Updated on: November 30, 2020 ; Investments

Introduction:

We have already covered numerous SIP investment scenarios on different market caps. There the focus was on the range of returns over different durations and investment start times. We compared the different possible returns, maximum upsides, and downsides that a long-term SIP investor could experience. Links to those articles are provided at the end of this article.

In this article, we are going to trace the journey of a long-term SIP investor as he/she wades through the years, month after month with his/her regular investments. By following this course we will get a flavor of the ups and downs the long-term investor experiences on this long and challenging journey.

Background:

As in our previous articles on SIPs, our long-term SIP investor here makes a regular monthly investment of 1000 rupees in the market consistently. We have taken BSE Sensex as the proxy for the market.

We have assumed that there was a way to invest in the Sensex equivalent market. Also note, we have not accounted for any dividends.

First, we have assumed that our long-term SIP investor has been religiously investing in the market from day 1, i.e. from January 1990. This is the earliest, from when we have the Sensex data available with us. Then we track his/her investments every month till November 2020. This makes it a very long investment horizon of almost 31 years.

This article will give you an insight into what a real investors go through and how do they see their portfolio’s returns at different levels of highs and lows of the market. This article will also help you understand how does it feel to be in a bull and a bear market. It will give you a better sense of, how long is long-term. It will help you access the risks a long-term investor faces. In short, it will help you make better and well-informed investment decisions.

Now, the scenario we discussed above is just one of the many possible scenarios. Indeed, it is a rather special scenario as it starts from the day Sensex data is available which goes way back to the early 1990s. But many of you would not have been born by then.

So, not risking to be one-sided in our analysis, we will introduce one more scenario. We will discuss the details later in this article.

Investing from the very beginning:

The long-term SIP investor who started his/her investment journey in January 1990, would have witnessed the roller coaster ride of bull and bear markets several times. Although, each of those swing events would not have felt anything like a roller coaster at the moment when it occurred. As each bear or bull cycle could last for months or years.

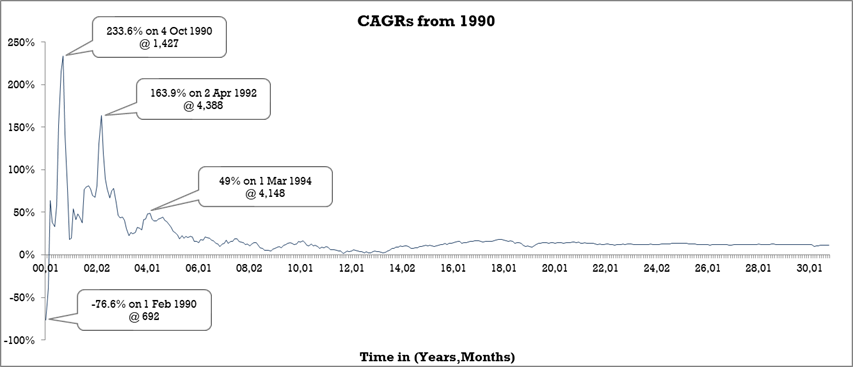

Now let’s look at the monthly CAGRs for this investor and see how the swings in the market translate into the portfolio’s returns.

In the initial 4 years, we see very big fluctuations in either directions. On the higher side, the CAGR touched as high as 233%, and on the lower side, it went as low as -76%. It might be hard to do so, but these numbers need to be ignored as short-term volatilities. They mean nothing for a real long-term investor.

These starting years would have been very exhilarating for a new investor. It would be a grave mistake if an investor took it to be the general norm. These kinds of supersonic starts instill false hopes and confidence in naive investors, and you need to be very careful when you experience any such performance.

The real story starts after this. So, let’s see what happens to our long-term SIP investor after the first 4 years have passed. For this, we will have a look at the zoomed-in chart. So that we can see the variations a lot better, which were otherwise dwarfed in the previous chart.

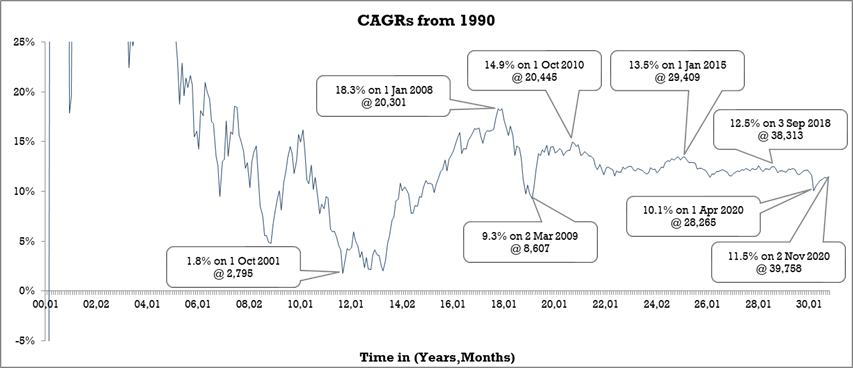

Here, we notice that after the 4th year there was a downward trend which continued till the 12th year. Of course, there were a few bounce-backs in between, but the overall trend remained downwards. This decline had a very negative impact on the returns, so much that the CAGR touched a low of 1.8% on 1 October 2001 (12th year of investment).

Now, imagine yourself in this long-term SIP investor’s place. What would be going through your mind, if after experiencing astonishing returns of 100%+ returns, you were to get only 1.8% CAGR after 12 long years of dedicated investments. In these 12 long years, you see your portfolio going only in one direction, month after month as if there is no end.

12 years is indeed a very long time, especially in a downward market. A negative move for a few days or months is enough to make any investor anxious. And if it continues for longer periods, it could even shatter the confidence of seasoned investors. In the scenario explained above, many investors would have taken out their money and left the markets for good.

12 years of disciplined investments resulting in a 1.8% CAGR is a very poor performance by any standards. This shows that even long term investments are not any guarantee for great returns, at least in this scenario. Please bear in mind that there will be other scenarios that narrate a very different story though.

But nothing lasts forever. Let’s see what happened to investors who had the courage and conviction to stay invested and continue with their SIPs. As we can see from the chart above, things start to move up after the 13th year (2003). In fact, within another 5 years, the same SIP portfolio gave a CAGR of an astonishing 18.5% (January 2008). This is the 18th year since the start of the first SIP installment.

People who had stopped their SIPs a long time back, and did not ever come back to invest after their miserable initial experience, would not even know what they had missed out on. Only the people who stayed back would have felt a sense of fulfillment or relief after a very demanding journey of 18 long years. But the story never ends on its own. You as an investor have to decide, when to start and when to end. We will see, what happens next to the investments of our long-term SIP investor.

As we move ahead, the CAGR falls to a low of 9.3% within a year (March 2009, 19th year of investment). This is due to the sub-prime crisis. This is the time when markets had collapsed by over 60% from their peaks. One would have expected the CAGRs also to go back to the levels of the early 2000s (below 2%) following this market crash, but it didn’t.

During this period, the CAGR drops significantly but still holds itself at a very healthy level of 9.3%, only because of the regular investments through the highs and the lows of the past 18 years. Please note, this is by no means the best investment strategy. You can and should decide on more intelligent and active strategies of dynamic allocation of your funds across different investment instruments, and different time periods. What I am trying to highlight here, is the performance of a simple and regular strategy.

You should decide for yourself, which strategy might work best for you. Not only in terms of returns, but also in terms of safeguarding your portfolio’s downside, your nights’ sleep, and your mental peace.

The rest of the story that we can see is very bland. I have highlighted a few points along the journey which show that the CAGRs keep oscillating within a healthy range of 10% to 15% by the time the investments complete their 30 years journey.

You can never predict what move the markets will make next. But any sharp rise or fall in the market levels will have a lesser impact on your CAGRs as you add more years of investments in your journey. Reminder – this was just one story. And stories can be very different for some other investor, depending on when you start. So, let’s dig into another story to get a fuller and a better picture.

When you started before the great crash of 2008

We come to that point in our article where we fulfill our promise to look at another scenario or story. We have attempted to make this scenario conservative and different from the one discussed above. This is to give a contrasting, or you may say close to a complete view of an investor’s experience. For this purpose, we have chosen to take the beginning of 2008 as the starting point of SIPs. This is when markets were at their all-time high, all over the world. And right after that, the markets came tumbling down, thanks to the sub-prime crisis.

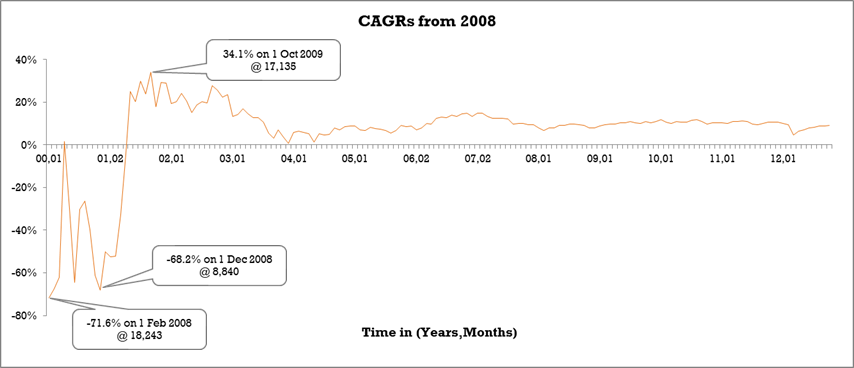

Time to look at the chart of CAGRs for our new long-term SIP investor.

This start is nothing close to an ideal start. Our investor hardly saw any positive returns in the first year. In fact, for the first year, the CAGRs were below -50% nearly all the time. This is one of the worst possible starts an investor could have experienced. That is the reason why we chose 2008, to see how the journey panned out after such a disastrous start.

The investor experiences CAGRs of -71.6% and -68.2% within the first investment year. Then things start to turn around nearly a year and a half later. The performance dramatically changes from ultra negative to super positive. CAGRs touch the levels of 34% by October 2009, which is less than 2 years on investment duration.

Any new investor would have been utterly confused by what he/she had seen in these two years. Again, as seen earlier the initial 4-5 years can be very misleading. The true returns for a real long-term SIP investor start to emerge only after a few more years.

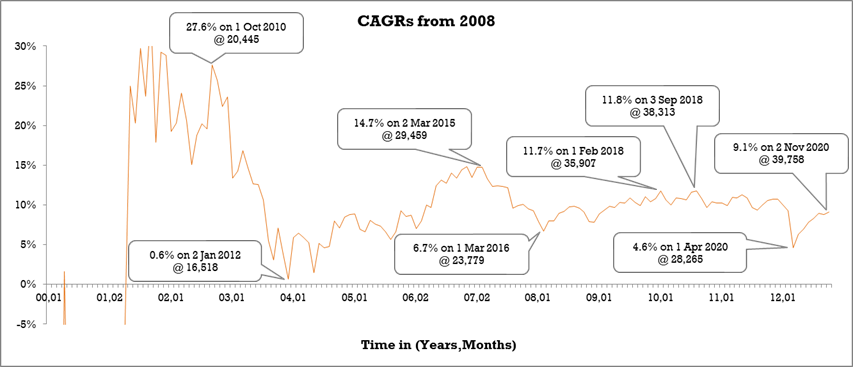

Let’s have a closer look at the following years to understand the SIP performance. For that, we have zoomed in on the chart below.

What do you notice here? After the remarkable recovery in the first two years, the performance dips again for the next couple of years. CAGRs almost touch the zero levels in Jan 2012, just 4 years into the investment duration. But after that, things start to pick up again.

These initial years can tire out many investors for good and force them out of the market. Some might still decide to stick around for longer periods. Let’s see what happens to these kinds of investors.

In the following years, the CAGR fluctuates to a large extent. Although most of the time, it remains above 9%, there are phases in between where it falls below 7%. It touches a low of 4.6% after 12 years of investments in April 2020 (Thanks to Covid-19). Then it bounces back to 9.1% within just 7 months. It remains to be seen what is in store for the future.

The longer time period has a stabilizing effect on the CAGRs. It is true for both scenarios. If you were to compare the last 5 years in both the scenarios, you will see this effect more predominant in the first case. This is due to the much longer investment period there.

Conclusion:

Long term SIP investments are a simple technique. It is not the best or the most optimal investment strategy. There can be times where SIP investment of 10-12 years can give near-zero CAGRs. But staying invested for a really long duration eventually irons out the major downsides. Another very important factor is the time when you enter the market. But eventually, if you decide to continue with the simple SIP strategy, the effect of start time will also fade out.

It is for you to decide your SIP strategy. Remember there is no optimal strategy that you can plan for. You can only be sure of the best strategy in the past, not the future. Do you get what am I saying?

Links to related articles below:

- Case study on SIP (Sensex)

- Case study on midcaps SIPs

- Case study on smallcaps SIPs

- Case study on SIP comparison

- Largecap SIPs – Study 2

- Midcap SIPs – Study 2

- Smallcap SIPs – Study 2

Data sourced from: https://www.bseindia.com/Indices/IndexArchiveData.html