Updated on: May 15, 2021 ; Investments

Why take a loan?

There are many different types of loans and providers in the market. The process of availing of a loan has also become much simpler and convenient. To help further, many sites provide in-depth comparative studies between different loan options.

Before we proceed further, let’s understand the basic reasons behind taking a loan. The first obvious reason is if you desire something, but don’t have the money to buy it. In such cases, you can look for someone to lend you the money or take a loan from a bank or a financial institution. For this, you would have to pay interest on the loan amount taken.

The second reason would be if you have the money, but want to use it for some other purpose. And if that other purpose is to invest somewhere, then you are in the right place. As you have the option of going for the loan or not, you need to weigh the options before making the decision.

Options:

That is what we are going to explore in this article. Let’s assume that you need 10 lakhs to buy a car and you have the amount in your bank account. In that case, you have 2 options in front of you.

- Option 1: Take the loan to buy the car and pay monthly EMIs. And invest the 10 lakhs in your bank account in any asset class of your preference. Now it is up to you to decide, whether you want to do staggered investments or a lumpsum investment. To keep matters simple, we will analyze the case of lumpsum investment in this article. I encourage you to explore different staggered or SIP investment scenarios on your own.

- Option 2: Don’t take the loan. Fund the car with your bank balance. Then, invest the equivalent EMI amount (if you had taken the loan) in the asset class of your preference every month.

Use cases:

For our analyses, we will be looking at two asset classes as the choice of investments. The first one being BSE Sensex that represents the broad large-cap equity market, and the other being gold which is a traditional investment asset for many.

We will be looking at the last 17 years of monthly data for BSE Sensex and Gold prices. We assume that the principal loan amount is 10 lakhs and the tenure is 10 years. Then, we will compare the returns of two options for different interest rates (8%, 10%, 12%, and 15%). In this analysis, we will be looking at all the possible monthly scenarios when a loan could have been taken.

The data for Sensex and gold prices starts from April 2003. So, the first data point for comparison is in April 2010. This is the time when the earliest possible loan is taken in April 2003 matures. Since this is a monthly analysis the next data point would be in May 2010. This is when the second possible loan is taken in May 2003 matures.

Analysis period ends in December 2020.

We have assumed that the EMI payments happen at the beginning of each month.

Comparison with equity investments:

As mentioned above, in this section we will be comparing the ‘loan or not’ options with Sensex as the choice of investment. We will compare the value of the investments at the end of the 7 year loan period for both the options. Just a reminder, option 1 is a one-time lumpsum investment in Sensex, and option 2 is SIP of EMI equivalent for 7 years.

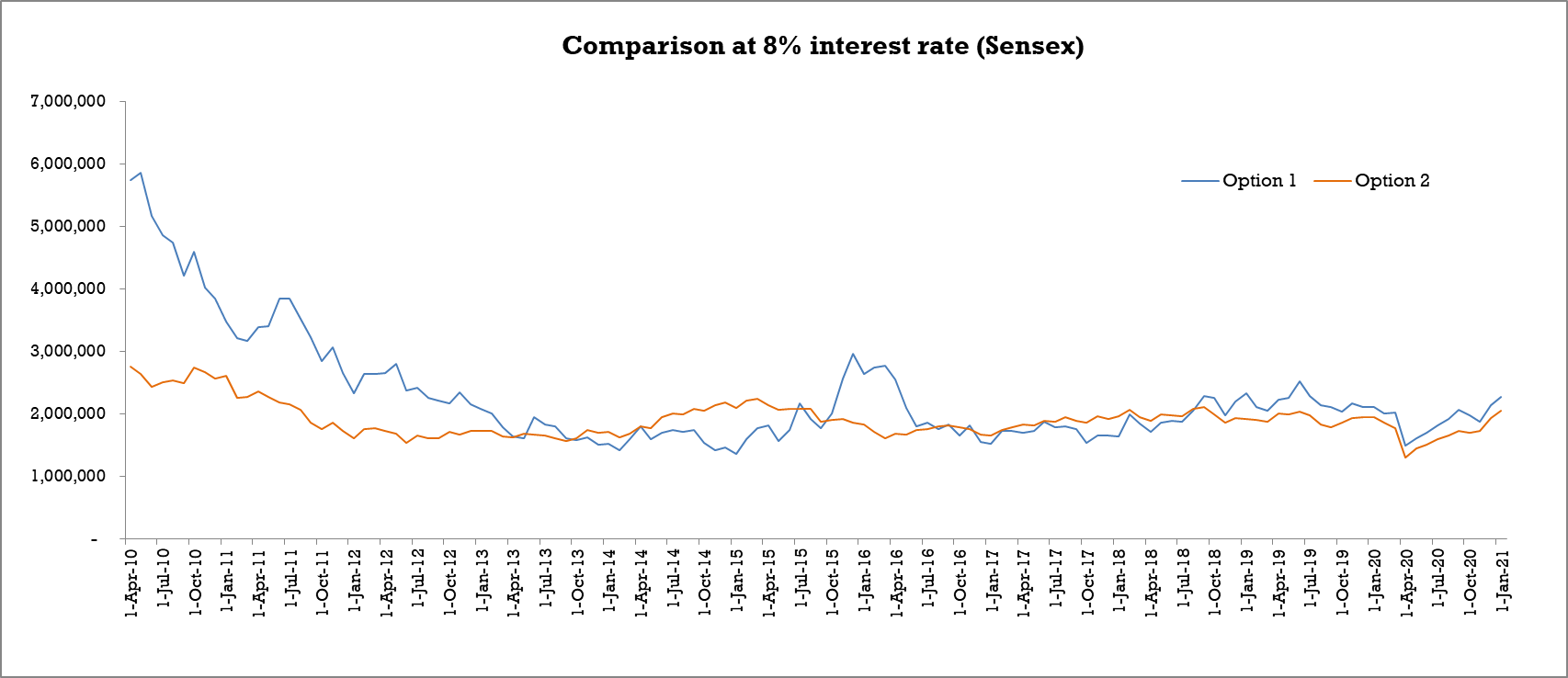

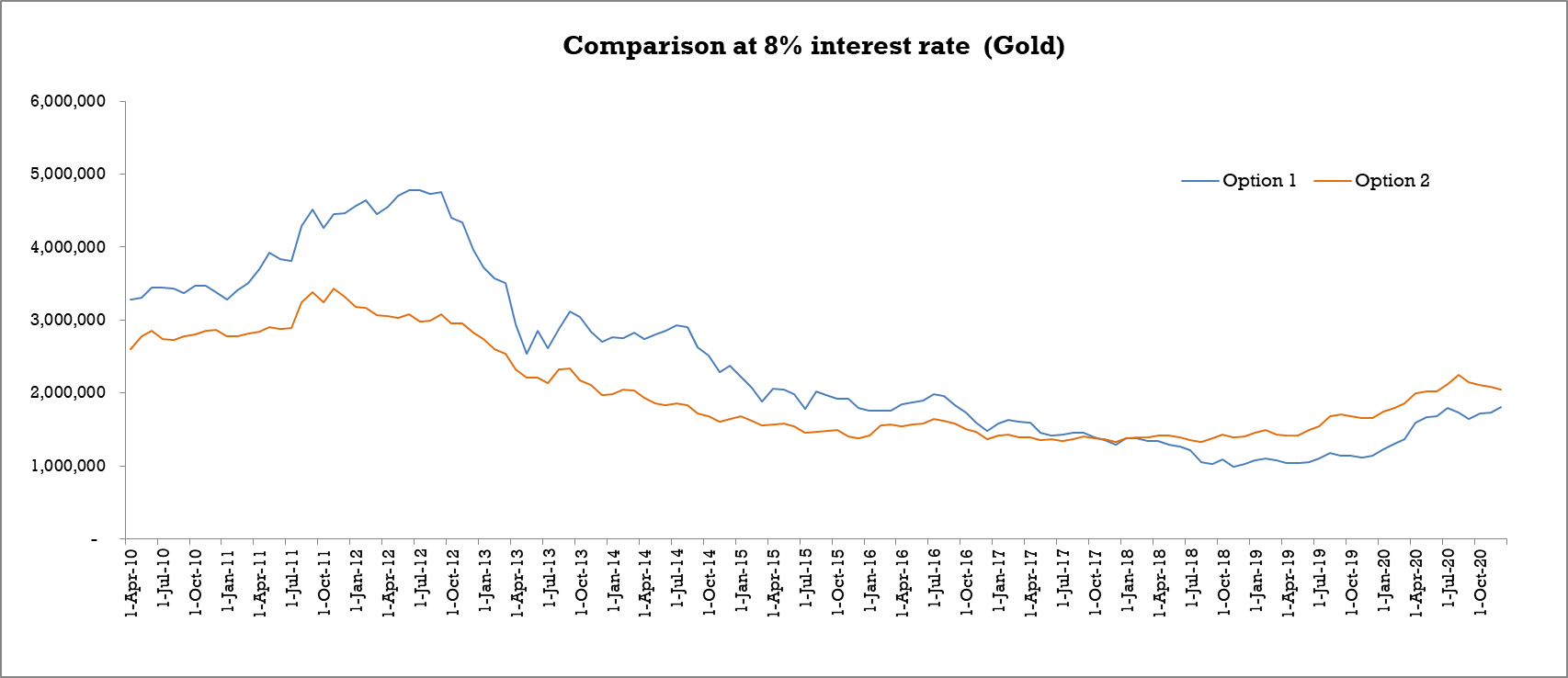

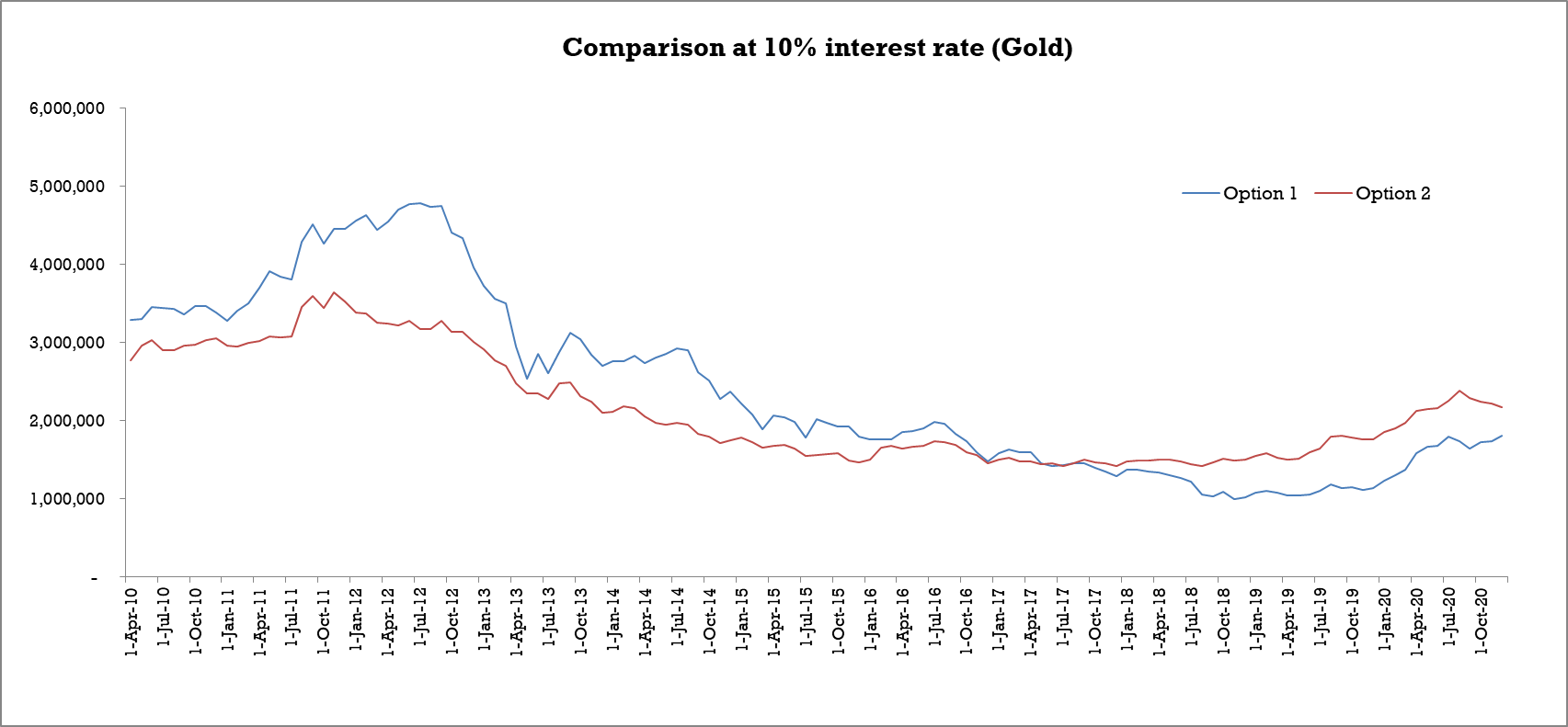

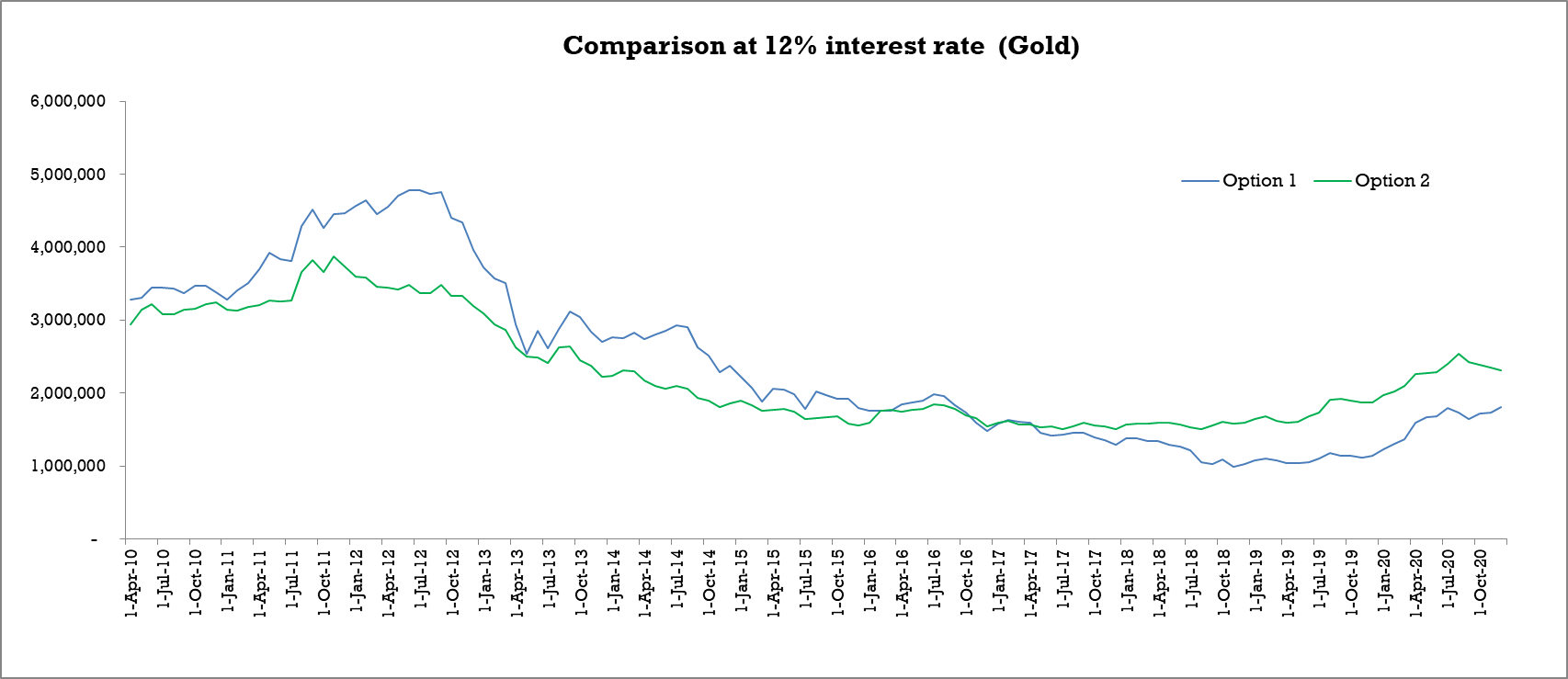

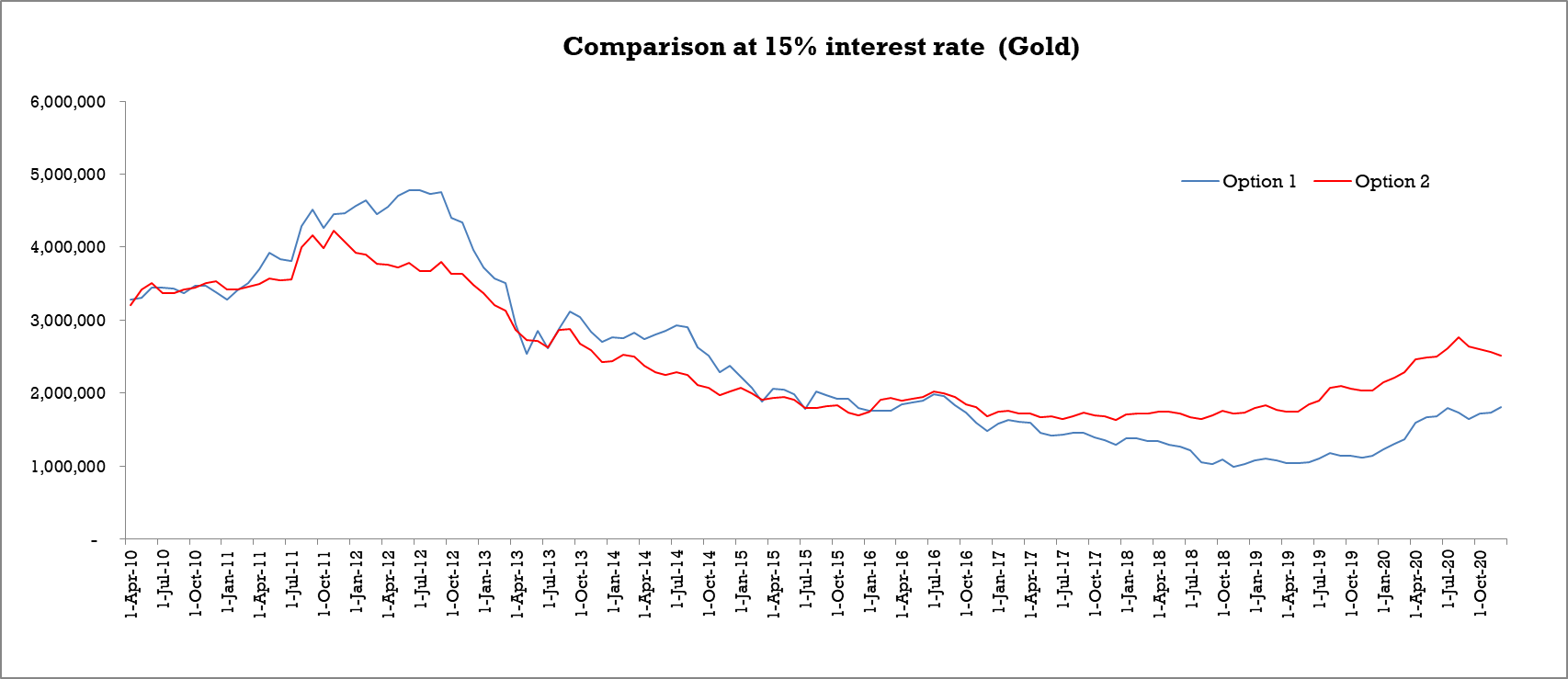

You will see the monthly comparison between the two options in the charts below. Each chart represents a different rate of interest for the loan. We will start with an 8% interest rate and gradually move to a 15% interest rate.

The blue line represents the value of 10,00,000 invested in Sensex after seven years, assuming there was some fund closely following Sensex. The second line represents the second option. In here, you would have invested the amount equivalent to your EMI had you taken the loan every month. So option 1 is lumpsum investment and option 2 is SIP investment. The only aspect that changes is the monthly investment amount in option 2. As the interest rate increases, the EMI amount also increases, and therefore the SIP investments.

For the first 3 years (till April 2013) Option 1 seems to be the clear winner, that too by a big margin. The period between mid of 2013 and mid of 2018 sees a few swings. Then in the last couple of years, Option 1 seems to be the winner again, but only with a slight edge.

It is clear from the graph above that, there is no consistent winner. It all depends on the value of the asset class (Sensex in this case) when you start your investments. But if I have to choose a winner, then I will go with option 1 in the 8% interest rate regime and try my luck.

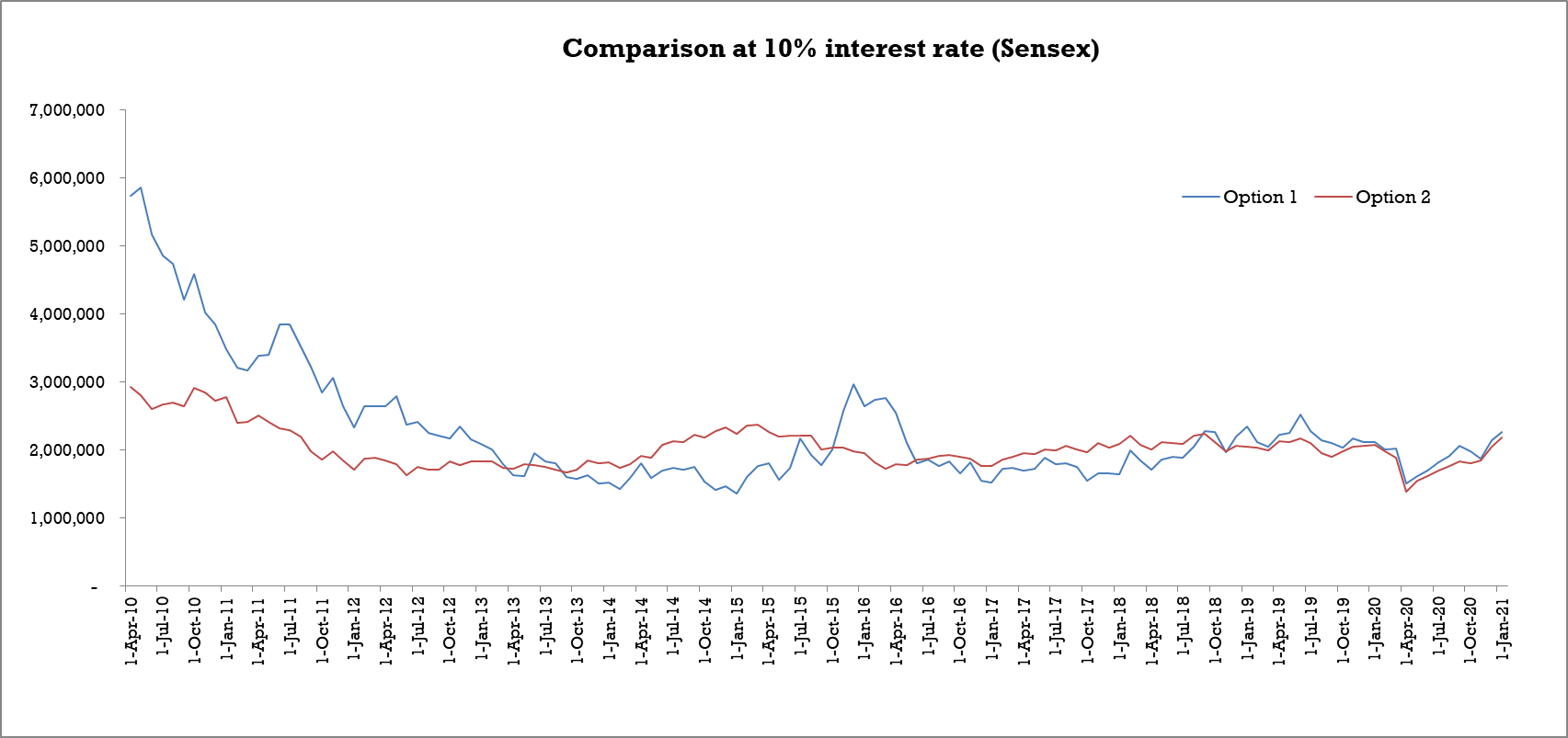

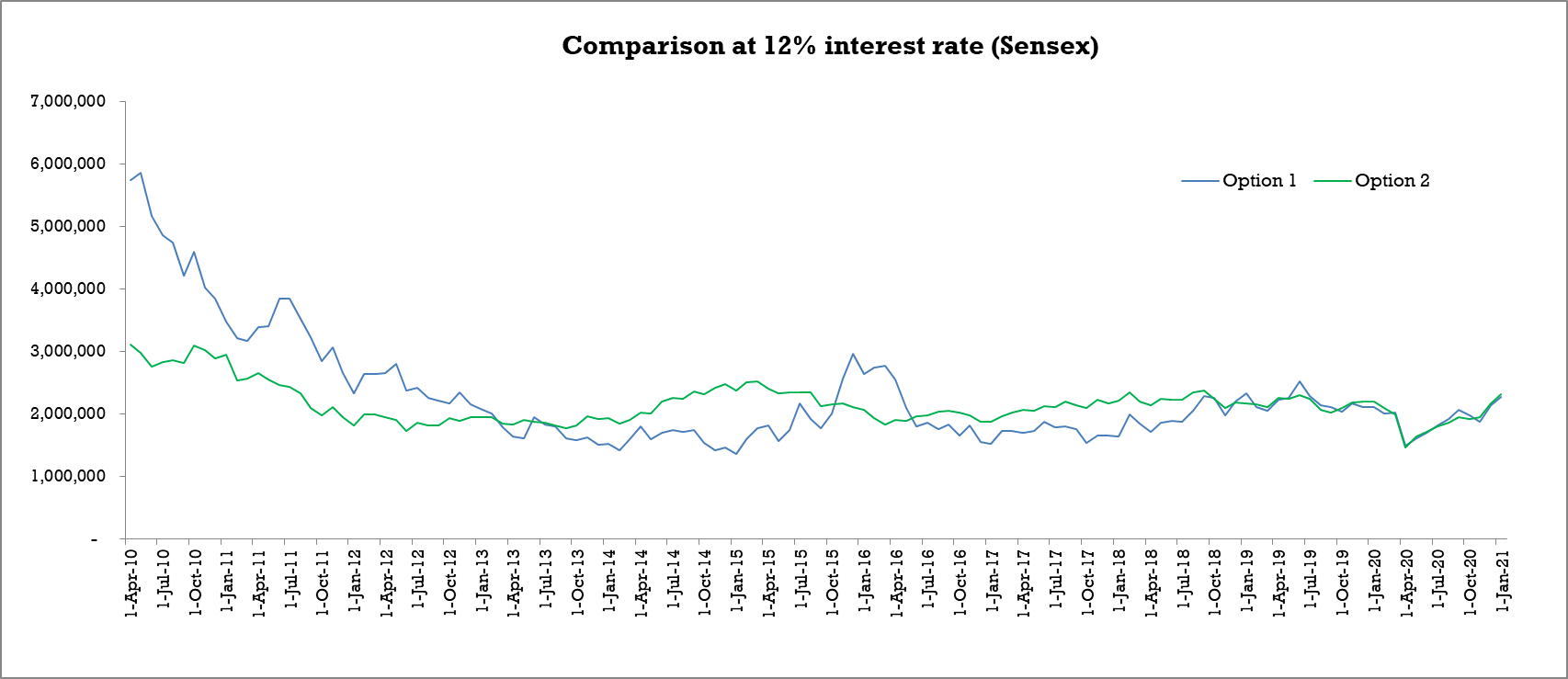

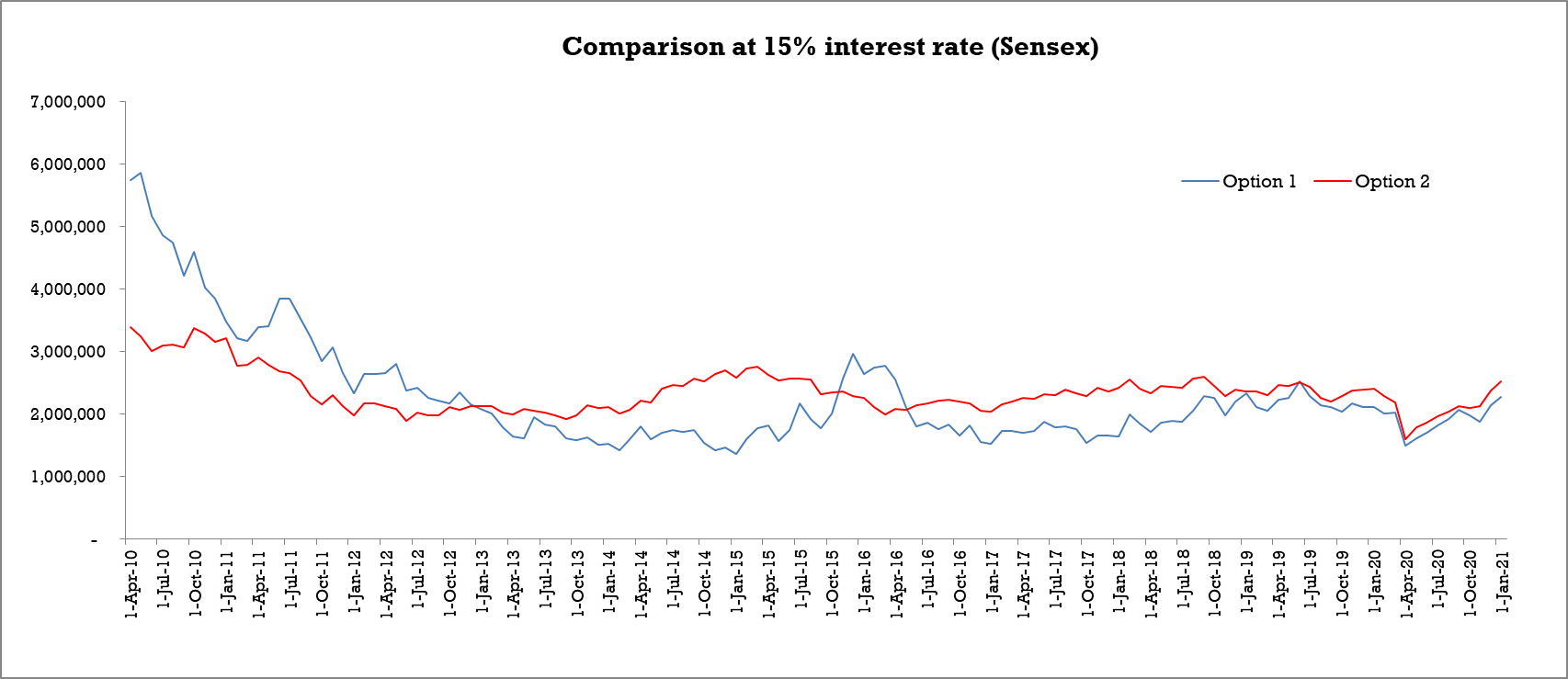

What do you think would be the story for higher interest rates? You should have guessed it by now. Let’s see that in the graphs below:

As the interest rate increases the slight edge that option 1 had over option 2 starts to fade away. In fact, if you ignore the first three years, option 2 turns out to be the better choice. This is a more prudent choice as well. Don’t take a loan until you cannot do without it or, the alternate option has a very good value proposition.

So this was a glimpse of how the ‘loan or not’ question fared against broad equity investment. You can also analyse this against other indices or you choice of stocks. Before we conclude, let’s look at the other asset class – Gold.

Comparison with gold investments:

Since you are already warmed up with the case of equity investments. We will proceed to the graphs for gold investments quickly. One thing to keep in mind is that, for gold investment prices, we have taken the average gold price of the month. There is no particular reason behind choosing it. It was just a matter of convenience as we had that data readily available from the previous analyses.

Below are the 4 comparison graphs with gold as the investment asset.

What we see here are some interesting trends. For all the 4 interest scenarios Option 1 seems to be the better option for the initial 5 to 8 years. As the interest rate increases, this time period decreases.

Once the trend reverses, option 2 becomes the better option and remains so. These relatively clearer trends are due to the less erratic price movement of gold prices compared to equity.

As seen in the case of equity, the positions have switched in the time frame of observation. It depends a great deal on the interest rate of the loan and the value of the asset class.

No investment decision is straight forward. So is this case. While deciding on not taking a loan you also have to consider if you would have enough cash for emergencies.

Conclusion:

There are no clear and consistent winners here. But it seems logical to avoid taking loans when the interest rates are too high. Also, as good practice debt should be avoided as far a possible. Finally, it is your choice, whether you want to go for the loan or not. You can also go for partial financing based on your cash position.

Make prudent and comforting choice!