Updated on: December 9, 2020 ; Investments

Introduction to gold investment:

Gold needs no introduction, neither does gold investment. We all know that traditionally, gold holds a very special place in most of our lives. It has been considered as the main trove of treasure by many for ages. The history of gold can be traced back to thousands of years, and for us, it also holds a very sentimental value.

But in this article, we will be looking at gold purely from an investment perspective. It could be a vital component of your asset diversification strategy. We will conduct two studies in this article based on the historical prices of gold. But before jumping on to the analysis, let me provide a little background on the data.

Background:

We have considered gold prices from 1979 till 2020. This makes it 42 years of gold investment analysis. This is a decent time period to understand the performance of any asset class historically. To simplify the matters, we have assumed that the investor buys gold at the annual average price of the investment year. This is to avoid unnecessary complication of different buying possibilities of monthly and daily.

With this backgorund, we can now move on to our studies.

Gold investment – Study 1

In this study, we analyze different scenarios of one-time investments and study the results in 2020. Each scenario depicts the case of a one-time investment in different years. So, in the first scenario, the investment was made in 1979, and in the last scenario, the investment was made in 2019. We assume that in each scenario, the investor bought 10 gms of gold at a 999 (24-carat gold) purity level. Other assumptions are that there were no transaction charges, and gold was bought at the annual average price of that year.

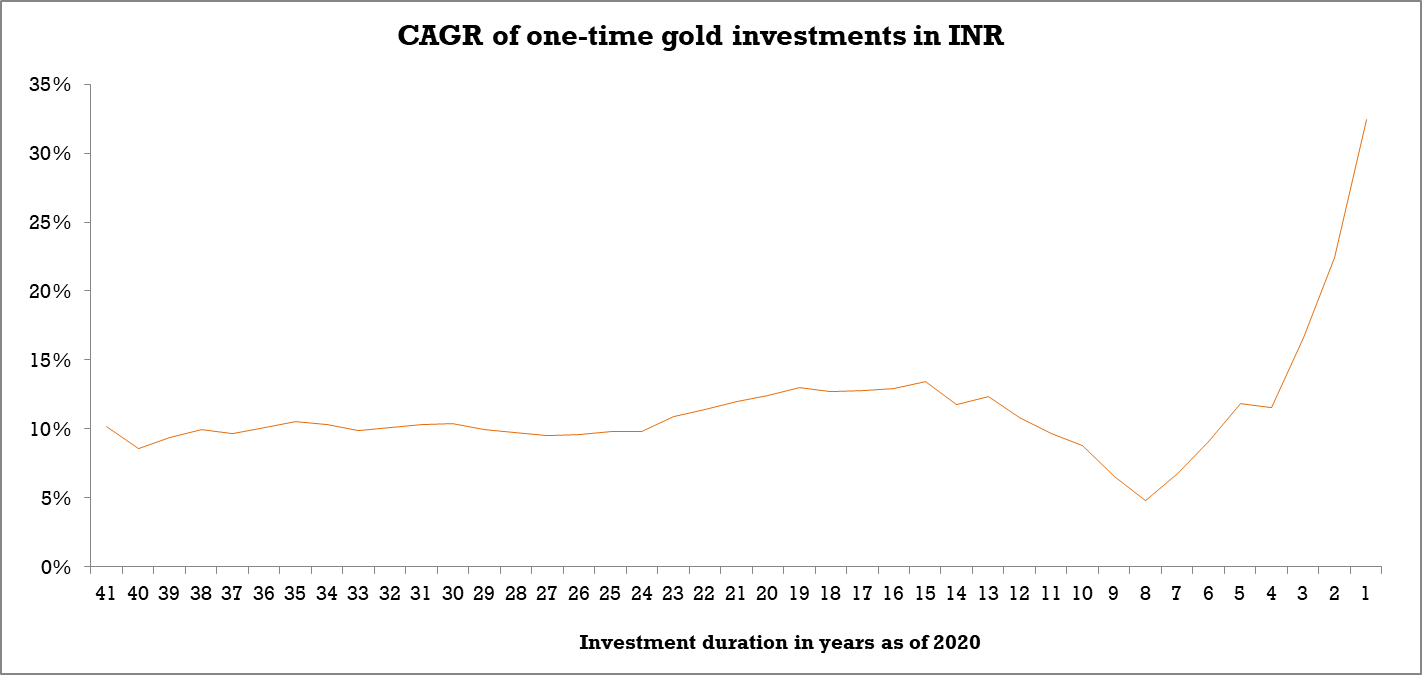

Now it’s time to look at the CAGRs for the 41 different scenarios in 2020. Just a reminder, the first scenario has 41 years of investment duration, and the last scenario has just 1 year of investment duration.

What we observer here is that investments older than 10 years have given a CAGR of 9%+, (almost in all the cases, barring one or two cases). For the investment duration of 8 years, it fell to a low of a mere 4.8%. Then at the end, it shoots up to a phenomenal high of 32.5%. More or less, the returns seem to be decent with a minor dip between 7-9 years of investment duration. Please note that this is because gold was sailing at its all-time high in the year 2020 (the assessment year).

In the case of gold being at a lower level, the story would have been very different for the shorter durations (especially less than 12 years). The CAGRs for investment durations above 12 years, would still be above 8% under most circumstances.

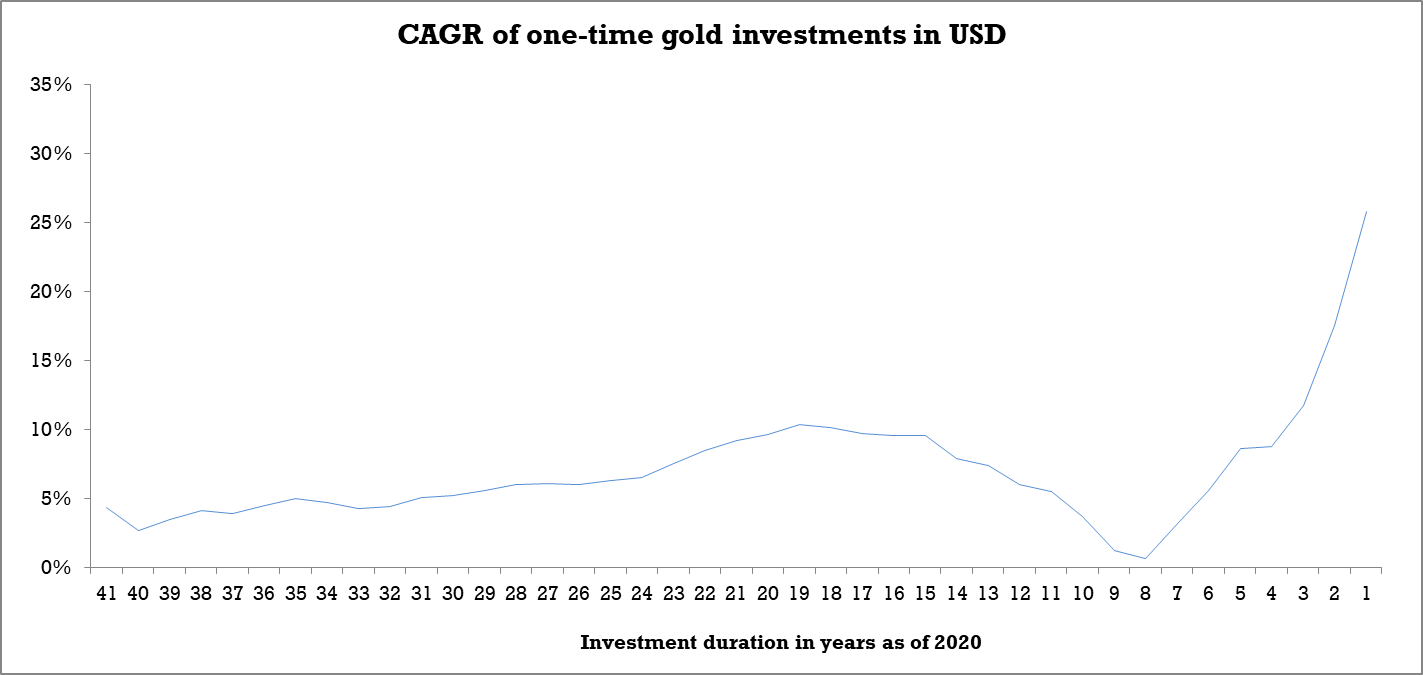

Did you notice the INR (Indian rupees) in the chart title? Wonder why I put it there? All of our investments have been in the Indian market with INR. But gold is a global asset, which gets traded globally in all the major currencies. So it is worthwhile to get a perspective from a global investor’s point of view. For that, we will analyze the same CAGRs, but for an investor who had invested in gold using USD (US dollars – $). USD is a standard proxy for an international or global investor.

The first impression you might get is that USD gold investments follow the same trend as INR gold investments. But you will soon notice that the USD chart is lower than the INR chart. For investment durations of 26 years and more CAGRs were below 6%. For most of the investment durations, there is a big gap of 3-6% in CAGRs between INR and USD investments. Not only that, the USD CAGR touched a low of 0.6% for the 8 years investment duration. It seems that an Indian investor would have fared much better than an ‘international’ investor.

But why is there such a big difference between the two investment currencies?

Many of you would have already guessed it by now. It is because of the exchange rate between INR and USD. The Indian rupee has depreciated significantly against US dollars in the past, and the slide continued in 2020 as well.

So what may seem to be a very good investment asset for an Indian investor, might not be as lucrative for a foreign investor. Of course, it all depends on what are all the other opportunities available, and what has been their performance in the past.

This study was based on the actual price of gold in 2020. This makes this study a bit narrow and very specific. Now let’s look at a holistic picture by analyzing the rolling window CAGRs in the next section.

Gold investment – Study 2

In this study, we will be analyzing 5 rolling windows of gold investments. These rolling windows are for – 2 years, 5 years, 7 years, 10 years, and 15 years.

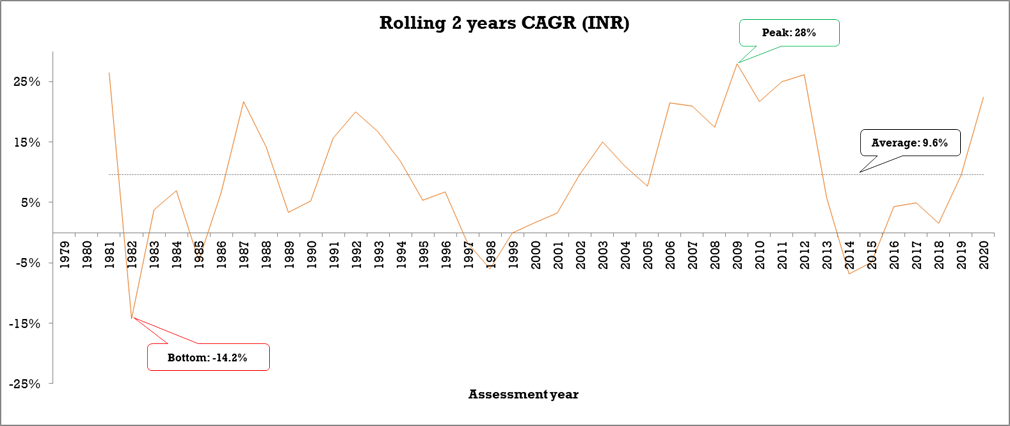

Let me explain what a rolling window is before we start looking at the charts. I will take the example of the 2-years rolling window to explain the concept. In this example, we assume that the investor buys 10 gms of gold in the first year (1979) at the average annual price of gold that year. Then the performance is measured in terms of CAGR after two years (1981). We repeat the same process for every year, till the measurement/assessment year reaches 2020.

So, this analysis provides a broader view of the gold investment scenarios spanned across different years and different investment ndurations. Now, we are all set to look at the charts to understand the performance.

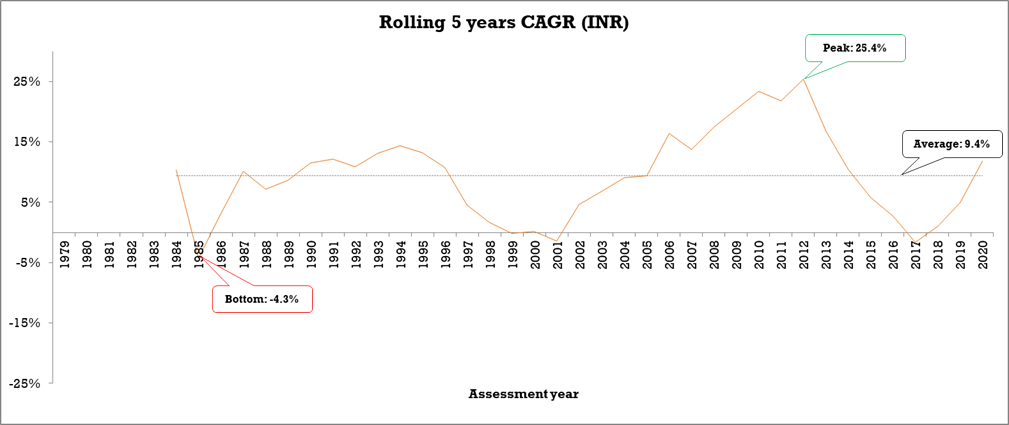

Have a close look at the CAGR charts above. What you will notice is that the average CAGRs for all the scenarios are almost the same. They are in the range of 9.4% to 10%, which is a good number. But does this mean that you will get close to 10% anytime you invest in gold? No.

Look at the trends and the volatility associated with it. You will notice that the volatility, which is represented by the high movements in CAGRs, is higher for the shorter durations. You can see higher peaks and lower bottoms for shorter rolling windows.

What this means that there is higher uncertainty in the CAGRs when you are invested for shorter durations, no matter what the average returns might be telling you.

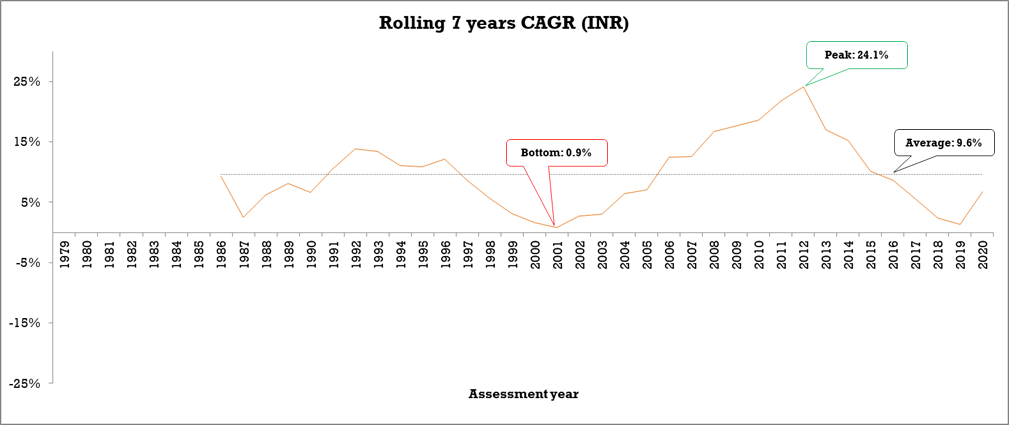

Now, I want you to focus on the bottoms because that is what depicts the potential downside of your returns. If you look at the 7-years scenario, you will see that in 2001 the CAGR was very close to zero. What it means that your 7 years old investment had not moved much. You could have been better off, parking that money in your savings bank account.

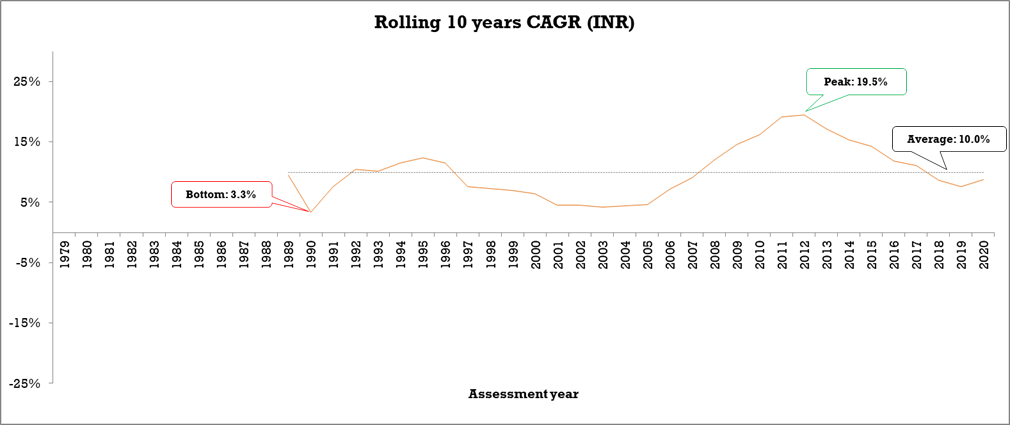

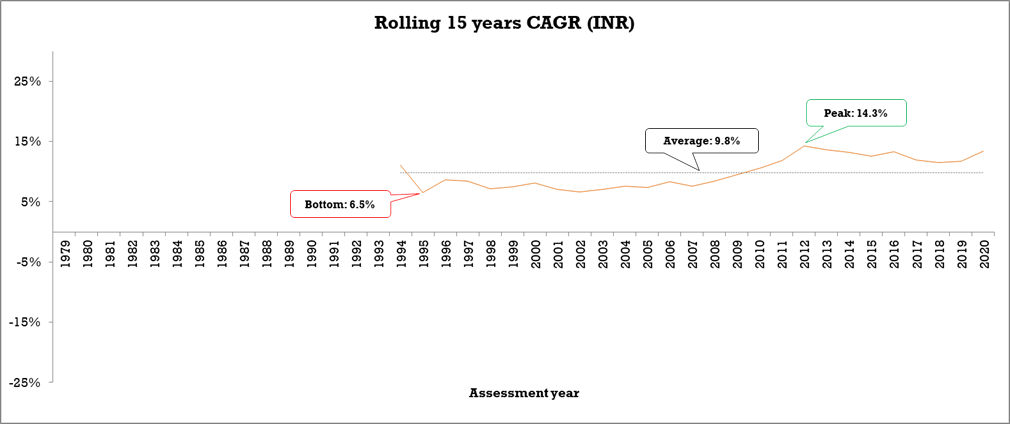

Even in the 10-years scenario investor experienced a very low CAGR of 3.3% in 1990. Only in the 15-years scenario, we saw a somewhat acceptable, if not desirable CAGR of 6.5% in 1995.

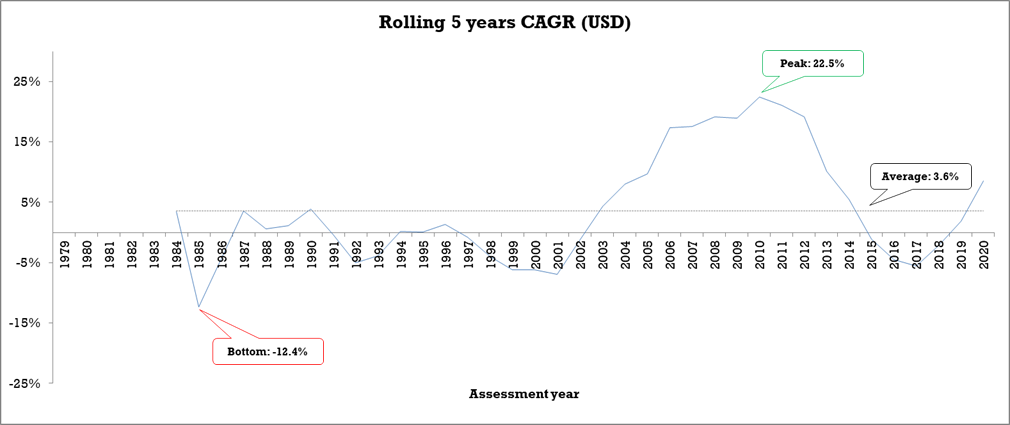

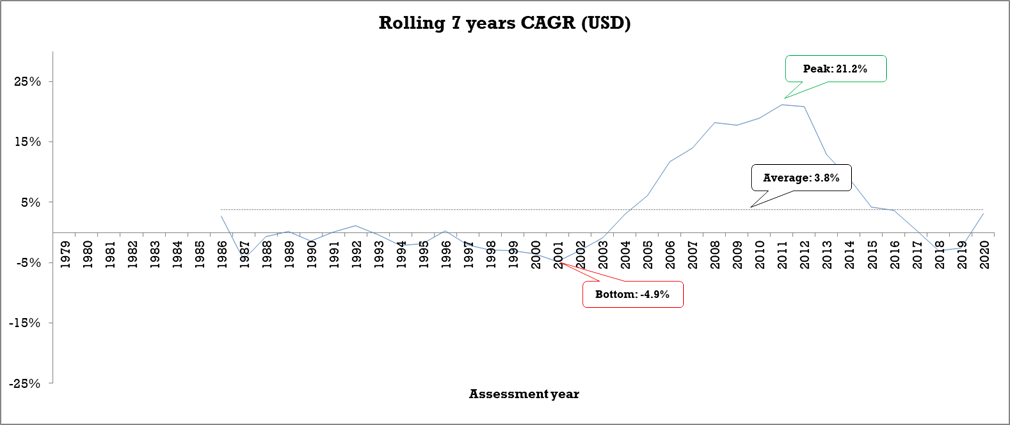

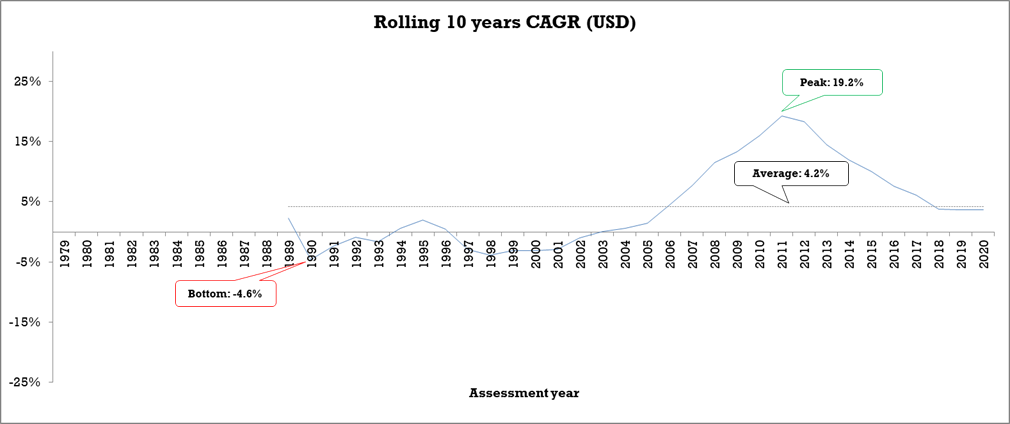

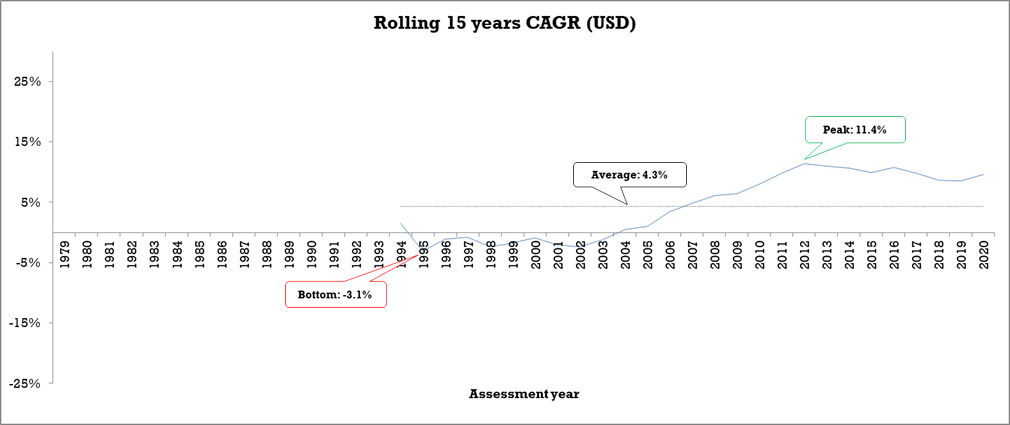

Let’s have a quick look at the CAGRS for gold investments in USD as well.

Compare what you see as a USD investor with an INR investor. The trends look similar, but the returns in USD are much lower than INR. You can see the same in study 1 as well. What is worth noticing is that in all 5 scenarios the bottom was negative. This means long-term investors saw their investments erode after waiting for very long periods. For instance, look at the 15-years scenario. CAGRs were negative for 9 long years, from 1995 till 2003.

Conclusion:

Gold may be considered a haven for many. But gold too has had its episodes of downward slides. Gold too can lose its shine at times. Hope you now have a better understanding of gold as an investment asset. Based on your investment currency, you might experience very different returns. I request you to read other articles on investments in other asset classes and make informed decisions while making your asset allocation.

Keep shining like gold !!!