Updated on: July 16, 2020 ; Wealth & Value

What is diversification?

Some of you might already have some idea of what diversification means. I will explain it in brief, with a very simple example so that all of us are on the same page.

Mr. Maalik Seth has recently opened a new departmental store in his residential colony. It is a small shop, and there is limited storage capacity to store items. So, Maalik needs to utilize the space very judiciously.

In recent times he noticed a rising demand for instant noodles in his colony. He expects this trend to continue for a few months, so he needs to plan for stocking the right amount and type of noodles in his store. But he is faced with a problem – the brand preference of his customers keeps changing. There is no brand-wise trend based on which he can make any predictions.

Now, Maalik can’t keep unlimited stocks of all the key brands of noodles. He doesn’t want to stock only one brand either, as then he faces the risk of losing sales of customers with other preferences.

So he decides to stock packs of the top four most-popular brands. He looks at the past data and makes an educated guess on how much of each brand he would store.

This strategy may not give Maalik the best possible sales figure for the month. But this will definitely help him in averting the risk of losing some sales or worse, not doing any noodles sales at all. This is an example of diversification of the noodles portfolio.

A similar approach is followed in the world of investments as well. We will explain this concept using a few scenarios. There can be many strategies of diversification that an investor can choose. Here, we will take the example of very basic asset allocation, which is explained in detail below:

Diversification scenarios:

In the scenarios below, we will be looking at a portfolio that is diversified into three asset classes: Equity, Fixed Income, and Gold. These asset classes have different characteristics and will serve as good candidates for a diversified portfolio. You can choose other asset classes as well. To know more about investment instruments, read here.

In each scenario, we will change the composition of the asset classes and observe the portfolio performance at different times over 20 years (Jan 2000 till March 2020).

We have chosen the following candidates within each asset class:

- Equity: Nifty 50 index. The value changes based on many market-linked factors. Price movements can be erratic.

- Fixed Income: 10-year government bonds. We have repriced the bonds daily, based on the previous day’s yield. This is not the ideal scenario, but a very good approximation of how a fixed income instrument would be valued over 20 years. The value changes more or less at a smooth pace.

- Gold: Historical gold price per ounce. The price varies based on the supply and demand for gold. Like equity, there is no trend seen in the price movements.

Initial investment: We start with the initial investment of 1,00,000 rupees. This money is invested on 3rd Jan 2000 across the three asset classes. The proportion of investment across the asset classes will change with different scenarios.

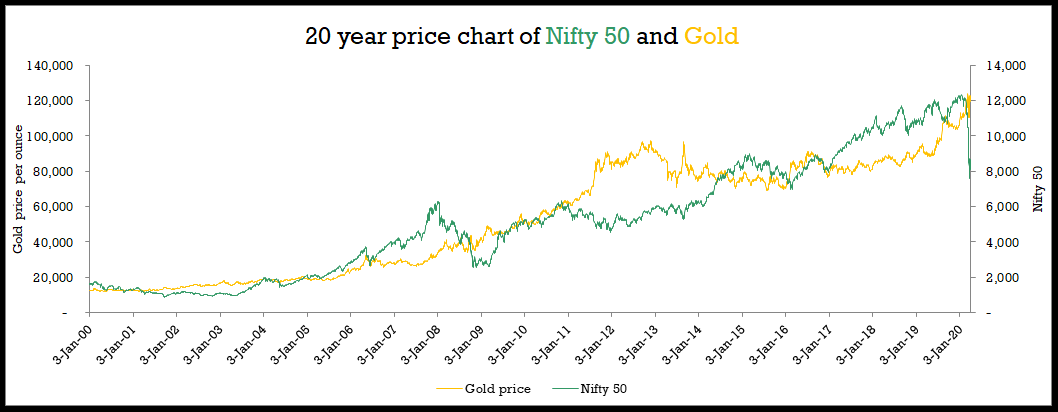

Observation points: We have chosen 10 points in the 20 years, where we evaluate the performance of the portfolio. These points are based on some of the highs and lows of Nifty 50 and gold prices.

Looking at the price trends of gold and nifty 50 in the chart above, you should be able to easily spot some of these points of interest. So we have taken 10 such points for our analysis.

Also, notice the relationship between the two trend lines. They tend to balance out each other very well at a broad level. When the equities (Nifty 50) fall, gold prices tend to hold their growth trend or increase. So they naturally make good candidates for a diversified portfolio.

On the other hand, bonds show a very steady growth rate. So, including them in a portfolio provides some stability.

I encourage you to do your research and revise the below scenarios for any other observation points. Now let’s have a quick look at the definition of the scenarios.

The scenarios: The four scenarios:

- Scenario 1: Equal allocation. Each asset class gets 33.33% of the initial investment.

- Scenario 2: Equity heavy. Nifty 50 gets 70% allocation. The other two asset classes get 15% each.

- Scenario 3: Fixed income heavy. Bonds get 70% allocation. The other two asset classes get 15% each.

- Scenario 4: Gold heavy. Gold gets a 70% allocation. The Other two asset classes get 15% each.

So far we have covered the background of the analysis and the scenarios. So, it’s time to look into the scenarios.

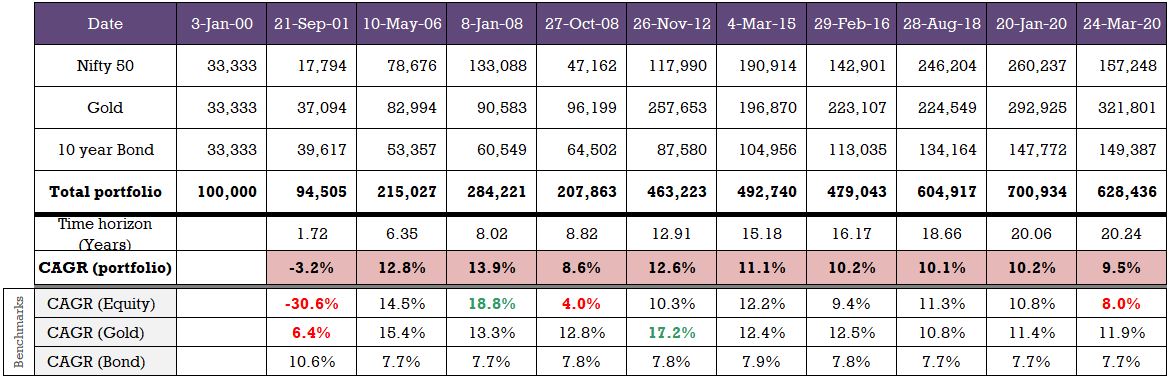

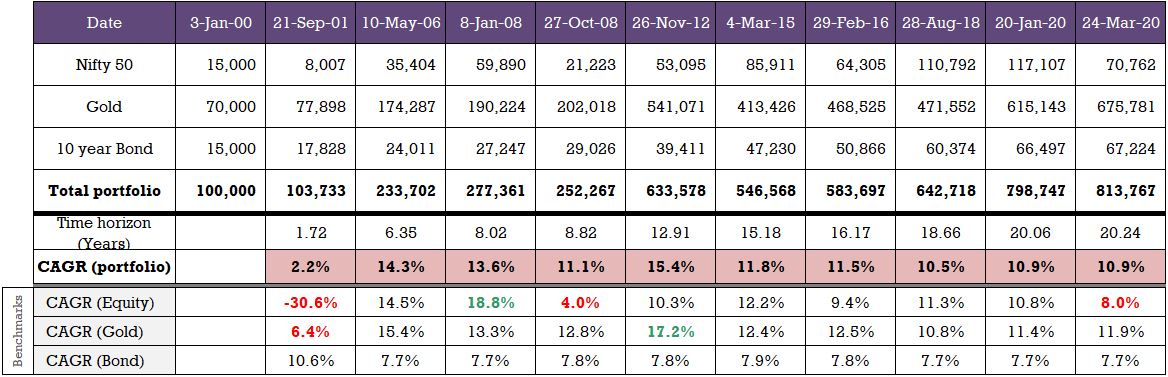

Scenario 1:

This scenario has 33.33% allocation for equity, fixed income and gold each.

Before we start with the analysis, I will provide a simple explanation of how to read the scenario tables. So, don’t get bothered by so many numbers in the table. I also apologize for the poor quality of the image. I hope it is legible enough for you to decipher the information in there.

There are 11 date columns in the table. The first date column represents the investment date (3rd January 2020), and the next 10 columns represent the observation points.

The first three rows specify the value of each asset class in the portfolio, on the respective dates. Please note that while arriving at the values, I have not accounted for any other charges like brokerage, management charges, taxes, etc. This should not have any considerable impact on studying the use-case of diversification.

The fourth row shows the value of the entire portfolio on the respective dates.

Next comes the time horizon (years) row that specifies the time for which the capital is invested. Please note that the time gap between the observation points is not uniform, as we have chosen these dates based on some highs and lows of the asset classes observed in the 20 years.

Below that, we have the CAGR of the portfolio, which represents the returns of the portfolio. We will use this number to measure and compare the performance of the portfolios.

Now, we have three more rows at the bottom of the table categorized as benchmarks. They show the performance of each asset class individually. This will help us analyze portfolio performances across scenarios.

You will also notice that some numbers are colored in red and green. These are just a few points when the asset class delivered very high (green) or very low (red) returns.

In case you are wondering that I missed coloring the benchmark for bonds, I left it as is on purpose. Bond prices don’t fluctuate like the other two asset classes. You can see for yourself by observing the numbers that they have maintained a steady rate over the 20 years.

Finally it’s time to start analying the scenarios one by one.

Let’s first look at the observation points with low returns. The portfolio returns -3.2% on 21 Sep 2001. Compare this with the equity performance for the same time, which is -30.6%. Observe the portfolio returns on 27 Oct 2008 and 24 Mar 2020. The returns are at the lower end, 8.6% and 9.5% respectively. But it is far better than the equity performance of 4.0% and 8.0%.

So, you can see that diversification limited the downside risk. Now it’s time to look at observation points with high returns.

Look at the returns on 8 Jan 2008 and 26 Nov 2012. The portfolio CAGR was 13.9% and 12.6% on these respective dates. These are very good performance numbers. Although lower than the equity performance of 18.8% on 8 Jan 2008 and gold performance of 17.2% on 20 Nov 2012.

If you look at the other observation points, you will notice that the CAGR is range-bound. The portfolio has delivered decent returns (more than 8.5%) 90% of the time.

Next, compare the portfolio CAGR with the benchmark CAGRs of the three asset classes, across the 10 observation points. The portfolio performance is far more stable than the performance of equity and gold. At the same time, it is higher than the steady CAGR of the bond.

If you are having some thoughts on gold performance being better than the portfolio performance, then you are thinking in the right direction. For now, just hold on to that thought because we will come back to that after covering the four scenarios.

Now, this scenario was based on a balanced allocation. The fluctuation in your portfolio’s performance greatly depends on the percentage allocation across asset classes.

Next, let’s observe how the performance varies based on all the different diversification strategies in the scenarios discussed below:

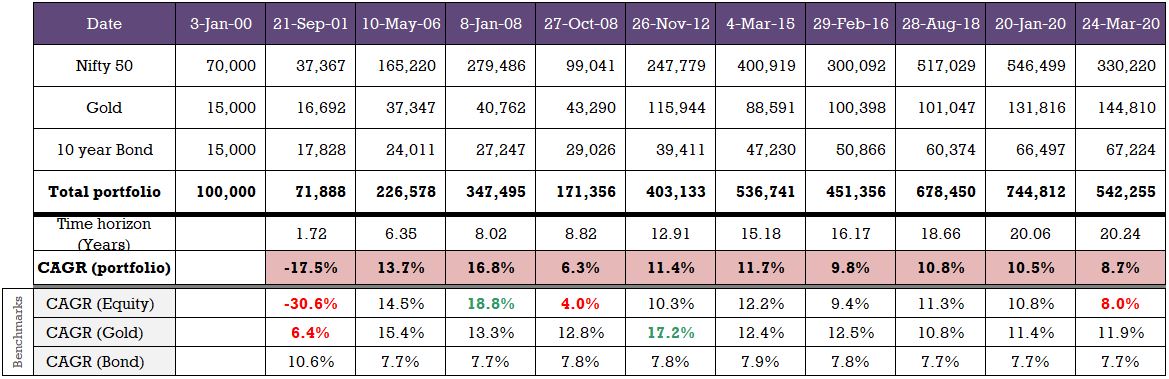

Scenario 2:

This scenario has 70% allocation in equity, 15% in fixed income, and 15% in gold.

Now, this portfolio leans heavily on equity. Therefore the returns will follow the equity trend more closely when compared to scenario 1.

This portfolio incurs a heavy loss of -17.5% CAGR on 21 Sep 2001. This is much lower than the portfolio loss of -3.2% in scenario 1.

However, during good times, like on 8 Jan 2008, the portfolio returned a CAGR of 16.8%. This is much higher than the portfolio gains of 13.9% in scenario 1.

You will notice that the movement in the CAGR of this portfolio is much higher than that of scenario 1. Depending on the observation point you look at, scenario 2 could be better or worse than scenario 1. This heavily depends on the performance of equity.

But still, at an overall level, the returns are in a very decent range after staying invested for more than 8-9 years. Now, let’s have a quick look at the other two scenarios before we conclude.

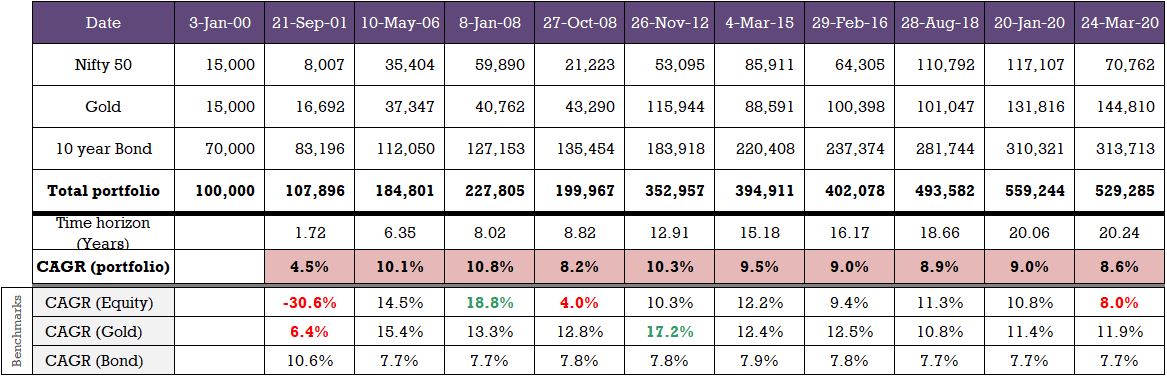

Scenario 3:

This scenario has 70% allocation in fixed income, 15% in equity, and 15% in gold.

Now, this portfolio leans heavily on bonds, which has a stable growth rate. The CAGR returns over the 10 observation points are in a narrow range, except for the first observation point. In any investment, there can be higher volatility in the initial phases, as CAGR is a function of time.

The portfolio consistently performs better(after the first observation point) than the bond benchmark, which is a good sign. At the same time, at most of the observation points, the returns are lower than scenario 1 and scenario 2.

So, what you get here is a more safe and secure portfolio with a little lower returns than the first two scenarios. Now it’s time to look at the last diversification scenario.

Scenario 4:

The last scenario has 70% allocation in gold, 15% in equity, and 15% in fixed income.

Compare the performance of this portfolio with other scenarios. This one looks the best among the four scenarios as it outperforms the other three scenarios on most occasions.

So, would you conclude that investing in gold or gold heavy portfolio is the best diversification strategy?

Just wait till we have a look at one alternate scenario, before jumping on to any conclusion.

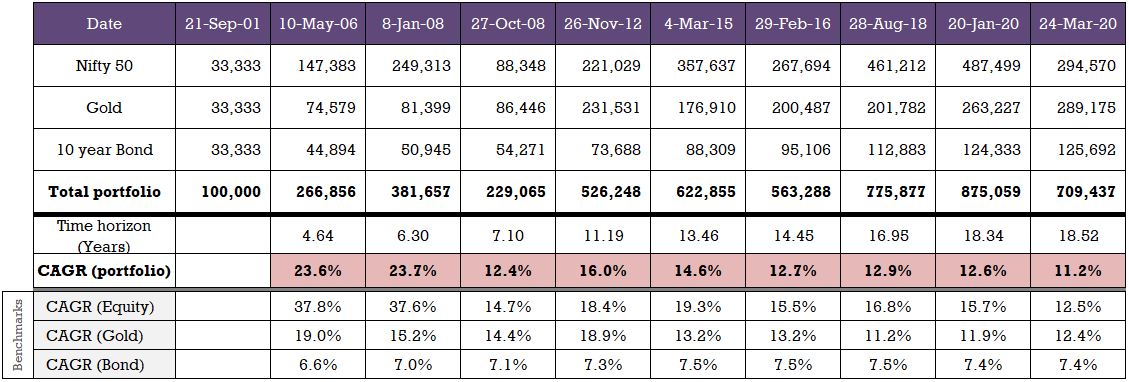

Alternate diversification scenario:

In all the scenarios discussed above, the investment date was 3 Jan 2000. But in real life, you have to keep investing at regular intervals, and this might have been just one of those many investment points. Let’s analyze an alternate scenario where the investment was made on the first observation point (21 Sep 2001).

Consider this scenario. Compare the performance of this scenario with scenario 1. This scenario performs much better than scenario 1.

Now take a look at the CAGR (Equity). The returns are amazing. An equity heavy portfolio would have given even higher returns.

Do you notice the contrast in the performance of this scenario with the other scenarios? We are looking at the same asset classes and the same observation points. So why this big difference in performance? It all depends on the time when you invested your money.

Now, let’s revisit the thoughts we had on gold being our best investment asset. Would that belief still stand valid in this alternate scenario? No, on the contrary, this scenario favors an equity heavy asset allocation.

So what did we learn from all these scenarios?

Diversification reduces the downside risks if asset-allocation is done properly.

Over a long period, you will start seeing less volatility in your returns(CAGR).

Certain diversification strategies may perform well for one time of investment, and some other strategy might work well for other times.

But nobody has seen the future, and no one can predict which diversification strategy will work best for you. So you have to decide on your diversification strategy based on your risk appetite and research.

You can keep changing your strategy based on the price movements of your assets. Just be cautious of not overdoing it.

In this article, we discussed the concept of diversification using very basic examples of asset allocation. In real life, you can diversify into many sub-asset classes as well, like different stocks, bonds, mutual funds, etc. You can read some of them here.

Conclusion:

So, diversification is an important concept to cover your losses or reduce your risks of incurring a loss. There is no set rule on the best diversification strategy. You have to choose your asset classes wisely. They should suit your risk profile and provide some stability to your investments. Ideally, the asset classes should be such that they cover for the dips in the other asset classes in the portfolio.

Keep investing with diversification!!!