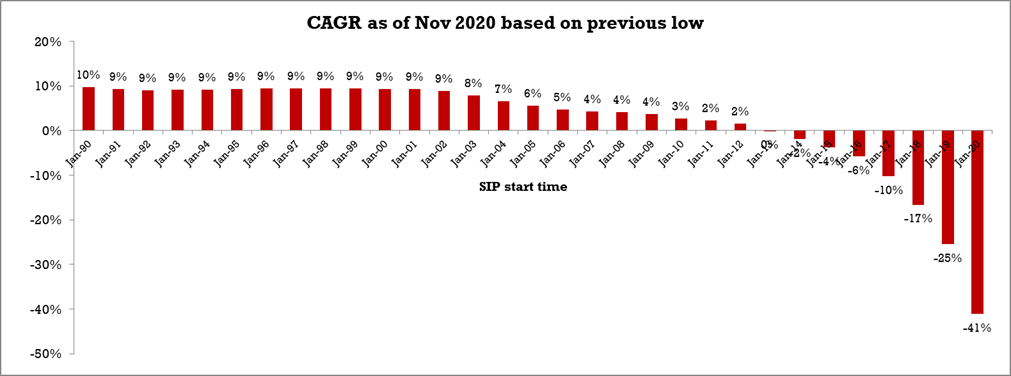

- Sensex at previous low: CAGRs computed based on the hypothetical case, where Sensex equaled the previous low level (in the last 12 months). In this case, it is 28,265 recorded on April 1, 2020. The actual lowest was in March, but since we are taking the data at the start of each month, this is the data point we will be using in our analysis. It is 29% lower than the actual level.

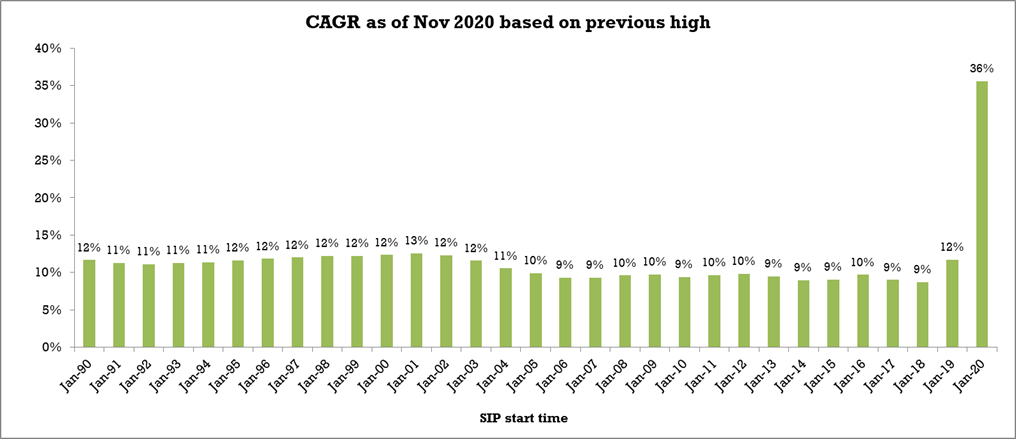

- Sensex at previous high: CAGRs computed based on the hypothetical case, where Sensex equaled the previous high level. In this case, it is 41,306 recorded on January 1, 2020. This is 4% higher than the actual level, not much of a difference here.

- Sensex at last 12-month average: CAGRs computed based on the hypothetical case, where Sensex is at the level of the last 12 months’ average. This level is 36,949, 7% lower than the actual level.

- Sensex at last 24-month average: CAGRs computed based on the hypothetical case, where Sensex is at the level of the last 24 months’ average. This level is 37,189, 6.5% lower than the actual level.

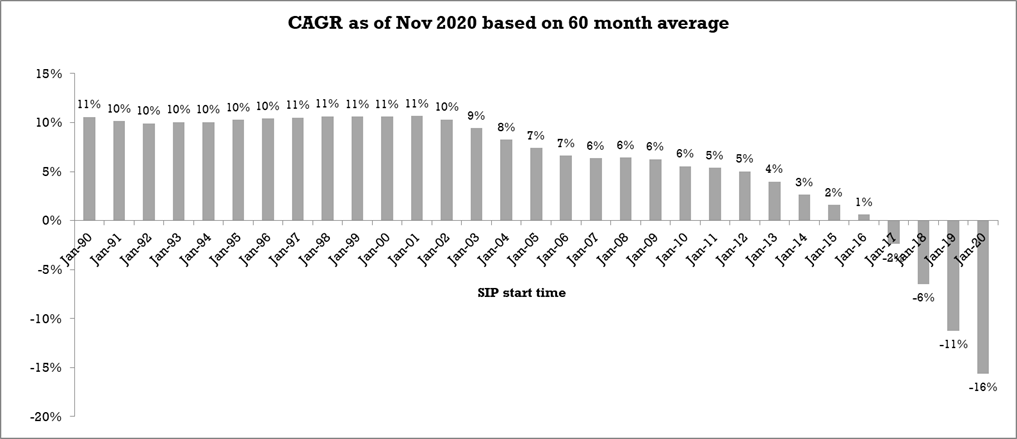

- Sensex at last 60-month average: CAGRs computed based on the hypothetical case, where Sensex is at the level of the last 60 months’ average. This level is 33,118, 16.7% lower than the actual level.

Largecap SIPs cases analyzed:

Now, it’s time to look at the data and observe how the returns would look like for the different scenarios within various cases. Just a reminder before we start. We are looking at all these scenarios as of November 2020. All the scenarios have different starting points for their SIPs but they all have the same evaluation point.

We will start in the same order as mentioned above. So, let’s begin with the actual case. The graph below presents the CAGRs for different scenarios in case 1 (actual Sensex level). The first bar represents the scenario where an investor had started his SIPs way back in January 1990 (investment period of 30 years & 10 months). I am not sure if this was actually possible, but we are assuming that there was a way to invest regularly. The last bar represents the shortest investment period of 10 months, where the largecap SIPs started in January 2020.

The CAGRs vary a lot depending on the investment duration. The returns look impressive, especially for the SIPs that are more than 18 years old. But after that, you notice the gradual dip in CAGRs after the January 2003 time period.

The spike of 25% seen in the last bar is because of the great crash in March-April of 2020 and a very quick recovery seen soon afterward. This is quite unprecedented and will have to see if it is just a short term spike or it is there to stay.

So, if you ignore the last bar, you can see that the longer-term investor (18 years +) has gained much higher CAGRs that shorter duration investors. We cannot exactly predict what this would look like 15-20 years from now, but this should give you a good perspective if you plan for very long term investments.

But what if the current level of Sensex were different? We can simulate a few cases for that. Instead of randomly assigning any value to Sensex, we will take some cues from the past to come up with these values. The following are the charts for the five hypothetical cases explained in the previous section. We will note down our observations once we have seen all the charts.

Now, there are a lot of colorful charts here. Each one of them narrates a different story. I urge you to have a look at them carefully and draw your own interpretations before I put down a few of my observations in the section below.

Key observations:

The following are some of my observations. Hope you also came up with some solid observations of your own.

- There is high volatility in the short term SIPs. Especially in the SIPs that started after January 2011-2012. You can observe this in the last few bars.

- Current market levels have the least impact in terms of CAGRs, on Longer-term largecap SIPs. Although there are dips seen in the cases where Sensex levels are lower than the actual value, these dips are not too large compared to the fall observed for the short duration SIPs.

- The obvious point to note is that all CAGRs depend on the current market level, but the intensity of it is more pronounced on short-duration SIPs. This point is kind of summarizing the previous two points.

- SIPs of 18 years and more (started in January 2003 or before) have given respectable CAGR returns. Even during the cases of worse market levels, the minimum observed CAGR was a decent 8%.

- Please appreciate that one big downswing can have a very adverse impact on your SIPs. Even long durations SIPs are prone to it. The 7-year SIP (second case of previous low) which gave negative returns is one such example. There is no easy or sure shot way to avoid or predict it. But keeping yourself informed will help you manage your expectations and plan your investments better.

Conclusion:

SIPs can give different returns based on your investment duration and current market levels. They can give you lower or even negative returns despite being invested for longer periods. This can happen if there has been a big crash, or most of your SIP investments were during a bull run in the market or at higher valuations. Longer durations act as a shield to fluctuations to some extent.

We will cover the same analysis for midcaps and smallcaps in the next few articles.

Think long term when you think of SIPs !!!

Data sourced from: https://www.bseindia.com/Indices/IndexArchiveData.html