Updated on: May 15, 2021 ; Investments

Introduction:

In our discussions on PE ratios so far, we have talked about its meaning and its possible usage as an investment indicator. In this article, we will apply the concept of PE as an indicator for strategizing investment plans. We will see how a simple PE-based investment channeling strategy plays out in reality.

We will answer the question – Is PE-based channeling investment strategy really worth it? In the next few articles, we will also look at different variations of this strategy. This will help decide if any PE-based investment strategy can improve the value of your investments.

What is PE-based investment channeling?

In a simple PE-based investment channeling strategy, the investor decides to channel or invest his/her capital into financial assets based on the PE level of one or more financial assets. This is not an industry-defined phrase. I have used this phrase to summarize the strategy in as simple terms as possible. I will explain this in a bit more detail.

Firstly, to keep matters simple, we provide the investor with a choice of two fundamental financial assets only. Many of you might have already guessed what these could be. One is an equity asset, and the other is a debt instrument.

For equity, we have considered the Nifty 50 index. And for debt, we have assumed a risk-free debt instrument that gives an 8% return annually.

In the real world, there are many more choices available to an investor. But, we are going ahead with these two basic assets to avoid any unnecessary complexities.

As far as data is considered, we have used monthly data for Nifty 50 starting from January 2001 till January 2021. The Nifty 50 level and its corresponding PE ratios are recorded at the start of each month.

The assumption is that the investor has 1000 rupees at the beginning of each month to invest. He/She can either choose to channel the investment in the equity bucket or the debt bucket. The default choice is to invest it in the equity bucket. This default choice will be our base case.

In this article, we will see what happens to the investments if the investor slightly alters the investment strategy. He/She does this by diverting the funds into equity and debt bucket based on the Nifty 50 PE levels.

So, the strategy is to channel the investment into the equity bucket if the monthly PE of Nifty 50 for that month is below a certain level. And in case the Nifty 50 PE crosses above that level, then channel the funds into the debt bucket.

There are no withdrawals in this strategy. That means, once the investment is made into a bucket, it is not taken out till the end of the analysis period.

Based on the previous article – Can PE act as an indicator, we have chosen two PE levels as the threshold levels. They are 22 and 18. The investor will channel the investments based on these threshold values. We will compare the investment value throughout the analysis period with the base case. In the base case, the investor continues with the simple monthly SIP of 1000 rupees in the Nifty 50 index.

We will also take a look at a small variation of the above strategy. In this, the channeling decision is based on the 12-month moving average PE of Nifty 50. This is to ensure that channel switching happens only when the PE threshold has been breached for a long time.

Now, it is time to look at the graphs, and see what they reveal.

Strategy in action:

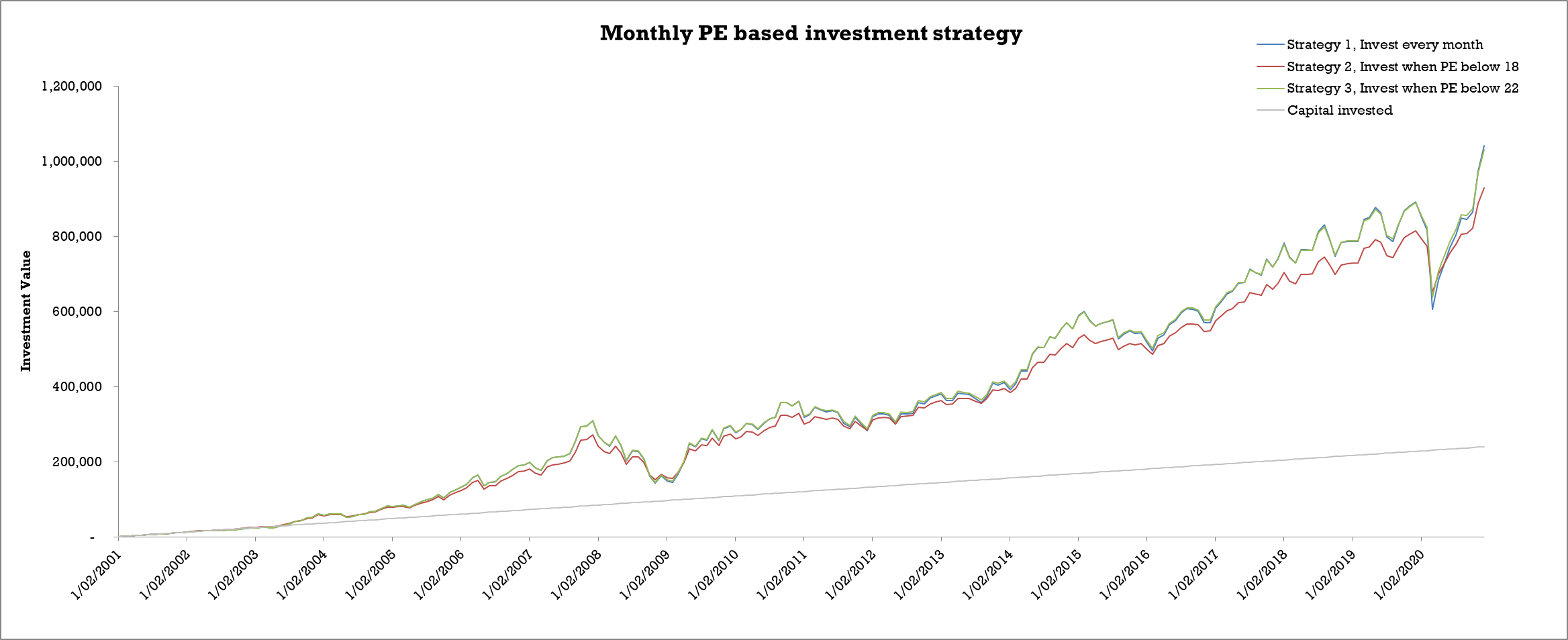

The graph below shows the performance of monthly PE based investment channeling strategy.

The first thing that stands out from the graph is the consistent underperformance of Strategy 2 (threshold PE = 18). So, this strategy for PE @18 is not a suitable option.

Now, here is the other interesting finding. The performance of Strategy 3 (threshold PE = 22) closely follows the performance of Strategy 1 (Monthly SIP). So, whether you deploy the channeling strategy with threshold PE as 22, or continue with a simple SIP, there is no significant difference in your returns. So, why bother with the added complexity of channeling your investments when there are no substantial advantages.

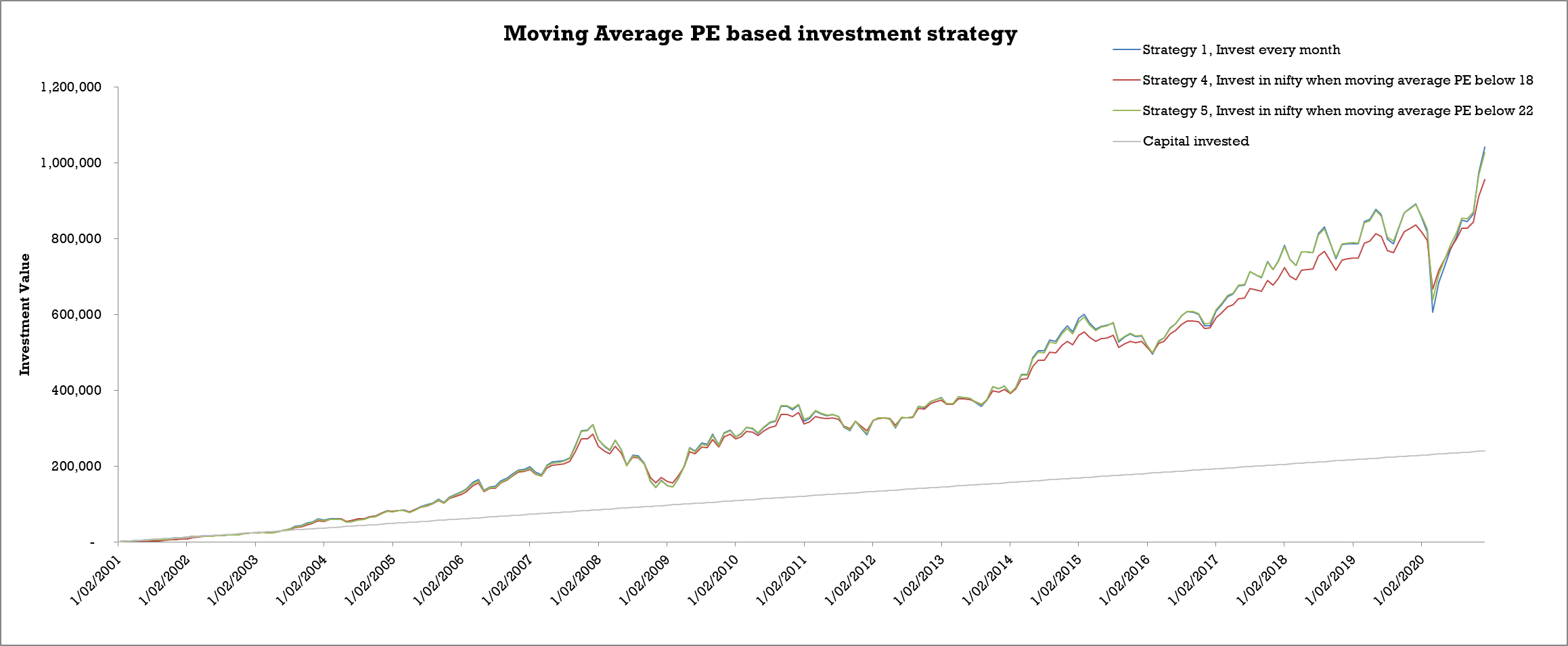

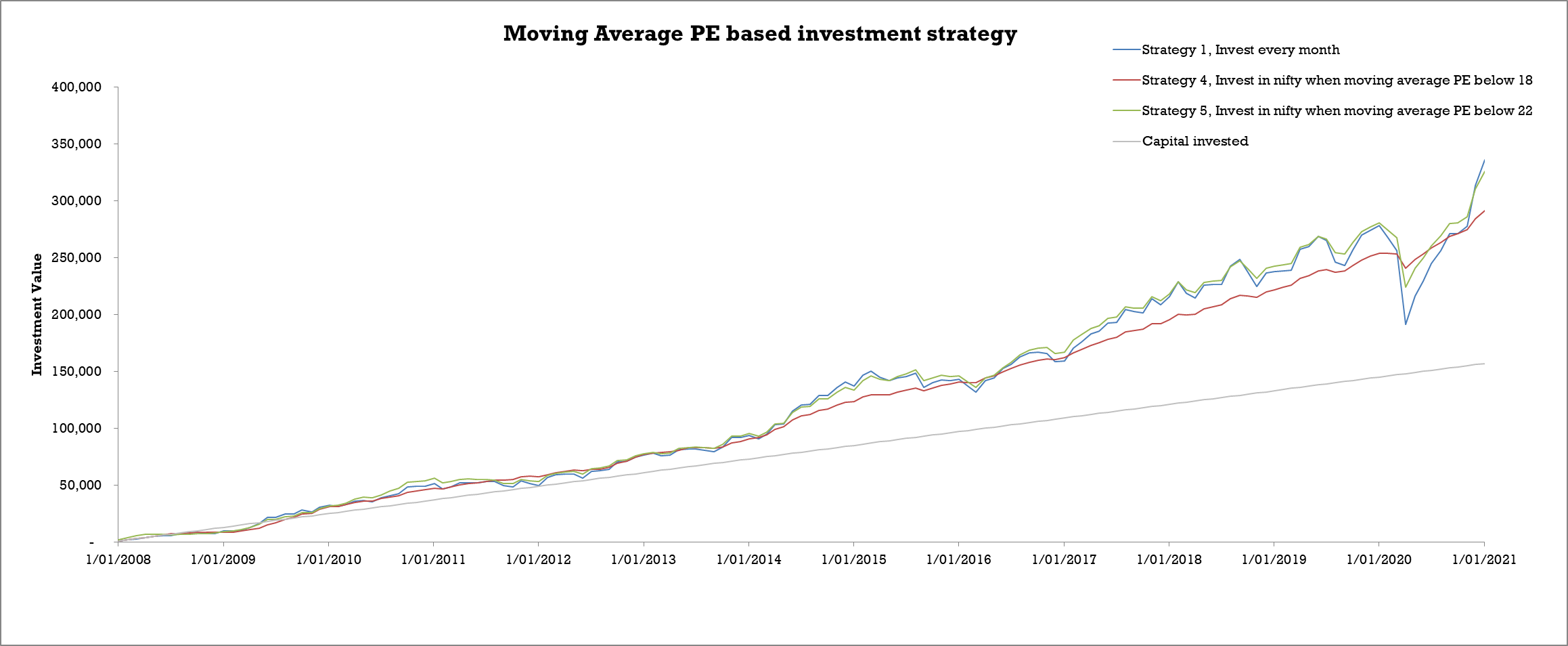

Now, let’s see what happens when the strategy is based on moving average PE.

The trends don’t change much from the previous case. The gap between Strategy 4 (threshold PE = 18) and the other two strategies are reduced. So, in this case, the strategy based on monthly PE and moving average PE results in very similar results. Before we move on, let’s put some numbers to see what the final investment values would look like.

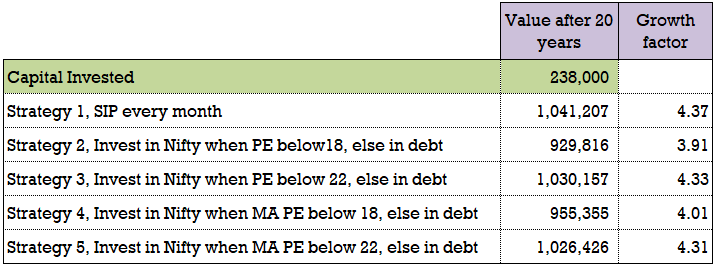

The total capital invested over a period of 20 years comes out to be 238,000 rupees. All the strategies have resulted in handsome returns of ~4 times. Strategy 1, which is the normal monthly SIP in Nifty 50, turns out to be the clear winner here. This leaves the PE-based investment channeling strategies at the PE thresholds of 22 and 18 inferior to the simple SIP.

But, before you draw any conclusions based on the above numbers, you need to look at another set of numbers. If you have gone through the previous posts on SIPs in mutual funds, you would know that the value of your investments depends on the time frame of the investments.

To complete our analysis, we will look at the scenario when the investment’s start time coincides with a market peak. For this, we have chosen a time before the financial crisis of 2008. This would have been one of the worst possible starts for any investor to get into the markets. So choosing this time-frame would help us understand the performance of your investments under unfavorable conditions.

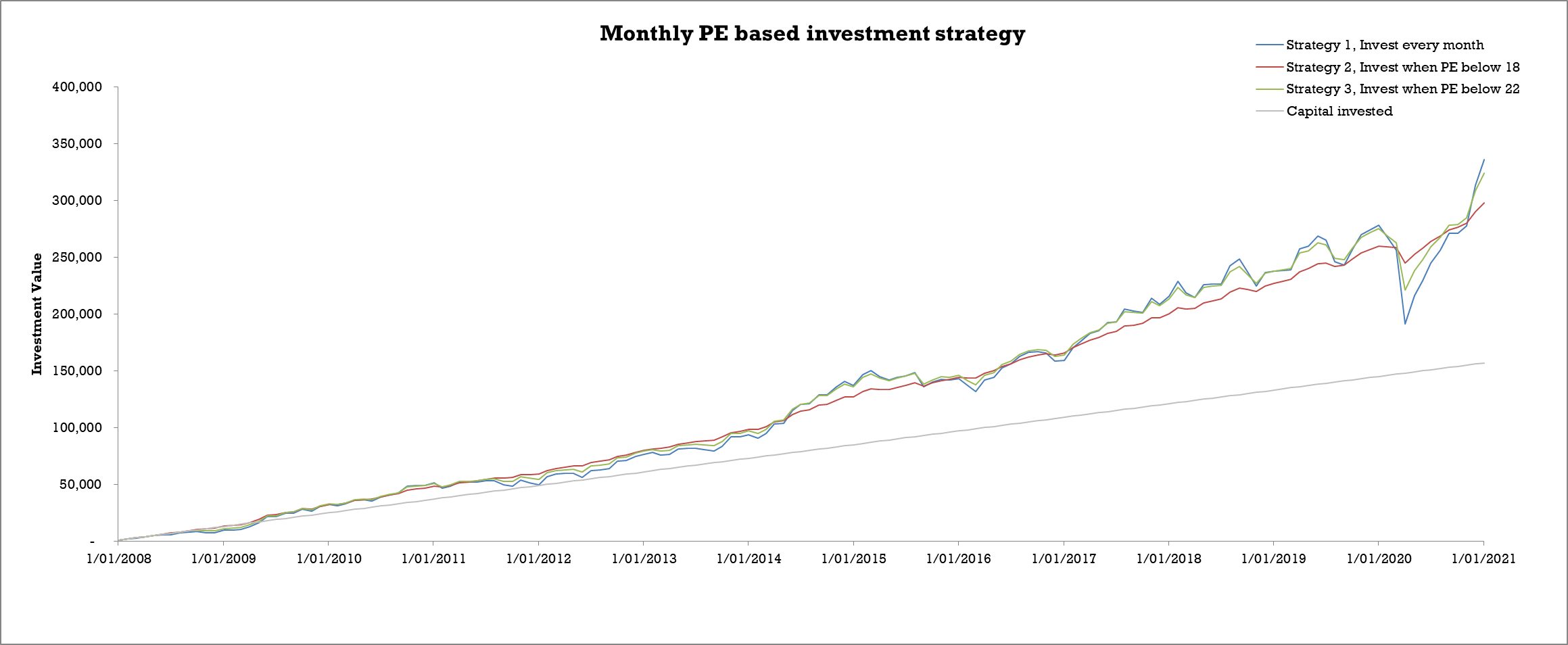

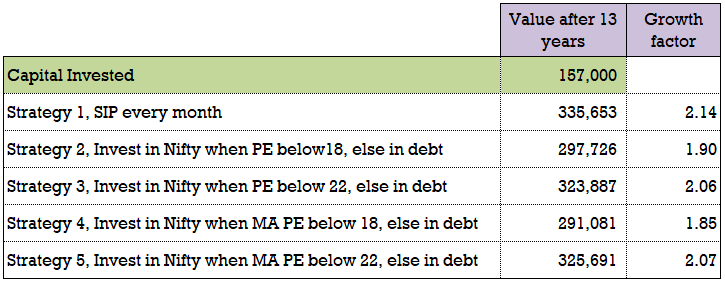

So, we repeat the same analysis, with the only change being the start time. The investment time frame reduces from 21 years to 13 years in this case. Let’s study the graphs now.

The story here is slightly different from the previous one. Did you notice the difference?

The first thing to notice is that Strategy 2 (threshold PE of 18) does not look that bad. In fact, this strategy provides some stability to your investments. During the bad market phases, this strategy saw a milder decline compared to the strategies. Strategy 2 seems to provide decent returns along with some downside protection. This makes it look like an attractive investment strategy in this scenario.

The other point to notice is the relation between Strategy 1 and Strategy 3. When compared to the previous scenario, there seems to be a slight divergence between the two. In fact, Strategy 3 (threshold PE = 22) also provides some cushion during market crashes. Otherwise, the returns were similar to that of Strategy 1 for most of the time period.

Let’s see what would the strategy based on moving average PE look like.

The results here are very similar or what we observed above.

Let’s look at the investment values for the these strategies at the end of the 13 year investment period.

Almost all the strategies have given a growth factor of ~2 times. Strategy 1 has provided the highest growth as of January 2021. But along the 13-year investment period, you can see that there were times when other strategies overtook it. So you can decide which strategy works better for you based on your investment time horizon and risk appetite.

Key takeaways:

Following are the some key points based on the analysis done above:

- There are no noted advantages of monthly PE-based investment channeling strategy in terms of superior returns. This is irrespective of the start period of the investments.

- If the investment starts when markets are at a high, then the PE-based investment channeling strategy helps in reducing the downside risk to some extent.

- When comparing between the PE threshold levels of 18 and 22, PE =22 seems to be a better option.

- To sum it up, based on these data points, it is not worth the pain of deploying this PE-based strategy. The simple SIP in Nifty 50 will save you the mental stress of monitoring and switching your investments monthly.

So, we will look at some other PE based strategies in following articles and see if they are worth their salt.

Till then, Stay tuned !!!